I think the good thing is that the merged entity will be led by Mr Vaidyanathan… Considering his record in ICICI bank and later in capital first, in all probability he should be able to ensure a good future for the merged company… And address the problems which are crippling IDFC bank…

1 Like

My 2 cents

Good for CF shareholders

- CF shareholders will get IDFC Bank shares at no extra cost

- CF will get access to low liability CASA accounts for investing in high rate loan portfolio

- CF will also get some protection from RBI in case of some Black Swan event (such protection is not available for NBFC but available for Banks)

Bad for CF shareholders

- IDFC has high GNPA and mainly in Infrastructure lending

- CF will be entering infrastructure lending zone which is not their forte - Infrastructure lending is reduced to negligible when CF mgmt took over from Biyani

- IDFC Bank culture will not entrepreneurial culture & can be sarkari office culture (assumption, may not be true) (Vaidya ensured entrepreneurial culture in CF).

This is the biggest impact which can destroy CF

Betting on Vaidya

Investing in CF is betting on Vaidya. We all acknowledge he is an Intelligent Fanatic who took a struggling Biyani company and converted into a super fast growing NBFC.

(Siddharth Lal took loss making Royal Enfield and converted it into super brand.)

Running / owning a Bank was Vaidya’s dream (I guess). He used to joke with his friends that one day he will be running a bank.

Vaidya has to prove here yet again that he can convert struglling bank to the likes of ICICI. One of the pillar on which ICICi Bank has grown is Vaidya.

It would be difficult task handling a sarkari office like culture but Vaidya is Vaidya. Intelligent Fanatics can survive anywhere & will do whatever suits in the interest of the minority shareholders as well.

4 Likes

I am not doubting the ability of Vaidyanathan to run a bank. It took a number of years for him to turn around capital first and the share prices have languished at low levels for a number of years as a result. Now just when things are looking good and the market is ready to give this a higher multiple, Capital First shareholders are again given a number of issues and high GNPA. Market rewards growth visibility and predictability of earnings, both of which are not there for the combined entity. It is a negative for Capital First shareholders if you do not have a forever horizon which most retail investors do not.

4 Likes

I am wondering what made RBI give IDFC a banking license if standing on its own feet was so difficult. I still remember Rajiv Lall’s aversion to the idea of application for banking license. Now he wants to dispose the same to Capital First. Well, Vaidy has experience of how ICiCI’s corporate and infra book slowed down the whole organisation. Still he has gone ahead which makes me believe that it is the PE guys and other prominent investors who has pushed this deal. Now we know why they wanted to pump more as new equity in CFL despite adequate equity. They would care for valuation and exit easily since size will be a helpful factor. The merged entity has become even more difficult to analyse and evaluate.

Disc - No holding in either.

1 Like

have been tracking CF and missed to enter when it was languishing around 680-700 range

With this merger talk now from a value investment would it make sense to buy CF or IDFC bank at this point in time.

I see some members criticising IDFC Bank but I do not think IDFC Bank has been a laggard considering they are mainly focussing on growing the retail biz.

When you say revenue de-grew, you have to look at the segmental revenue to understand why. Looking at sep '17 results, Treasury income fell (I do not know whether this happened at other banks), and wholesale revenue was expected to fall, while retail revenue has grown around 400% YOY. And then, even though they started with a legacy total infra book, now their GNPA is much better than Axis, ICICI. On the deposit front, I am not able to judge that as their strategy till now has been to not open many branches all over the country immediately.

And I will consider this (The CapF merger) an acquisition at 4 times book (not cheap) as a booster for their retail book. Both companies benefit here in my view.

Please correct me if my analysis is wrong.

Disc. : Holding both since Aug '17

2 Likes

1 Like

http://wap.business-standard.com/article/companies/idfc-bank-is-getting-a-person-who-understands-retail-ceo-rajiv-lall-118011300857_1.html view by Rajiv Lall current CEO of idfc bank

1 Like

5 Likes

As per my understanding, you can buy either if you wish to be part of the merged entity. If you choose to buy CF you will get 13.9x shares of the merged entity (which in turn may mean 13.9x of the share price of idfc bank).

Now the valuation has to be calculated based on the price if IDFC Bank??? If so, Whats the impact of regular fall of price??

Any one who is clear can clarify please

According to me there is nothing wrong with that. There are hundreds of arbitrage benefits available in the market. What happens when a company fixes date and price of buyback of its shares? There is a potential benefit of earning 15 - 20% out of it. The company buys back its shares at a pre-decided price despite the change in its share price.

We have analyzed the post merger scenario of Capital First with IDFC bank using the 4 following lenses:

- Standalone business commentary of capital first

Capital First has been performing well within the retail and SME financing NBFC space with a loan book growth rate of 27% (CAGR - from 2013 to Dec 2017). It has been able to manage the net NPAs (0.8%) while still being able to grow healthy at a NIM of 9%. Also, the asset liability mismatch is well covered with no significant risk. Pre-merger available at a P/B of 3 which is low as compared to most relevant peer Bajaj Finance. Its RoE was 12%.

Using a simplistic approach, with business as usual, assuming a loan book growth rate of 20%, NIM of 9%, NPA of 1%, in 2021 we estimate the book value to double in this duration. So, as a standalone entity, Capital First should be 3X from current levels. We also checked in key electronic retail stores where there could be a small affinity towards Capital First since they dont charge any registration fee from new customer unlike Bajaj. To summarize, on standalone basis, Capital First was headed to be 3X from here.

- Standalone commentary of IDFC bank

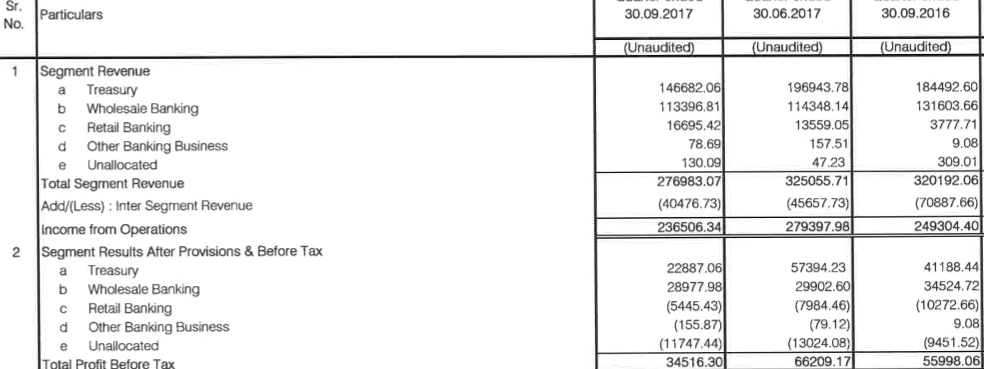

IDFC bank has been suffering badly under NPAs and a slight asset liability mismatch. It has been able to show some decent

results off late due to sale of NPAs to ARC and general tighter control on NPAs. As per company estimates, loan book was 91000 Cr in Dec 2017 and expected to be 1,05,000 in March 2020 giving a growth rate of 7%. Given the way IDFC has run this business so far, we expect not a significant change in NIM and hence it would be in the same range of 1.9%-2% as now. NPAs will be under control and stay on trajectory as of now - close to 2.5% and assuming they provision 100% of net NPAs. They have a asset liability mismatch in 6 months to 1 year as per 2017 Annual report, but since they would have been through that we will come to know only in the next annual report. At a current P/B of 0.9, since key business parameters are not making significant improvement, we think that it will stay in that range. Hence, 3 years down the line, P/B would be close to 1.5X of current.

- What does capital first gain by selling itself to IDFC bank

We see 2 synergies, Capital First gets access to low cost deposits of IDFC bank. Casa + FD of IDFC bank has been improving, from 8200 cr in 2016 to 40000 cr in march 2017. At the same time, borrowings reduced from 57000 cr to 50000 cr. This growth in CASA and FD funds is sufficient to meet the higher margin loan book growth of Capital First (5000 cr on for this year). So the appetite for cheaper funds of Capital First should be met by growing low cost funds of IDFC bank.

Another area we see of synergy is cross selling of products. Anyone taking a retail or SME credit from Capital first could be positioned to open a bank account with IDFC bank and vice versa. There could also be more products in future (MF being one of existing them ) which will generate additional streams of revenue.

One of the reasons why Capital first could have sold itself to a not so great bank as IDFC is - it wanted cheaper source of funds to grow and compete against bajaj finance. Options to raise such money - Debt (can kill a healthy business), Equity dilution (costly source of funds and existing investors might not be keen) or merge with a bank. Having ruled out first 2 options, it could have identified a high-flyer like Yes, Indus or Kotak type bank. But those banks wouldn’t have given a fair deal to Capital First considering their own strong presence. So, it identified a suitable suitor in IDFC bank where Capital First could still call the shots, use the low cost funds and meet its aspiration of being a bank.

4) what could be combined future state - optimistic scenario and pessimistic scenario

Pessimistic scenario: loan book growth rate of 15% overall, NIM at 6%, Opex of 5% and NPAs of 1.5% - assuming that P/B remains 2.5 at end of 3 years, market cap of entity could be 2.4 of what it is today

Optimistic scenario loan book growth rate of 15%, NIM of 7%, Opex of 4% and NPA of 1%, assuming that P/B of 2.5 at end of years, market cap could be 3.5X of today's

Captial First in itself has no asset liability mismatch even now, and apparently IDFC Bank would have either sorted or restructured the mismtach by now.

So, can you please help us to identify any wrong assumptions or missing points in building this analysis before we buy either of this.

- Nikhil and Akash

10 Likes

@CF investors,

Any reason why the stock price has fallen so much despite merger talk? When will the merger complete? Is n’t CF a buy opportunity at CMP considering 139:10?

1 Like

Its a buy.

But what I believe is, Capital First’s share price is now chained to the destiny of IDFC Banks share price with a discount of 7-8% to 13.9 times of idfc bank price.

And idfc bank has historically stayed quite range bound with a downward bias.

Any idea when the merge is planned? I have a feeling that IDFC stock will be sold by CAPF holders. May be that is the reason for IDFCs price hovering near ATLs (apart from its own issues)

1 Like

As per merger announcement press release merger is expected to complete by Oct 2018. However, I recall reading somewhere also April… But can’t recall the source.

The merger should be completed via October. Check out an interesting article with benefits to Capital First more than IDFC Bank.

Link to the Article.- IDFC paying premium to get acquired, will IDFC be second time lucky?

1 Like

Requires us to subscribe. In case you have the subscription, can you share a summary?

They have pie-chart and other images so not able to share the whole thing. Sharing a summary for the same.

Summary for the same

Why the deal with Shriram Group failed?

In July last year, IDFC and Shriram Group had agreed to merge to create a financial conglomerate and offer various types of retail and corporate loans. But the deal was called off following differences over valuation or the swap ratio. The concerns were raised by some IDFC shareholders like Enam Holdings and Sipadan Investments (Mauritius) Ltd. Most shareholders of IDFC were demanding a 60% premium to the current market value of the company. The deal could have still worked had Shriram Capital been split into two parts like merging of Shriram City Union Finance and IDFC Bank. However, that was not possible because of the structure of Shriram Capital. Also, the complex structure proposed by dealmakers was the key reason for the merger failing.

The big challenge

The biggest task for the merged entity will be scaling up the current account, savings account (CASA) base to enjoy lower cost of funds as a universal bank. At present, Capital First does not have access to CASA base. Deposits form only 39% of IDFC Bank’s borrowings and the current and savings accounts ratio is just 8.2%. The pass the deal, the company will have to seek regulatory approvals from Reserve Bank of India, Securities and Exchange Board of India (Sebi), Competition Commission of India and the National Company Law Tribunal. The merger process will take three to four quarters because of all the regulatory approvals. IDFC will also end up subscribing further shares as part of the merger to maintained its stake at least at 40% unless RBI relaxes that requirement

So, in a way the merger is a win-win situation as IDFC Bank will get a strong retail loan book and Capital First will be able to pursue its banking ambitions. While the merger could bump up operations costs in the near term, the merger will benefit the joint entity as the synergistic benefits of lower costs and economies of scale start to accrue over time.

End of Summary

1 Like