Mis-quoted most likely but not sure if they can expect higher valuations this time due to all the issues around NBFC / HFC, economy, market conditions etc. The last time around, Canara bank was in a position to demand but now I guess the buyers will be in that position and they have many other potential acquisitions in the market in general as well.

Can Fin Homes : Targets loan book of Rs 23000 crore by March 2020, reduce GNPA level to FY19 level by Q2FY20

Can Fin Homes conducted a conference call on 23 July 2019 to discuss its financial results for the quarter ended June 2019. Shreekant M Bhandinad, DMD of the company addressed the call:

Highlights:

- The company has recorded healthy performance in the quarter ended June 2019 with 17% growth in loan book to Rs 19003 crore end June 2019 over June 2018. The disbursements of the company have increased 10% to Rs 1276 crore in Q1FY2020.

- The company has recorded loan growth of 22% from non –Karnataka region, while Karnataka loan growth was lower at 7% end June 2019. Loan growth for south region stood at 15% and non-south at 20%.

- About 30% of loan book comes from Karnataka and 70% from South region end June 2019. The company hopes Karnataka region to do well ahead with RERA and GST issues behind now. Also, the unsold inventory is depleting faster in Karnataka.

- The loan growth for salaried and non-salaried was similar end June 2019 with salaried segment contributing 70% to the loan book.

- The company has aims to raise loan book to Rs 23000 crore by end March 2020 from Rs 19003 crore end June 2019.

- The company has recorded revenues growth of 20%, while expenses also moved up 20%. The net profit increased 17% to Rs 81 crore in Q1FY2020.

- The company has exhibited 16 bps improvements in yield on advances, while contained the rise in cost of funds at 3 bps to 7.93% in Q1FY2020 helping to improve margins.

- GNPA of the company have increased to Rs 139 crore end June 2019 from Rs 113 crore end March 2019. However, the net slippages have been lower at Rs 26 crore in Q1FY2020 compared with Rs 40 crore in Q1FY2019. In last full year FY2020, net slippages were Rs 50 crore with Q1FY2019 alone contributing Rs 40 crore which has declined to Rs 26 crore in Q1FY2020.

- With the enhanced efforts on recoveries, the company expects to improve asset quality going forward. In most of NPA cases, the company has already started action under SARFAESI. Thus, the company expects to reduce GNPA to March 2019 level by end September 2019 (Q2FY2020).

- The ECL provision requirement for the company stands at Rs 47 crore, while the company is holding excess provisions of Rs 107 crore end June 2019 of which Rs 46 crore is for NPA and Rs 60 crore is for standard assets.

- The company has made provisions of Rs 6.75 crore for NPA and Rs 1.91 crore for standard assets in Q1FY2020.

- The company has comfortable liquidity positions with sufficient unavailed credit lines of Rs 2000 crore along with additional credit limit sanctions of Rs 2300 crore, which would take care of its funds requirement for next two quarters.

- The outstanding borrowings of the company stand at Rs 16823 crore end June 2019.

3 Likes

I would say, this time they have a better bargaining power. They have proven that they mean quality, and quality players are few and far between.

HFCs or infact NBFCs which have really high quality portfolio now feels like oxymoron.

I doubt Canara management would accept any bids which are lower than what they got in last round, though at the end will also depend on how investors want to play and see India as a market in the long term.

Yes, agree that Canfin kind of stood out in the NBFC turmoil. But their asset quality has been detoriating in a small but steady manner. I wouldn’t be surprised if they hit 1% mark soon. Though it wouldn’t matter for the buyers as it is still way better than many other firms, personally I am watching this parameter every quarter as I suspect it is primarily from higher lending to non salaried class…

This could add pressure to the NIMs of HFCs like Canfin Homes.

HDFC is planning to introduce external benchmark linked loans…similar to what banks are mandated to do by RBI. This is not mandatory for HFCs but competition will force them to do and HFCs don’t have CASA & big term deposits…hence would be a challenge for them to have a flexible / floating type liabilities…

Hello, noticed the corp tax for Canfin homes are around 35%+. Due to the recent tax rate cut, this could benefit them positively right ?

Can someone help to understand?

This action of tax rate cut helps majority of companies and canfin is also benefited. There are different reports in circulation about exact impact in % terms. I did notice a surprising event that PNB Housing came up declaring 8%-9% positive impact for them while few reports expected lesser nos. The surprise was that PNB Housing nosedived after their filing on NSE / BSE.

It affirms the belief that scrips run on rumors / assumptions & fall on news. Similar thing may happen for canfin an others as well.

A simple calculation shows following

For a company paying 35% tax earlier now 25.17% the PAT will jump by 15.12% . As this isn’t a guidance but an increased cash flow till eternity the P/E even if it expands by the same ‘if not more’ should lead to a stock price move of (1.1512 x 1.1512)-1=32.52%.

We must note that this euphoria may not survive for long BUT we must enjoy if we are already IN. Be cautious if you are still planning and want to enter now because slowly but steadily the prices have almost factored in the impact of this announcement.

1 Like

Hi. What’s the update on divestment of Canfin by Canara Bank?

Looks like the bids will be opened only on Nov 7 and not today

Any news source for this?

It’s available in the tenders section in the canara bank website

1 Like

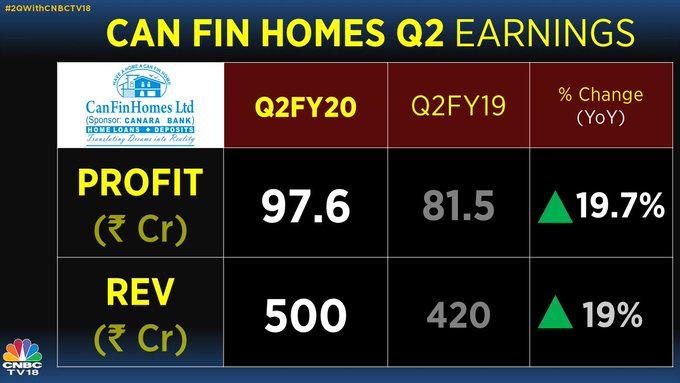

Q2 results:

Really good quarter. Stake sale is the key trigger. Hopefully it goes through post 7Nov and who ever takes over are professional enough and can scale it up. At just a marketcap of 5400 Cr there is certainly huge runway ahead.

Disc: Invested

Q2 investor presentation:

2 Likes

Does anyone know when will the bidding details and the final winner be announced?

When the original dates were announced, the successful bidder was supposed to be announced in 1 week time from date of bid open: so I expect announcement by next thursday

Q2 Concall highlights:

(MD Girish Kousgi, CFO Prashanth Joishy and DGM Shreekant M Bhandinad answered the questions)

NIM 3.2%, Cost of funding 7.95%, Yield 10.23%, Spread 2.28%

DER 8.91, Capital Adequacy Ratio 18.82

Opex slightly high due to new employees, salary increase, CSR spend

Asset quality:

- GNPA 0.79%, NNPA 0.58 slightly higher compared to Q1

- SENP segment contributed in higher NPAs but repossessed assets close to 26 crs in Q1/Q2 and expecting NPA to go down in coming quarters due to recovery

- NPA for salaried 0.47, SENP 1.57. CanFin’s SENP NPA levels are best in industry

- Branches does light underwriting of loans and collection. For above certain threshold values CPCs are used

- PCR 35% comfortable with this level due to expected good recovery

Growth

- Disbursements are flat in H1 as we are cautious due to stress from builders side

- Demand growth coming back in Karnataka, Hyderabad and AP

- Expecting decent growth in the coming quarters with stable asset quality as few competitors stopped/reduced lending

- Focus will be on Tier 2/3/4 cities where competition is less from banks

Capital, Liabilities:

- Have unitized credit lines of 2200 crs

- Will raise retail deposits going forward

- NCD borrowings cost is slightly higher vs banks so didn’t raise any NCDs in the recent

- Bank borrowings are from various banks and Canara bank is not the largest lender so there won’t be any impact of Canara bank’s stake sale

- Capital raising will be decided at later point of time

89% home loans, LAP 4% Plots 1% & other loans 6% - most of these non home loans are given to existing home loan customers after having good repayment history

Disclosure: Holding - Do not recommend buy or sell. Not an investment advisor and Investors are advised to do their own due diligence.

5 Likes

A solo bidder could complicate the sale process. Let’s wait and see how this goes.