Can you share the source for this news?

What could be the future of Can Fin Homes when the sale is not done? Valuations drop. If results are bad, then it could be worse as well.

There’s complete silence here post Can Fin stake sale not working out, BM selling stake etc. India bulls Housing and gruh Finance results have been pretty good. Any estimates for Can Fin Homes

Any long-term investors jittery…

Salil

Canfin, the race horse (I still dont want to term it “of the past”) seems to be at a crucial juncture now:

- Catering to the niche segment - same as that of Gruh, however operating in a different geography. It is important to know if the specific geographical market has revived for Canfin to perform at the same level of Gruh.

- Promoter not focused - firefighting as it is mired in loan default, corruption controversy affecting PSBs in general.

- Desperate to sell off non-core assets including Canfin.

- PSB parentage affecting sentiment - No angel investor nor Sanjay Gupta as in PNBHF

- Misfired Stake Sale by parent and atleast the management / staff partially not focused in performance. Lot of smoke with no fire. Dampened the entire sentiment towards revival.

- Confusion on Capital infusion - Lending needs capital - Parent bank more interested in taking care of itself.

- No clarity on rights issue (announced some time back).

- Concerns on Asset Liability Mismatch in a scenario of rising interests.

- Most importantly - Missing its own guidance multiple times

Though BM may have his own justification for dumping Canfin and moving on, a couple of his statements are thought provoking

The results due on 28th Apr if good, may offer some solace, however, the long term concerns listed here needs to be addressed if it is to regain the past sentiments (and value) in my honest opinion.

Discl: Invested

1 Like

Very well articulated. Canfin has been a star for the last 4/5 years and suddenly showing a decline on a YOY basis.It is a big lesson to all of us.What has changed: 1. Management is weak.2 Competition is increasing.3. Inherent B/S mismatch 4.Loan growth tapering off 5.In a market where opportunity costs are high- it is sad Canfin will be a loser.

Disc: invested

1 Like

Thank you

What is the logic to remain invested in case of such negative aspects? Looking for a rally to exit?

Salil

Did Canfin miss its guidance twice in this year?

I guess they had never given quarterly guidance , only one given was annual Loan Book targets.

And during Q2 results they told that it will be met however in Q3 they revised it.

So technically its missing that only once. Hopefully they achieve the revised one with Q4 results.

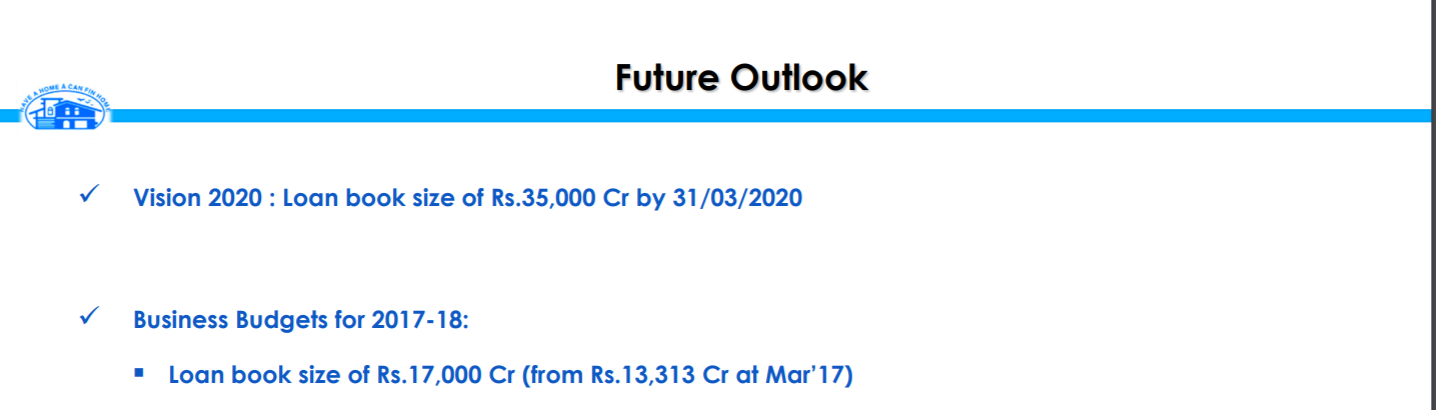

Q1 2018 Inv Presentation Highlights - Future Outlook

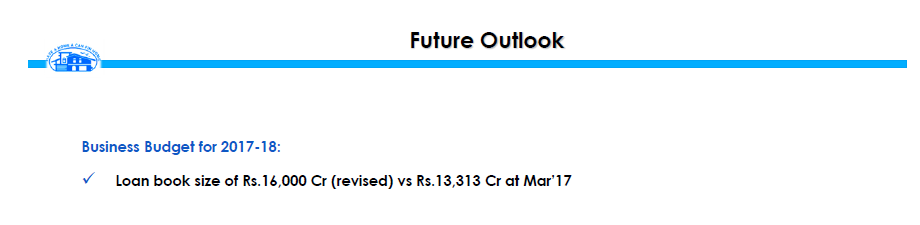

Q3 2018 Inv Presentation Highlights - Future Outlook

BM was right on missing guidance twice over. At this rate Canfin is sure to miss the Vision 2020 target as well, unless there is some magical turnaround in RE sector.

The reason why am still invested?. Not as agile as BM to dump it at the right moment. Waiting for the Ann results . Now want to see if some of these analysts are right.

Canfin - Edel - Q3 2018.pdf (243.2 KB)

Do you mean they will miss the revised guidance of 16000 crores in Q4? Even if so, how would BM know about it?

Gruh had a great Q4, their loan book grew by 750 crores QoQ and their GNPA came down from 0.73% to 0.45%. Both Canfin and Gruh had similar growth patterns in the recent past. Going by that (and hopefully no distractions to the employees in Q4 due to stake sale process) the loan book growth and asset quality levels should be good in Q4.

Take a guess looking at the trend whether they will miss or not the revised guidance of 16000 Crores.

As I mentioned in my earlier note, though they got similar profiles, erstwhile Gujarat Rural Housing Finance, caters to a different Geography, Canfin is dominant in Karnataka and Southern states, which is one of the worst affected market due to DeMon, RERA, GST, the recovery and growth patterns for these markets are not comparable. I would love to be wrong here though.

Please compare the quarterly growth pattern for Gruh as well and you will notice to be in similar lines. In the Q3 concall, Mr.Hota has mentioned that RERA approvals have increased in Karnataka and Chennai is also stabilising. Moreover, March month generally sees higher approvals and disbursements. Along with this, if other regions also have stabilized as per growth seen in Gruh, achieving 16000 crores shouldn’t be impossible. Gruh MD also mentioned that in Q4, growth mainly came from disbursals under PMAY scheme, which is also the main segment for Canfin. My main concern is if the management and field teams morale was impacted in Q4 due to the stake sale process.

Besides, the loan book guidance of 16000 crores by Mar 2018 was given on Jan 23, 2018. So, hopefully they have done a proper calculation as it was just 2 months before.

See below given article which talks about growth in residential sales especially in Mumbai & Bangalore. Gruh has 25% of its branches in Maharashtra and close to 10% in Karnataka. Canfin gets 35% business from Bangalore / Karnataka and both states have shown growth. You can also look at Sobha’s Q4 results where clearly they could sell more properties in Bangalore in the quarter gone by. So I the market conditions have been good. The question is if Canfin was able to capitalize without getting distracted in the stake sale / due diligence processes in Q4. The main difference between GRUH & CANFIN is that GRUH tends to the non-salaried class more as they focus on EWS & LIG whereas CANFIN focuses on salaried class in the LIG & MIG segments. So GRUH gets a better NIM due to the higher yields than CANFIN but also manages their asset quality well.

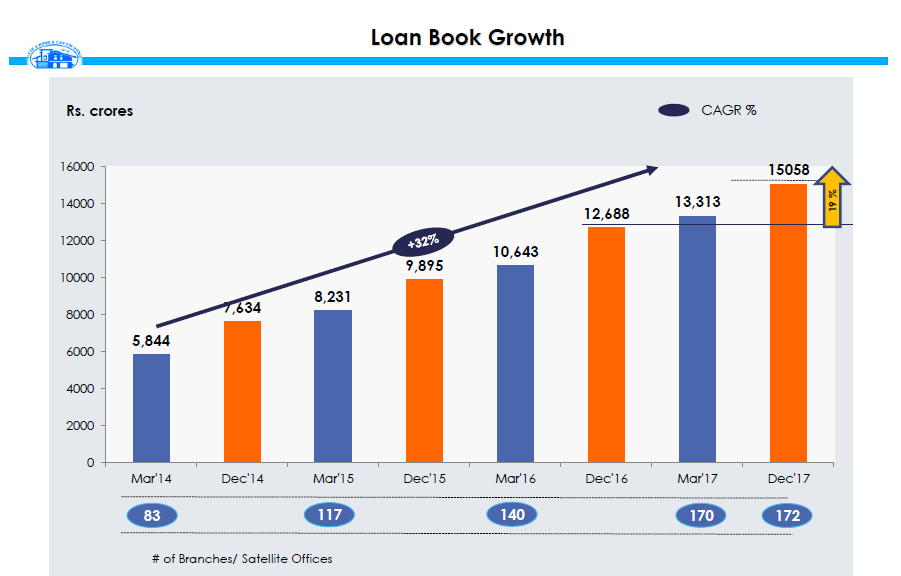

Also have a look at the loan book CAGR of GRUH, which is quite similar to that of Canfin (In fact, Canfin’s growth had been better)

Stake sale was being led by Canara Bank mgmt per the CEO’s interview. Can Fin mgmt was not involved. Hence, no question of them being distracted in stake sale.

Quarterly results are out today - results are quite weak (EPS growth of just around 6.4% QoQ). I think this is what the market has been pricing in as well for quite some time now.

The Quarterly EPS #'s and the Yearly EPS #'s are not matching up. Hope someone can clarify…Quarterly #'s are below:

Q1 EPS - 5.35

Q2 EPS - 5.63

Q3 EPS - 3.01 (This was earlier reported as 6.02, but now cut by half. Not sure if there was a stock split)…

Q4 EPS - 2.83

Summing it up, yearly EPS works out to 16.82. However, the report claims it to be 22.67.

Will wait for the detailed presentation with details on disbursements and other metrics before deciding on next steps (Trimming down Vs Selling off with loss).

Thanks,

Yearly EPS is 22.67 (301/13.3). There is no mention of NPA details

You need to double up EPS for Q3 and Q4 for share split.

I think share split from rs 10fv to rs 2fv (face value).adjusted EPs should use 1/5.

Updaed result reported.

In furtherance to our letter, we have attached the revised results. The corrections made relate to ; `Revenue from Operations’’ may please be read as Rs.39943.86 lakh’’; Paid up equity share capital of Rs.2663.31 lakh includes Rs.0.23 lakh forfeited shares; EPS for 3 months ended 31/03/18 is Rs.5.67; EPS for preceding 3 months ended 31/12/17 is Rs.6.02 and EPS for the corresponding 3 months ended 31/03/17 is Rs.5.32.