good to know. where did you find the information on office space required?

Announcements / News sections in company website.

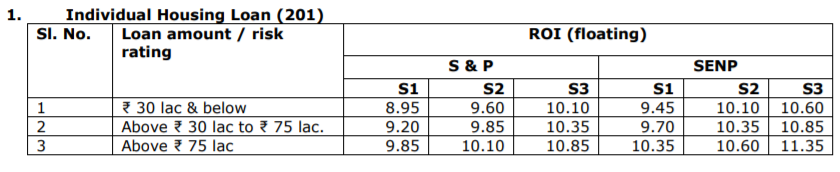

The home loan rate was 8.95% on the website till sometime ago. It now reads 8.5% onwards. Smart move since most of their clientele is salaried class who do their homework on the internet before deciding where to go. They probably don’t want to turn away customers by advertising a higher rate. So “8.5% onwards” make sense as they can finalise the rate based on the customer’s creditworthiness.

1 Like

This was the point I had asked the management in the 4Q Concall. Their reply was that they have always offered loans at a premium to market - and sounded confident to continue to do so.

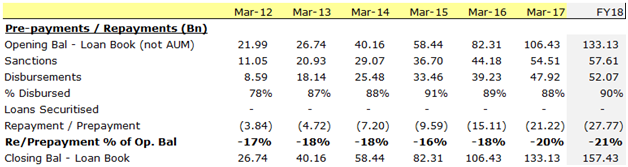

I still do think this is a key monitorable - as can be seen from the table below. Repayments as % of Opening Loan Book has steadily risen over the years - and has now reached 21%

Lets Check whether what the management says is true or know. The way we can do this is to Plot the Yields on Loans provided all HFC’s from Say 2014 to 2018. They are available in the presentations. We can then see the trend in 2 ways

-

What are the absolute yields of the HFC’s over the years

-

Fall in yields by HFC’s - If Canfin has less sensitive customers - drop in yields will be less severe.

By the way - when you click the link below Housing loan products on the website - It takes us to the page detailing the various products - which still mentions 8.95%. Given that the genuine home buyer is smart - he may not fall for the lure. Link given below.

http://www.canfinhomes.com/canfinhomes.php?page=housingloans

1 Like

@jainnitinp, @ronak

There are few special affordable housing loans which are offered at 8.5% fixed for 3 years as shown below. If you leave them out, the home loans start at 8.95%

1 Like

Given that a large part of their loan book is focused on AHL, the 8.5% for AHL bodes well.

Another key parameter for growth in this business is network expansion - both in terms of location and feet on the ground. Given that the company has published an advt. for 125 new officers and 28 new locations, we should expect the network expanding significantly in the coming qtrs. I’m hopeful of growth returning in q2 fy19 after the karnataka election dust has settled and the new network is in place.

Great… I wish for the same, that growth rebounds for this company.

Just one more thing, the GRHS & LUH referred to above constitutes a miniscule portion of the overall housing - I vaguely remember the figure to be not more than 12% of the total loan book (Will confirm from the transcripts).

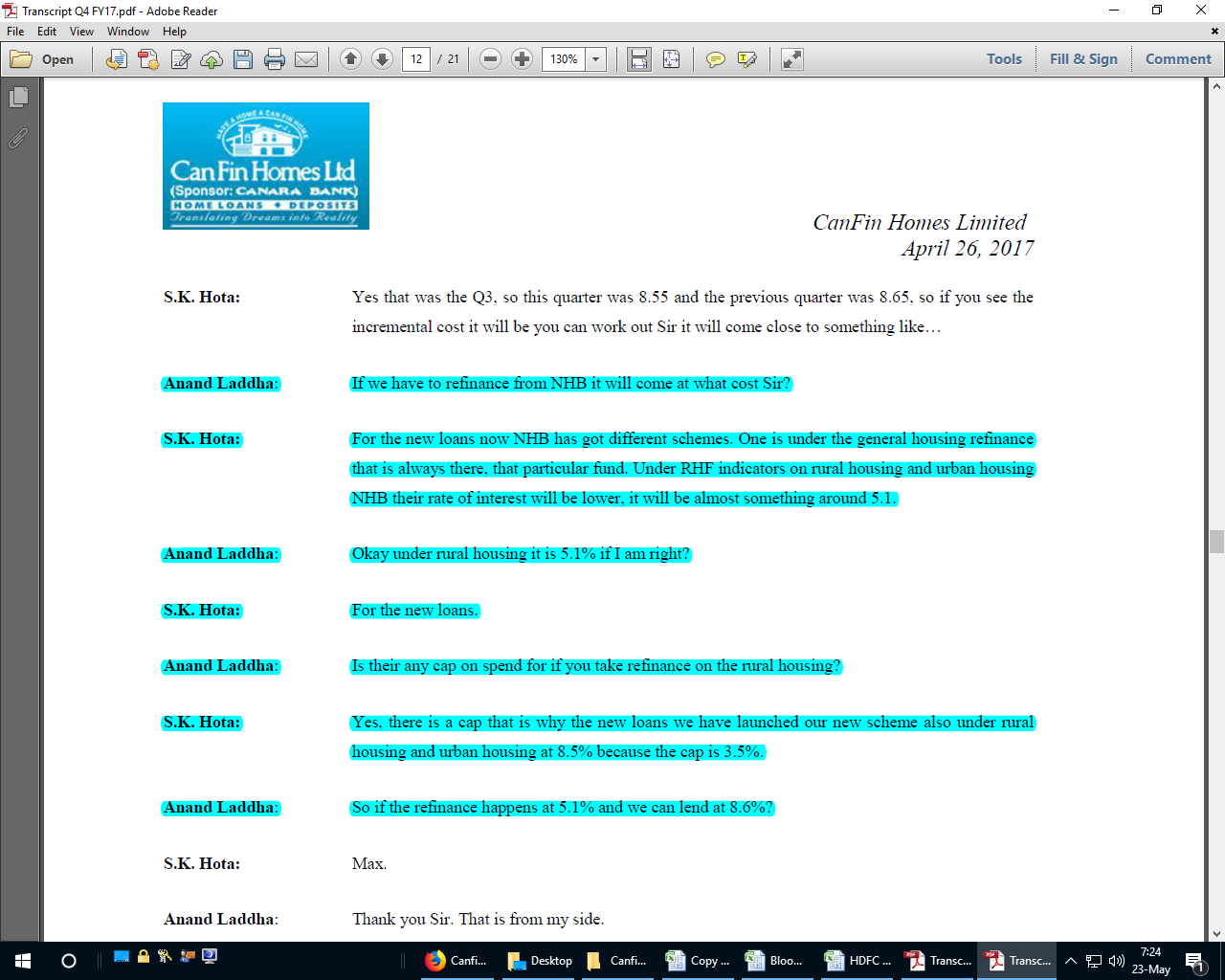

So if this segment picks up - it will be a huge positive for the company as these are higher spread loans - Co gets the funding for these loans from NHB @ fixed 5.1% (Excerpts from the Apr 2017 Concall)

1 Like

Hello fellow investors

My thoughts on CanFin and other HFCs in general are that housing finance will most likely see subdued growth in share price in the near future because

-

Interest Rate cycle seems to have bottomed out with multiple indicators (such as Inflation, Crude prices, rate increase by US FOMC) pointing towards likely increase in rates by RBI.

-

Increase in competition with many new private lenders in the market and older players such as ICICI, SBI going aggressive on retail loans such as home loans.

-

Valuations multiples have increased. 3-4 Years back most HFC were trading at 1-2 times book value but now so many are trading st more than 3-4-5 times book value.

All of the above factors can work simultaneously can cause a strong slowdown especially 1) interest rate cycle.

I remember Mr Basant Maheshwari saying once in an interview on TV that the demand of housing is very elastic, in the sense many people defer housing purchase decisions based on price. So there will always be bunching of demand in a space of few years.

It is interesting also to compare the trends in the period from 2010 to 2013 when RBI had continuously increased repo rate from ~4% to ~8%.

If news of reduction of interest rate by Can Fin to start from 8.5% is true it is a further indicator that margins are getting squeeze and therefore profitability on existing loans will fall.

However in the long term I am very bullish on HFC since mortgage market in India is very under penetrated and a combination of good volume growth, good NIM and control over credit costs means a steady compounder of book value. I only feel it will be wise not to buy at the current time.

Disclosure- I am holding small position in CanFin which I bought in 2017.

5 Likes

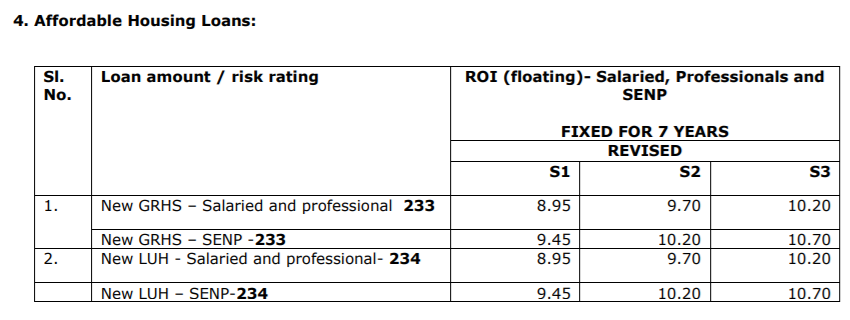

Canfin has revised the affordable housing loans upwards by keeping it fixed at 8.9% for 7 years now as compared to 8.5% fixed for 3 years earlier.

Would be interesting to see what they decide on the board meeting on their fund raising plans. Best to go with QIP I guess.

1 Like

Looks like company is trying to raise significant amount of money. How often does company raise this large an amount? How is it going to affect the growth, will the raised money be immediately utilized? or will it be done over the time? Can some one throw some detail? How does it work?

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=c4abc715-dd7f-4013-8d46-0ab8eee13491

Thanks-Mahesh

raising of funds is an enabling provision. if and when it materializes, it would imply resumption of growth for canfin. That’s the key trigger.

If am not wrong, one year ago itself they had made this enabling provision to raise NCD upto 6000 crores and equity upto 1000 crores via rights issue. Not sure why they are doing the same again. Is there a validity period for such resolutions?

Also, they mention raising funds upto 6000 crores debt & 1000 crores equity. It is not necessary that they raise the said amount and it could be lesser. I am more interested in the equity part and how much they would end up raising and in what format. I would personally prefer QIP with a strong institution.

Looks like situation in Bangalore / Karnataka has not improved but getting worse

The below report dated today says 685 projects under investigation…

RERA website shows 936 projects under investigation. This is almost double the number from January…

1 Like

One of the objectives of the fund raise plan is to explore acquisition opportunities???

“This special resolution enables the Board to issue Securities for an aggregate amount not exceeding `1000 Crores or its equivalent in any foreign currency.The Board shall issue Securities pursuant to this special resolution and utilize the proceeds for business purposes, including but not limited to meet capital expenditure and working capitalrequirements of the Company, repayment of debt, exploring acquisition opportunities and general corporate purposes”

Also, it looks like they will skip the rights issue and go ahead with a combo of QIP and Preferential allot to Canara bank (so they can maintain their 30% stake). If so, it is finally some good move from management…

"Considering the cost, benefit, requirement of time etc., with reference to each of the alternative modes of raising funds to improve the Leverage Ratio of the Company, the Board has now recommended to raise funds not exceeding ₹1,000 Crore, through any/mix of Right Issue already permitted and/or allotment of shares through QIP mode and/or preferential shares to promoters so that the shareholding percentage of promoters will remain the same pre and post issue of preferential shares and/or QIP"

Company has appointed 18 marketing officers and 103 junior officers. However, appointments happened towards the end of Q1. So benefit would most likely trickle in by the end of Q2 or Q3. No update yet though on the new locations proposed.

I think this noise is unnecessary. I think we should focus on what happened to Canfin in last 1 year, are they facing a lot more competition, are they just taking a quick stop in the marathon to energize? or something seriously wrong with the new management? How does future look? Is anyone planning to attend AGM to uncode all this? I think if we collectively channelise our energy to analyse better, it shall serve everyones purpose.

10 Likes

Hi,

If anyone is attending the AGM, I would be happy to compile my list of questionnaire we can put forward to the management. Guys attending can address it. I will compile the same by Wednesday.

Hi Guys,

Some unnecessary posts have been deleted.

Before making any post, please pause a moment to decide whether your post is adding value to the ongoing discussion. Let us all maintain focus on the business. The forum is about discussing pros and cons about the business and way forward. It is NOT about opinions of investors and/or sitting in judgement on anyone.

That is not our job, and it serves no useful purpose other than cluttering up the thread. Members should be mindful how the quality of discussion deteriorates - by such actions - and how thankless the job of Moderators is.

Thanks for your co-operation.

10 Likes