http://www.livemint.com/Companies/aPjdpeCxSx3ZnRufO5nHXJ/Capital-First-promoter-looks-to-sell-onethird-stake.html

Warburg sells 25% stake. Looking ahead for more correction to take a position.

1 Like

It helps to evaluate own invested company performance against sectorial peers and becomes ‘legally required’ (![]() ), if you are pitched against someone as formidable as a Bajaj Finance.

), if you are pitched against someone as formidable as a Bajaj Finance.

Here is quick summary, almost consistent >30% CAGR revenue growth for both of them. Attained largely by identifying profitable gaps within the structured financial system.

What differentiates a boy from a man is just evident from ROA metric. While Bajaj has maintained (and improved actually) a ROA of >3. Whereas CapitalFirst has ROA of approx. 1.5 for FY17. Key point to notice is that there is gradual improvement in ROA for Capital First.

.

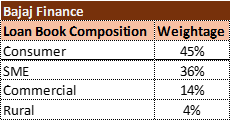

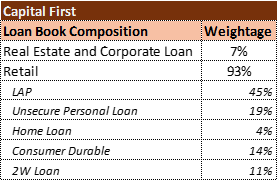

What is driving this disparity in ROA? Much before the Net margin level view, even at Operating margin level both of them got an evident gap. This gap can be understood best by understanding the underlying loan book composition for each of them.

Bajaj with its innovative wide range of product offering and distribution reach has created a virtuous auto propelled growth path within the consumer fiancé business. Siblings Bajaj Auto and Bajaj Finance providing perfect symbiotic support to each other and stand to benefit in the process. Same goes with white good distributor alliance and on-line partnerships.

Whereas Capital First still trying to pivot away from its heritage. As of now, 14% of total revenue from consumer durable and 11% from 2W. Majority (45%) comes from LAP.

Most significant part to be called –out (and that will explain the disparity in operating/net margin) is that LAP has an IRR ~10.50 % whereas consumer durable finance and 2/3W finance got ~25% IRR.

Now is the time to apply a little beyond type 1 thinking (however, not exactly a level 2).

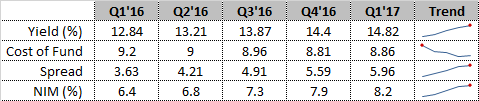

- Other key metric from a landing business entity perspective is NII. Bajan finance got NII of 10.30% whereas Capital First is just shy to it at 9.30% (no typoes, they are very close).

- Not to forget, growth engine is firing on all cylinders and have shown directional resolve by improving retail loan book from 10% of total AUM in FY10 to >90% that too when the AUM has increased by a whopping 20 items within these 7 years.

- Being consistent with the narrative, they have shown a growth of 62% in the lucrative consumer durable finance for the FY’17. Likewise, 44% growth in 2W finance and 22% in Home Loan.

- On one hand this pivoting towards better IRR accretive business will improve the yield on the other hand the cost of funds are expected to come down from consistent rating improvement. Within FY’17 they have improved the long term credit rating from AA+ to AAA. Positive on both tails is expected to improve the NII further.

- What I see is that Bajaj Finance quoting at trailing 10.59 times book whereas Capital First at 3.15 times book.

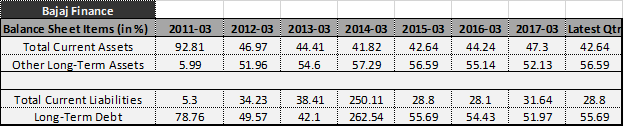

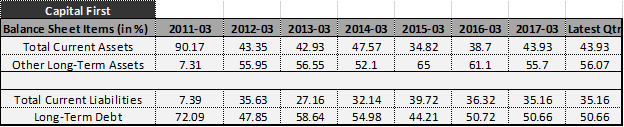

- Another very interesting point is related to the balance sheet composition:

What I see here is that for Capital First, comparatively higher % of assets (as % of balance sheet) are in long term asset category. Also, on the other hand they have higher mix of current liabilities as compared to long term liabilities. Thinking aloud, this appears to be best strategy in a falling interest rate market where you locked your lending for a longer duration with a higher interest rate and are also stand to benefit with each subsequent slide in interest rate while borrowing.

In conclusion, this is not other Bajaj Finance for sure. However, banking on the growth and move towards margin accretive business can make this an interesting story down the line.

As always, counter views, different perspective invited.

Tarun

Disc: Invested, no transaction in last 6 months.

34 Likes

Great Comparison and superb analysis…It wud be intertesting to know whether these Long terms higher interest rate locked assets cannot be refinanced by customers with competitors and how would that impact the ROA picture

Cheers

Tarun

Very pertinent question. As much I know about this company, the answer lies in understanding a) target customer profile b) loan objective and c) worthiness evaluation process for the loan.

Most of those are SME LAP loans meant for working capital requirements,equipment finance etc for the small/micro/medium enterprises with average duration of ~ 5 year and average ticket size INR 7 -20 Mn.Talking about the credit worthiness evaluation, where Capital First is different is the fact that their risk evaluation is mostly based on cash flow analysis whereas most of the traditional lenders are looking at collateral valuation to evaluate worthiness. (Which one between the two approach is better can be a topic of an altogether separate thesis though).

In my limited understanding most of the competitive players are much focused towards building a portfolio of better IRR business like CD, vehicle finance etc. and undercutting each other there fiercely while ignoring basics of underwriting practices . Since this LAP SME business is not much IRR lucrative, not much of incentive for poaching each others customers.

Though little dated however some relevant reading from Edelweiss research report:Capital-First-Edelweiss.pdf (1.3 MB)

Tarun

6 Likes

Thanks Tarun Jee for excellent analysis… Just wanted to know your thoughts about the recent stake sell by Warburg Pincus… Regards

First things first, all 'sir’s left India in 1947 and 'jee’s should have much earlier.  Seriously, all of us are just fellow seekers pursuing common interests and in the process getting mutual help. So, I am not ok with suffix/prefix.

Seriously, all of us are just fellow seekers pursuing common interests and in the process getting mutual help. So, I am not ok with suffix/prefix.

With regards to Waburg Pincus stake sale, I will not pretend that I have some deep expertise on PIPE

(Private investment in public equity) investment, however, what I read and understand is that these are not open ended investments. In that sense, they have predefined objective and milestones with eventual target time horizon, target multiplier etc.baked into the decision. Accordingly, this stake sale is to take some profit off table. However, not to forget, they still have ~36% stake and are single largest stakeholder.

Other way to look at it is that while Warburg Pincus has reduced from 61% to 36%, other marquee name GIC of Singapore has infused apprix INR 3.5B thus increasing stake to 14%.If I i am recalling it correctly, this GIC of SIngapore is ALSO one of the top share holder for Bajaj Finance.

In summary, at least I am not able to read much between the lines with respect to Warburg exit.

Thanks,

Tarun

6 Likes

Thanks again… On a lighter note, Jee is just a simple way to show sincere respect/appreciation, which actually can’t be compared with Sir in Indian context… Regards

2 Likes

This is actually one of the near perfect visual (though with limited data points) to convey the message - “here is someone who is on a mission”.

Near perfect execution in improving each of the ‘metric that matters’.

I think in each subsequent posts I am just getting carried away towards positives. Will appreciate if someone can really come-up with ‘specific’ counter view. What is really not adding up/ is way too good/ may not pan out/ blind spots etc. etc.

Tarun

12 Likes

Thx Tarun…Much appreciated…It’s a good company having makings of a great one…I agree, Just need to time the avg entry points…Can be a MB in 3-4 years Time frame

Hi,

I’m new to this forum and really enjoying the free flow of information and learning that is taking place here.

With the roll-out of GST imminent and some of the commentators predicting a bleak-future for the SME (Small and medium enterprises) sector in the post GST scenario , I’d like to understand from the knowledgeable boarders their views on the impact of GST on Capital First , given the fact that it has very high exposure to this sector.

Any comments/ thoughts is welcome.

Discl:Invested.

1 Like

Hi Som…My two cents…GST will not prove to be a death knell that most experts are making it to be. Yes 1-2 Qtrs it wll be disruptive for some of them…Govt will keep on tweaking as they see it fit depending the proposed compliance requirements and costs…Couple of my aquaintences in the Gems and Textile side have said that for sure next qtr will be a adjustment/consolidation and not much growth so yes in context of Cap first what we need to see if the client profiles. You can read Tarun’s brillant analysis above.

From my exp with Cap First, it provides excellent entry points and Yes the Story is a great one for me 3 years down the line., considering Govts push to develop all sort of india centric industries.

Disclaimer - 375 -> 720 is when i was invested and looking at better entry points.

1 Like

During the Warburg Pincus sale last month, VV (vaidyanathan) came on TV and emphasized that we do not need to raise any further capital. Since then I have seen multiple announcements from CAPF regarding fund-raise through NCDs. While these fund-raises do not dilute equity, I am just wondering if there is a risk of further equity dilution in CAPF leading to diminished returns in future. I see that RoE of BajajFin is higher than CAPF which has made it a better investment so far…

Discl: invested, exited and looking to enter again at lower prices

When they say they don’t need further capital, it means equity capital or Tier II bonds. If there is further equity dilution, it’s not a risk. It’s good for company and it’s growth. Bajaj Finance has much higher ROA than CapF and hence better ROE.

5 Likes

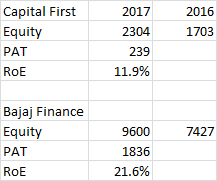

I was going through Annual report 2017 of Capital first and found out an interesting piece. I have compared the RoE for both-Capital First and Bajaj Finance and underlying reasons for that.

And, I have some serious concerns with Capital First.

RoE computation-

Two reasons for high RoE can be high yields or high capital gearing. Then, I computed these figures for both the companies for 2017-

But, for both the points, Capital first fairs equally with Bajaj Finance. So, the problem of low RoE is not related to these two points. Then, there must be some problem with the cost structure. Either, Capital First cost of borrowing is very high or there are very high provisions/write-offs.

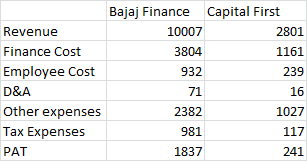

I went to the consolidated 2017 financials and they are as below-

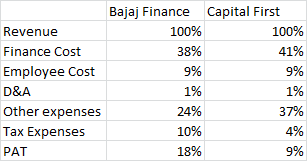

Re-basing everything to revenue-

This was shocking to me as why other expenses difference is 13%. Digging deep, it came down to two factors.

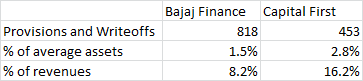

1- First factor is the provisions and write-offs

Capital First has written off approx 403 crore of assets and that is approx 2.5% of their average assets. This is inspite of them claiming that they have very stable asset quality. I think they write-off the loans to under-report NPA’s. This is one very serious observation I have found.

Again, They have Amortised loan origination cost that is approx 237cr and is 8.5% of the revenue. I have no clue what it is about. Can anyone help me with that?

I don’t think RoE will improve much if this condition persists where they have to write off such amount of loans.

I am new to valuepickr and looking for comments and feedback.

44 Likes

Very nice analysis Karan!

Were the write-offs high only in FY2017 or is it a long-standing problem for the company?

1 Like

Hi Karan attending CAPF AGM today shall get a clarification on this point. Many thanks for your fantastic analysis.

2 Likes

Thank you so much!

Can you please ask them about amortised loan origination cost too ??

Looking forward for your post.

I do not think this is the correct interpretation. The NPA are reported as GNPA & NNPA

Gross NPA = Total Bad Loans

Net NPA = GNPA - Provisions

So this data is always available. I would rather interpret that they are maintaining clean books by recognising and writing off bad loans instead of carrying them.

The main question here is whether the management has the ability to put processes in place wherein they can reduce the level of bad loans and actively watch the market and get out of a segment at first signs of stress like Bajaj Finance.

Disclosure: Invested

1 Like

I agree with your point that management is clean and GNPA and NNPA figures are right.

But, Asset quality is not upto the mark and they need to create GNPA and then provisions for the same.

But, I think they don’t recognise bad loans as NPA and straightaway right them off.

Or, They need to tell investors that Asset quality is not upto the mark and we are writing off the loans before recognizing them as GNPA

So, We always see from Investor presentation stable asset quality but it is not so.

They are trying to increase contribution from other segments but still MSME forms a big part.

1 Like

So, what you are saying is basically that they don’t recognise bad loans as NPA and straightaway right them off. I do not know if NBFC can do that under RBI rules, but one can always seek clarifications.

Disclosure: Invested