I am not sure. You are assuming that the book size would increase by ~25% by Q4 FY19 and yet the run-off amount would remain the same as in Q4 FY18. That is a decrease of 25% in the run-off rate during FY19. At the same run-off rate, the run-off amount for FY19 would be approximately 2800 crs* (1+1.25) / 2 = 3150 crs. This gives you a disbursement requirement of ~6900 crs. I think that ~7000 crs can be a reasonable estimate. (numbers revised.)

Reg, the loan book growth at 25%, it is not my assumption but is the target given by Canfin management in their investor presentation. I don’t know if they will achieve.

As far as pre/repayments/loan transfers are concerned, the quarterly (calculated) number for the last 3 quarters have been at 700, 720 and 700 crores. They have been increasing till mid 2017 with all psu banks reducing home loan rates drastically but kinda steadied off late. Also as the interest rates have turned up recently and also as Canfin has this annual re-setting of interest rates to its customers, I do expect loan transfers to other banks / hfcs will be much lesser and I assume the total of such pre/repayment / loan transfers would hover around 700 crores per quarter for next 1 year. Even if it is higher, I guess the average per quarter would be around 725 crores. Hence the disbursements figure of 6600 odd crores for next year

Dude! take it easy on me.

My thoughts do not cause the CanFin stock to go down. I just shared my opinion, which you often solicit. I know that people who visit a thread are likely invested in the stock. So, if I say nice things about the company, then I would be appreciated more. But, I have the bad habit of saying what I think is true.

Good luck!

1 Like

Sorry if I gave a wrong impression

I really didn’t mean anything wrong. I just like such discussions and listening / sharing different opinions. Think I know you since long time from Canfin forum in MMB. Please excuse if I gave a different impression.

Not much new info from con-call. While confident of 24% loan book growth for FY19, MD also cautions about growth in Q1 due to Karnataka election impact.

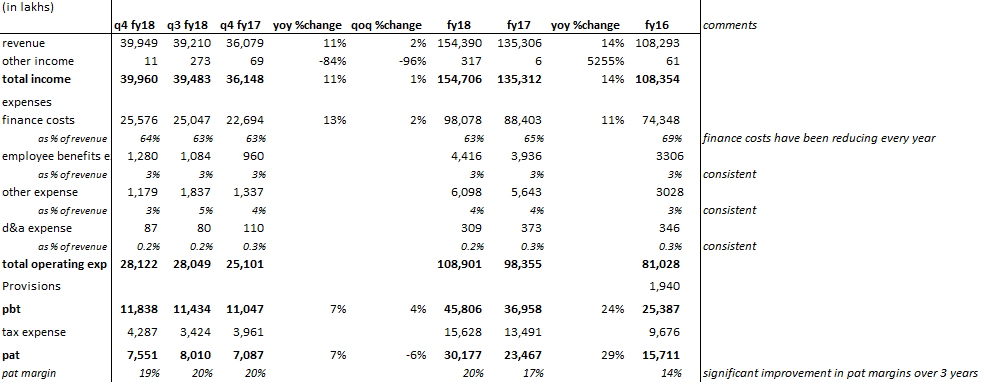

a snapshot of financials quarterly and annually

what is encouraging here is the annual trend in finance costs…they have dropped significantly from 69% in fy16 to 63% now…also, all other costs have been kept steady over the years…the positive impact of this can be seen on pat margins that have improved from 14% in fy16 to 20% in fy18. if the company is successfully able to expand its network this yr to 190 as promised and the karnataka market picks up, this could play out to be a very good story with these kind of margins…fingers crossed.

disclosure: invested

1 Like

The average yield as on FY17 (Mar 2017) was 10.96% and since then it has changed as below.

Q1 FY18 - 10.59 %

Q2 FY18 - 10.51 %

Q3 FY18 - 10.39 %

Q4 FY18 - 10.33 %

Till Q1 FY18, the lending rates started at 8.95% and from July 1st, 2017 to Mar 31, 2018, it was reduced to 8.5%. From Apr 1, 2018, the starting rates are again back to 8.95%.

Last year, Canfin also introduced automatic re-setting of interest rates at one time nominal cost to retain customers and avoid balance transfers.

Now that the lending rates are increased, how do we calculate the average yield for the current quarter (Q1FY19)?

For the previous quarter, it was 10.33%.

Can we assume the interest rates for the existing borrowers (loan book of 15743 crores - any repayments) to increase by 0.45% - for those whose interest rates were reduced in the last 3 quarters?

Comparing the performance of Canfin against that of Gruh,

| 2018 Vs 2017 | Gruh | Canfin |

|---|---|---|

| Disbursements Growth YOY | 27.48 | 8.66 |

| Loan Assets Growth YOY | 17.54 | 18.25 |

| NIM Growth YOY | 23.73 | 20.79 |

| PBT Growth YOY | 27.15 | 23.74 |

| PAT Growth YOY | 22.37 | 28.26 |

| P/E | 60.42 | 18.97 |

| P/BV | 15.87 | 4.26 |

| Gross NPA | 0.45 | 0.43 |

| Net NPA | 0 | 0.20 |

| Cost to Income Ratio % | 14.16 | 15.21 |

| Capital Adequacy Ratio (CAR) | 18.9 | 19.07 |

| NIM to ATA % | 4.4 | 3.53 |

| ROE | 29 | 22.41 |

| ROA | 2.45 | 2.09 |

Gruh’s consistency and predictability over long time horizon is richly rewarded by the market. Canfin too looks reasonably okay, with the exception of Disbursement Growth YOY. I would give Canfin couple of more quarters to see how the results pan out before deciding to act…

Disclosure: Holding both Gruh and Canfin…

14 Likes

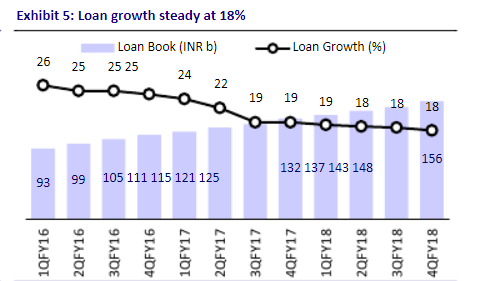

Canfin seems to be following in the lines of Gruh. As Mr.Hota mentioned in many con-calls, when the market condition is not good, better to adjust to it by slowing growth and focussing on quality. Below pic shows Gruh’s loan book growth also came down from 26% to 19% and is steady around there. And market is treating them well. One thing Mr. Hota can do differently is give a lower loan book target matching his own statements as mentioned above. For FY19, they have set a growth target of 24% whereas in the con-call he says Q1 will be slower in Karnataka (their 50% book) due to elections. I would have been happy if they had set target of 19% instead of 24% for Fy19 and then aim to beat that target. But for that, all operational & return metrics of Canfin is comparable to Gruh. Hopefully they are able to maintain / improve the asset quality levels.

7 Likes

Interesting that so many mutual funds are meeting Canfin Management.

Something’s brewing at Canfin homes…

(1) Meeting with lot of MF and Institutional investors on Monday, Tuesday

(2) In addition to 50 DSA on contract, they plan to recruit additional 125 Junior officers on contract for 1 year with starting salary of 2.4 lacs

(3) Additional office spaces required in 28 locations with majority in Maharashtra, UP, Gujarat etc as against their plan to open only 20 new branches.

3 Likes

A general question (to Keki Mistry, if he gets to see this):

Mr. Mistry had been repeatedly saying that they will acquire a HFC or an Insurance company at the “RIGHT VALUATIONS”

Even if Canara bank was expecting Rs.750 per share (hypothetically speaking), it would be 7.5 times the book value of Rs. 100. If market rumors are to be believed, their offer price was around 500 to 550, which is 5 to 5.5 times Price to Book.

Now I look at Gruh finance, which is above Rs. 700 per share and is trading more than 20 times its book value. If for some reason, HDFC wants to sell some stake in GRUH, would they be selling at 20 times book or 5 to 7.5 times its book value

Would have been good if he had thought about it when they made the offer to Canara bank.

1 Like

My 2 cents there lot of difference in gruh, that’s y market is valuing gruh very highly pedigree

Canfin’s operational metrics are quite good as well and hence much interest. If HDFC had seen long term value, they could have offered some additional premium as it is still a small company. Their investment would have multiplied in the short to long term

Quality of loan book also matters, gruh has reached in most minute areas I mean to say majority of their loan is to where population is between 50000 to 100000

Agree. They have carved their own niche market segment where others like Repco are struggling. I am still trying to figure the exact segment which Canfin is targetting. They say it is LIG & MIG-1 but HDFC itself is targetting these since last few quarters. That was perhaps a reason why they were interested in buying Canfin homes.

Is Canfin beginning to get attractive at CMP which is just above 3 times Price to book on FY19 basis?

At Rs.375 per share, it would be 3 times book on FY19E book value of Rs.125 (without considering any fund raise activity)

Caladium investments (part of GIC Singapore) still holds 13.45% that they bought last year at Rs.420 per share.

2 Likes

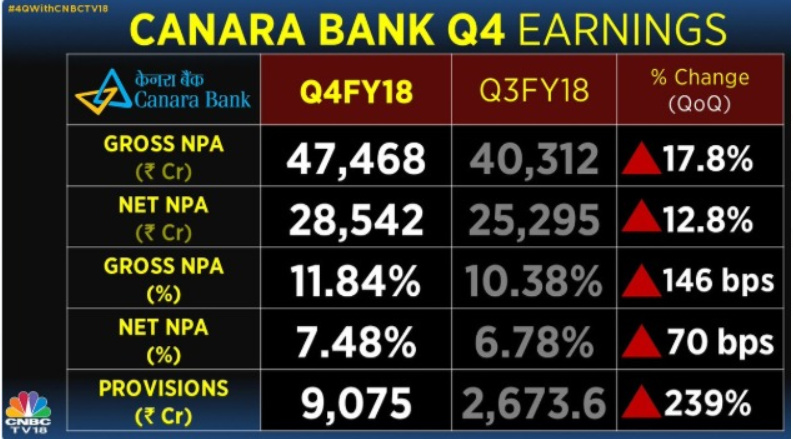

Canara bank has reported a really bad Q4. For them to subscribe to Canfin Homes Rights issue looks very difficult.

Perhaps this will revive the stake sale idea?

2 Likes

Canara Bank plans to raise up to Rs 5,000 crore by end of first half of FY19

(But not by selling stake in Canfin homes, which looks to be happening only next fiscal)

In March end, Canara Bank had called off the stake sale in Can Fin Homes after bid offers by several interested entities were not in tune with the expected valuation. Sharma said the offer was above market price but below our expectation as we have an 8-10 percent “management premium” which the bidders did not agree to.

“We have now posted a full-time deputy managing director to strengthen the company further, improve its performance, profitability and accordingly give value to the shareholders… Also, because we are sufficiently well capitalized, we do not have the urgency to sell off that subsidiary but will look at other smaller businesses,” Sharma further elaborated.

1 Like

simple reason that market was anticipating that some big ticket player will take stake from Canara Bank, but that has not happened. So market wants to bring valuation to actual growth rate in last one year (which is very very low)

2 Likes