Perhaps, the stake sale will go through, this time around…

1 Like

Could you please share me the link for this. Even canfin web portal doesn’t have the latest annual report.

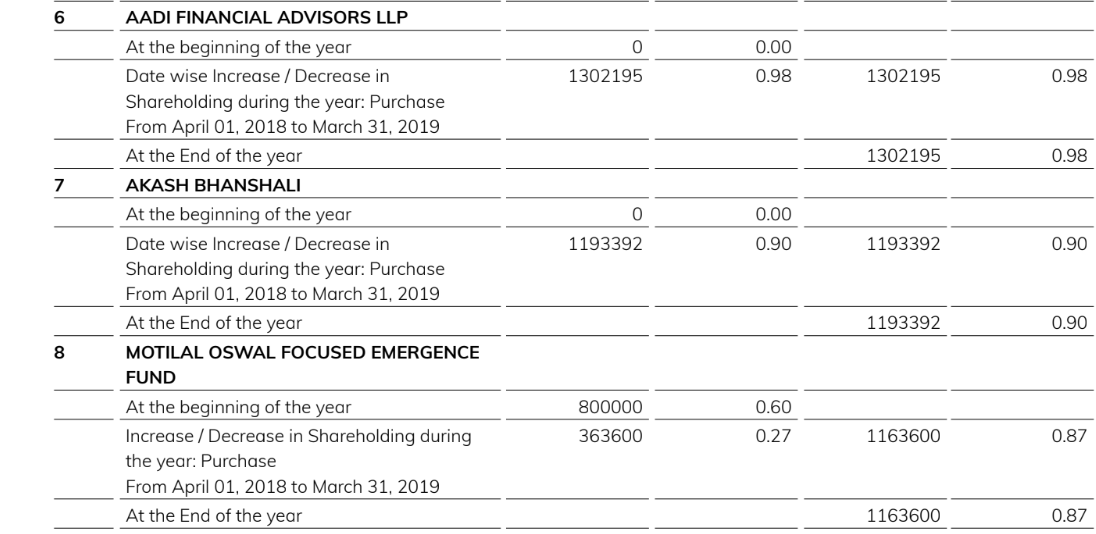

I don’t see his name for the quarter ending on 31st March from the shareholding pattern report.

Thanks in advance.

Canfin homes seems to be breaking out of its trading range on the upsides. DHFL its bigger competitor is warning abt its survival. We have seen how Spicejet/ Indigo gained market-share from Jet fiasco. Odds seems to be in favor of higher prices for Canfin.

4 Likes

Attended Canfin homes AGM today. Below are my notes.

Loan book & growth guidance:

-

Given the liquidity crunch in H2 FY19, still maintained decent growth in FY19

-

Expecting loan book to reach 23k crs as guided

-

Confident of reaching this as good number of branches opened in last 2 years. Normally it takes 1-1.5 years for new branches to stabilize. Each branch has target and reviewed every month

-

Will raise Equity if growth is good. Require equity mainly to improve leverage ratio (~9.5 currently) when growth resumes and Tier-1 capital 17% which is more than adequate

-

Most Bangalore branches are legacy. So good amount of loan closures happens always, If Bangalore grows in double digits, reaching 23k crs will not be an issue

-

Planning open branches in Tier-2 cities like Bellary, Bangalore rural in Karnataka

-

Not planning to buy loan assets from other companies. Will grow organically always.

Asset quality:

-

Maintaining best asset quality remains 1st priority over growth for the company. Bringing down GNPA from current levels is tough but will try to maintain at current levels.

-

Recruited lateral hires from outside like legal officers etc. This will help in asset quality in the longer run

-

Have Chief Risk Officer Mr. Narendra reporting to MD

-

All non housing loans are secured & Not giving any insecure loans. Also exposure to builders are very less always

ALM mismatches on shorter durations: Always have good unused credit lines to take care this and maintain sufficient liquidity at all times. So do not expect any problems

NIM: Expecting maintain and possibly slightly increase

Expenses:

-

Legal fees increased due to INDAS. Audit fees, travel expenses increased due to increase in branches. Still cost to income ratio of 16% which is one of the lowest in the industry

-

Employee expenses didn’t decrease. Shows slight reduction due to lesser provision for gratuity (Have gratuity plan with LIC which had given interest so provision was lesser this year)

MD: New MD appointment will be announced soon as Mr.Sharda Kumar Kota joined NHB. Didn’t clarify for shareholders questions related to whether they’ll hire MD from outside

Stake sale: Canara bank stake sale plans will have not have any operational impact

More customer complains the year: Normally happens when there is an interest rate increase/decrease. All are resolved in FY itself.

4 Likes

I have attended canfin agm. Notes from discussion at AGM/sidelines of AGM ( I may have misinterpreted few points while preparing notes).

Process of appointing new MD and CFO is in advanced stage and will be announced soon. They will be recruited from outside Canara bank as board wants to give them enough time compared to earlier appointments from canara bank for 3 years.

Stake sale: Its decision taken by canara bank and Can fin has nothing to do with it. This will not have any impact on canfin operations will continue to operate independently. Till now nobody has approached for stake and what % canara bank will divest is also not finalised.

Fy19 we have done well considering the overall market condition while other NBFCs have struggled. We should have done much better in the second half but external environment was not conducive.

We will have a better year in fy20. Expect Q3 and Q4 to be good. Reaching 23k cr of loan book for Fy20 is possible.

Bengaluru market is showing improvement and double digit growth in Bengaluru market will helps to achieve 23k cr loan book.

New branches have been opened in tier 2/3 cities and peripheries of Bengaluru. Tickets size from these non metro branches is lower but all the disbursement will be converted into loan book.

Competition and taking over of our loan by NBFCs have stopped. Now banks are giving competition in metro for high ticket size.

As we move away from metro and with small ticket size take over by banks reduces.

Established central processing units in Bengaluru, Hyderabad, chennai and NCR to reduce costs and better efficient collection. Each CPC will be headed by DGM.

Total 175 branches and 14 satellite offices. Converted some satellite offices to branches and closed some non performing offices. Expanded to most of the West, and North India. Few branches in parts of eastern India. Most of new branches are profitable now. Each branch have given targets and review meeting done regularly.

20 more new branches will be opened in tier 2/3 cities in fy20.

Digital: new website… Customer friendly. Easy process to upload and review documents from branches… Planning to launch app. More digitization in future.

CAN FIN focus to remain on asset quality rather than just growth. Net NPA to remain less than 0.5%. Appointed risk assessment officer as directed by NHB who reports directly to MD.

ALM mismatch: we have adequate funds approved from banks can match short-term ALM mismatch easily.

Capital adequacy of 19% ( for technical aspects its mentioned as 16% with 257 cr held with canara bank). No need to raise presently from market.

Bank borrowing to remain dominant. Will try to maintain the cost of funds to <8%. Banks may pass on repo cut by RBI. NIM to be around 3% may slightly improve. Will raise from market if bond rate comes down. We may do QIP if required. We ensure and plan that canfin remain adequately capitalised.

Both Housing and non housing loan(personal and mortgage loan) have adequate security backup ( will not lend without asset backup)

Builder loan : presently very low (11 cr)…wants to grow this in 2 years…will be funding known developer and RERA approved small builders( 50 lac ticket size …minimum 8 flats/5000 sq feet project to be RERA registered in Bengaluru. Builders loans helps to maintain NIM.

Cross selling of insurance is gaining good traction in few quarters after launch. We have tied up with 3 more general insurance companies.

Overall body language was positive. Looks like they will do better this year with good assets quality.

Discl: tracking position

10 Likes

Q1 Results - QoQ comparison is following

Topline - 484 Cr vs 402 Cr

EBITDA - 123 Cr vs 112 Cr

Bottom Line - 81 Cr vs 73 Cr

EPS - 6.08 vs 5.5

canfin_Q1.pdf (266.5 KB)

Press release:

Presentation:

1 Like

Attended Q1 concall today. My notes below (Excluded financial numbers mentioned in the presentation and other points repeated from AGM notes of @narendra and mine ):

NPA:

- Usually slippages more in 1st qtr and NPA comes down in later quarters after invoking SARFAESI

- Expecting Q2-Q3 GNPA to come down to Q4 FY19 levels

- NPA levels are same in North and South, Slight increase in non salaried NPAs but overall its similar to Salaried class

- Underwriting for non salaried is delegated to the branches as it requires specialized skills, interest rate is 50 bps higher

- Do not have separate people for recovery, Same branch people are used for lending, collection and recovery

- Have specialized recovery hubs in Bangalore and Chennai

- Provisions - 40 crs for NPA, 60 crs for standard assets as per INDAS

Funding:

- Have sufficient unavailed credit limits 2000 crs + additional credit 2000 crs for ALM

- Focus for the branches so far have been lending and less on collecting deposits, Now with branches establishing, will be focussing on increasing deposits

Loan book & growth:

- 22% growth excluding Karnataka, 7% growth for Karnataka, 15% South

- Expecting Karnataka to grow better considering fast depleting inventory (30% of book from Karnataka)

- 11% growth in metro, 30% growth in non metro branches

- Growth is similar for salaried and non salaried

- Avg housing loan ticket: 25-30 Lacs for Metro, 10-15 Lacs non metro. This ticket size is usually non viable for banks

- Avg housing loan ticket: 10-11 Lacs and given to existing customers

- Builders loan 11 crs, 6 builders account only

- Most of the lending is for affordable housing loans

- No exposure to interest subvention, Lending is done after seeing the construction progress only - Example if loan is for a flat in 5th floor, then lends only when the construction starts for the 5th floor

- Process 3000 applications every month

- 50% loans sourced from DSA

- Delhi, NCR, Rajasthan regions in north are doing well

- Maintaining 23k crs loan book guidance for FY20 and expecting to grow faster in the coming quarters

Disclosure: Holding - Do not recommend buy or sell. Not an investment advisor and Investors are advised to do their own due diligence.

7 Likes

Company spent a lot of time in finding and onboarding a new CEO, and finally they announced.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=b36cd5b7-14f8-49f0-94a2-4279cee4af8d

Does anyone know how good this executive is? Was it worth the time they spent?

Best-Mahesh

1 Like

Canara Bank invites bids to sell 30% stake in Can Fin Homes - https://www.moneycontrol.com/news/business/canara-bank-invites-bids-to-sell-30-stake-in-can-fin-homes-4412061.html

1 Like

Hopefully considering the merger this time they will actually do the sale as it is permanent hangover on the stock

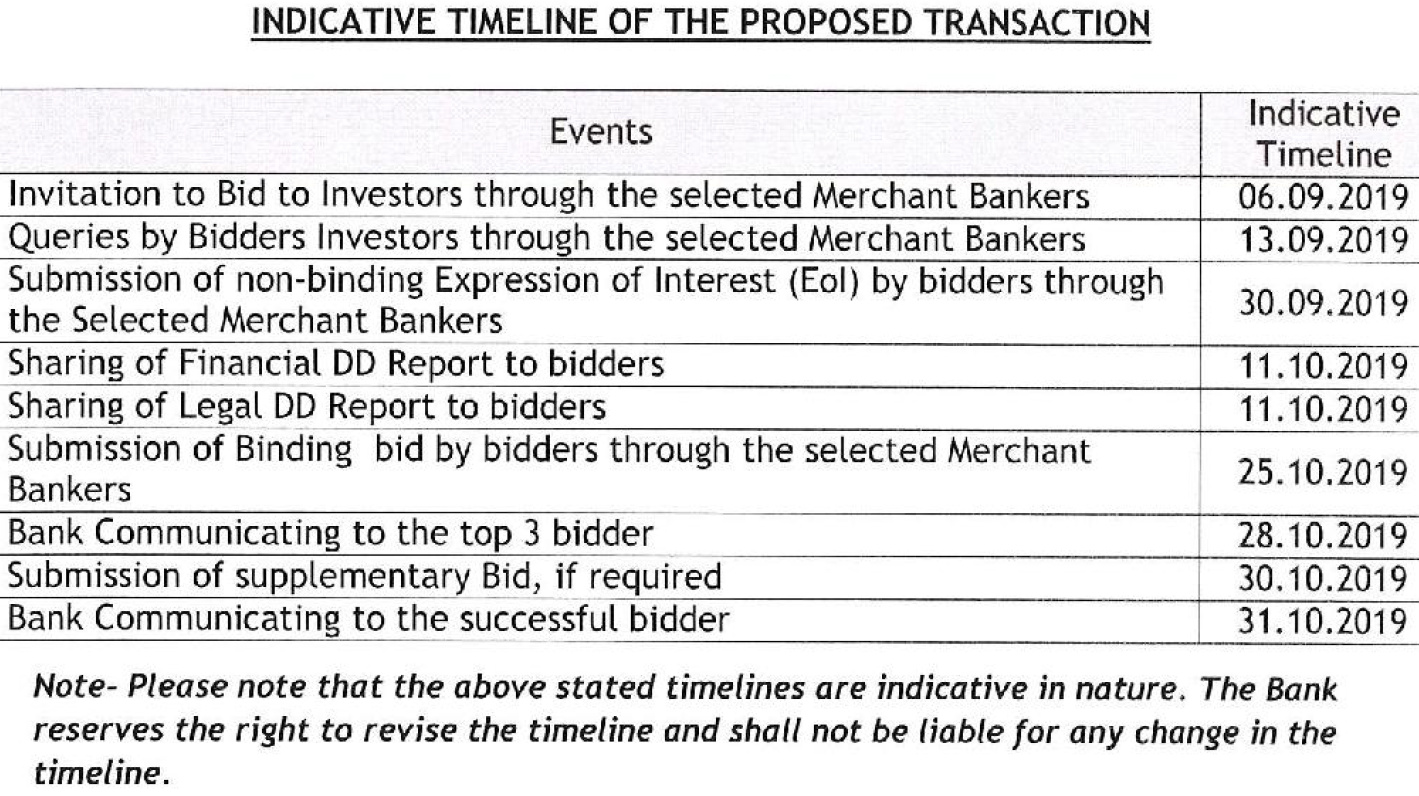

the invitation offer document

https://canarabank.com/media/13729/eoi06092019opt.pdf

Does anyone has their latest earning call transcript ?

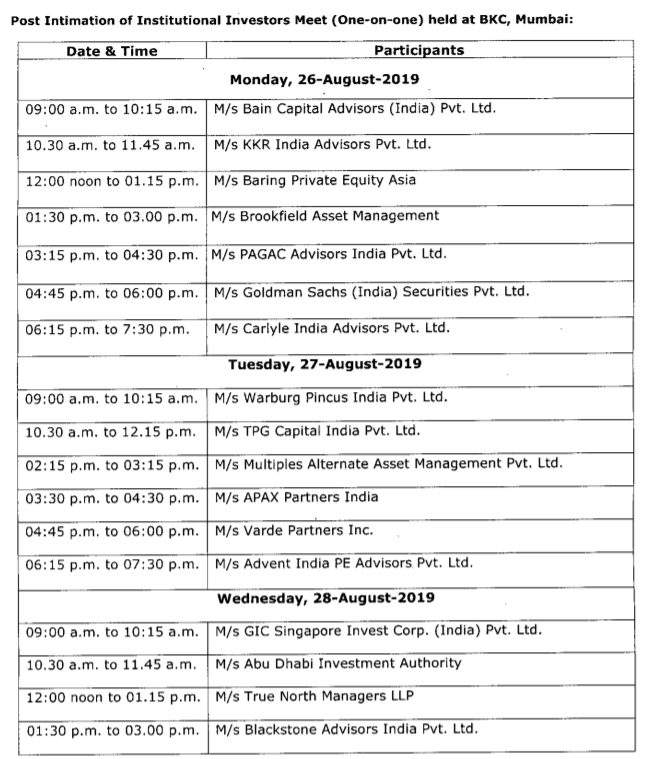

Will they as much good interest they saw during the previous attempt in Jan - Mar 2018? If one compares the stock price, many firms would be interested at sub 400 levels, as it is around 3 P/B. The below screenshot is about meeting with (perhaps potential bidders) in the last week of August. Similar thing happened in end of Jan 2018 as well.

Also a bit strange to bring in a new MD right when Canara bank decides to sell it’s entire management stake…The new management (if the sale goes through) would like to have their own MD (especially when the newly appointed is in fact totally new to the company)

Whats the reason behind using an 80 day and 140 day ma

A news article says Canara bank CEO says he expects Rs.1000 crores from Canfin homes stake sale. 1000 crores for 30% comes to Rs.250 per share. Perhaps it was mis-quoted?

Mis quote for sure no doubt about it