Fellow members I’ve a genuine query.

If this isn’t the appropriate thread for posting this question please guide me to the right one.

In my myopic view the major factor for home loan selection is the interest rate.

Is there any other factor/s that play crucial roles.

If it’s only the interest rate that matters the company offering cheapest rates will emerge victorious,right?

Yet again, if this is the wrong thread to post this question please guide me.

there are many factors… ease of getting loan, documentation required, willingness to give loans, location, turnaround times… apart from marketing and sales.

Also, I do not think every consumer is aware enough of the interest rates offered by all.

Interest rate is the main factor. However flexibility can be a consideration as well. For example Bajaj Finance gives you a loan account to which you can transfer excess cash you have and reduce the interest payment, you can then transfer the money back to your bank account if you need it say after a couple of months. It is more like a Overdraft loan at the interest rate of a mortgage.All this is done online. Again does your HFC allow you to make pre-payments online or do you have to visit a branch? How fast is the processing and disbursal

1 Like

Valid question.

When I did my one and only home loan process in addition to the interest rate, I was more concerned about the safety of any document which I submit to the lender. There were stories of one PSU bank and another private sector bank mis-handling the documents leading to the loss of papers. I did not want to end up in such a trouble and went for HDFC considering the trust I had in them.

Secondly, the service quality also matters and the ability to connect with the institution and get certain exceptions when you really require them would create a good impression. Most of the time, people will go to a lender based on what their friends, family members or advisors recommend based on their experience.

1 Like

Many thanks for the responses.

The factors that play a crucial role in lender selection in no particular order

2) Willingness to lend

3) Customer service

4) Document safety

5) Reputation

I’m of the understanding that leading lenders are inundated with creditworthy applications. Hence, they can be choosy.

Those who don’t meet the requirements of top lenders may opt for NBFCs who may not be as stringent because they desire to expand their loan book. Currently, around 80% of the lending is done by 5 leading HFCs and they’ve done fairly well at curbing NPAs.

Now, there can only be so many truly credit worthy applicants. As the country grows, youth are inducted in the work force very few people will earn enough money to be able to meet the expectations of the elite housing finance companies.

So, either top HFCs will dilute their requirements, increasing risk for loan going bad. Or the demand for NBFCs will go up.

And, there’s a higher risk of bad loans.

Or lending institutions refuse to lend to borrowers with questionable profiles. This in turn will adversely impact the housing sector.

Hence, in my humble opinion, creation of good quality jobs and enterprises is key to flourishing of this sector.

If quality job creation doesn’t occur lending may not reduce but the quality of loan book will without a doubt deteriorate, significantly.

1 Like

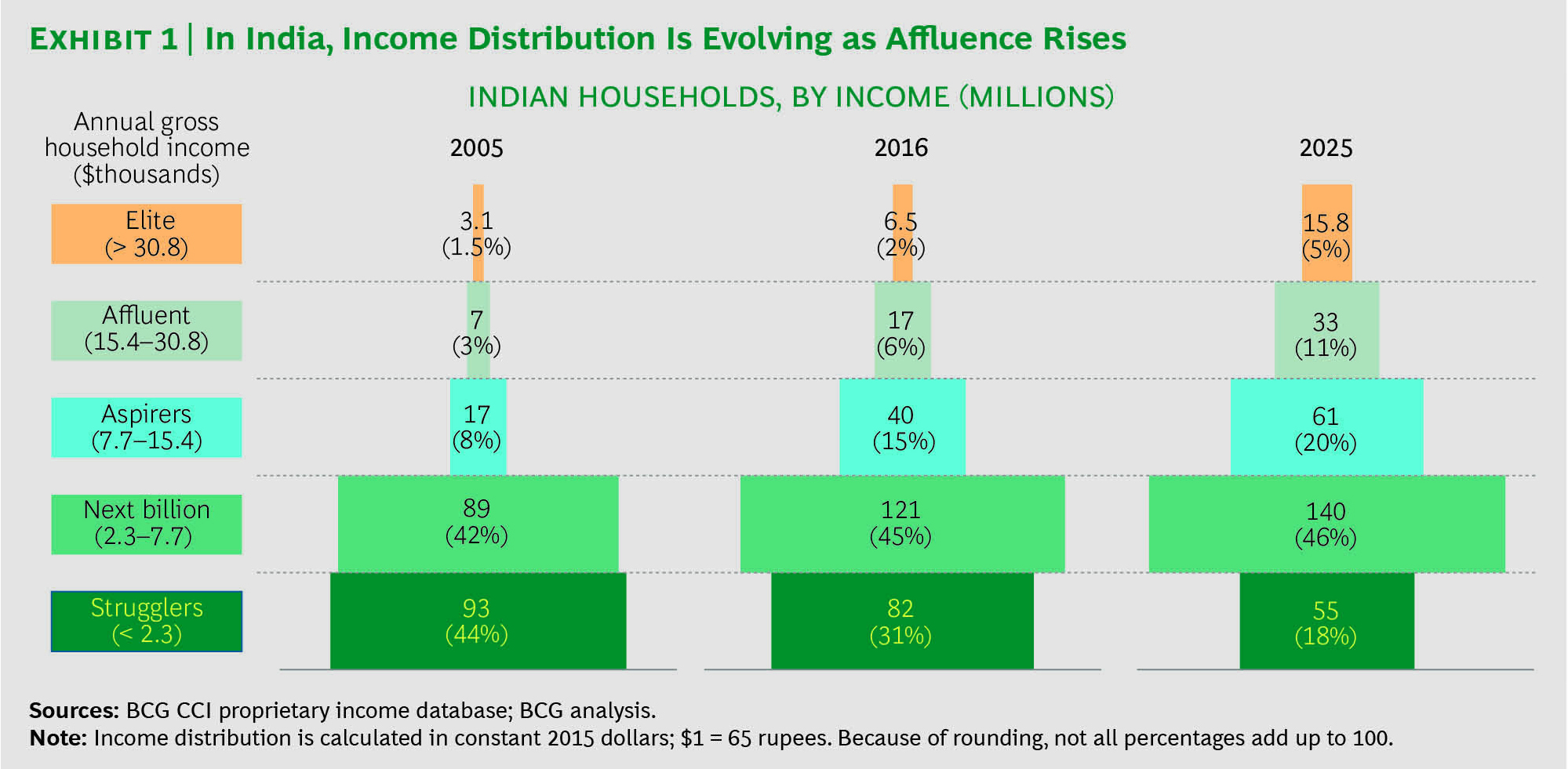

What you are saying is against the consensus. I am pasting BCG’s population segregation based on income for India.

The first two categories i.e. Elite and Affluent are the most creditworthy and contribute something like 70% to the consumption credit off take. If Elite and Affluent population doubles in size by 2025 as projected the pool of creditworthy applicants will continue to grow and there wont be any shortage. Another factor is some of the new players are aggressively wooing existing customers of PSUs (and some private banks as well)with better service for balance transfers. Remember the existing customers have been paying their EMIs for say 5-6 years so their credentials are well established. You can of course disagree with BCG on the income distribution projections.

1 Like

Dear all, now this thread has gone on a different tangent again.

The topic may have some significance to all hfcs. However, in the larger interest of Canfin, can we not start a thread for this discussion.,

As much as I’d like to participate in a discussion, it’d be wrong to inundate the thread with non Canfin relevant information.

As @adityajp mentioned maybe another thread can be initiated.

Perhaps other HFCs and Banks will follow suit…first Canfin, now HDFC increasing lending rates…

Canara bank may come under PCA. Can this put pressure on them to sell Canfin stake?

This is not about BM and his picks, how ever the pointers he and others makes needs a discussion.

Companies that miss guidance deserve no mercy

Basant was also irked by the fact that Can Fin Homes was playing hard-to-get despite missing earnings guidance.

“And a company that misses its guidance twice a year is like a student who fails an open book test. He gets no mercy,” he fumed.

1 Like

Interesting. Canfin is selling at a price to book of 4.6 times lesser only to Gruh Finance. I hope those who have done calculations on book value growth, will also take into account that price to book could be revised downwards in the absence of growth.

Hopefully the lull created by RERA is going away…

If you look at PNB Housing & Repco, they also trade at a P/B range of 3 to 4 times.

PNB Housing has amazing loan book growth but on all other parameters like NPA, RoA, RoE etc, they are at same level of Canfin or little lower.

Repco’s parameters are lower in all aspects when compared to Canfin. Slow growth, high NPA mainly. But still trades between 3 to 4 times.

So, why shouldn’t Canfin be available at a higher premium to these two when all its parameters are very good. Even the loan book growth is around 20%, which is the same as that of Gruh. On an 1 year forward book basis (BV of 125), at CMP, the P/B is 3.5

So, it doesn’t look overvalued even at a loan book growth rate of 20%. Let’s wait till Q4 results to see growth commentary. But then, Q4 could have been impacted as an one-time thing due to management being busy with the stake sale process.

1 Like

I think this report needs to be taken with a pinch of salt as NCR definitely is no to seeing in pick up and so is the case with pune

I agree. I also see this news today where Karnataka RERA had issued provisional approval earlier to 500+ projects, with which the builders have started the work by collecting money from buyers. Now RERA says they have to get permanent approval. Quite strange…

The winners in this sector are going to be decided by how the competitors are able to handle increased competition. There is going to be growth in this sector and NPAs are going to be fairly low, but at the same time there is going to be competition and pricing pressure because entry barriers are low. If this is going to be the case I would bet on a management backed by Carlyle (PNBHF) over a PSU management to handle the increased competition. So market will give some discount for the PSU management.

Perhaps.

But ultimately, it will be the business performance. If the loan book growth comes back, then PSU management or not - does it matter? This is clearly visible from the share price performance since 2013.

Also note, that growth (relatively) slowed down only after DEMO / RERA. Once that impact is over, we need to see how the business performs.

Your question was why shouldn’t Canfin get a premium so the reason might be that the market thinks it might lag behind the likes of PNBHF in the future because of the difference in management pedigree. Whatever has happened in the past (2013) doesn’t matter now. Valuations are decided by perceptions about future growth. Whenever private players have entered a space dominated by PSUs the latter has lost market share. You can have a different view about this and feel that Canfin deserves a premium (perfectly justified) I was merely giving a reason why the market (not me) might think otherwise.

Sure, I was not challenging your views, just expressing my view

My reasoning was that all the growth Canfin had till now was also due to PSU management only, so why can’t they continue the same in the future as well. Naturally, a private company management would be better (provided they are of good quality ones). Let’s wait and see