Here is the BSE announcement

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/7ebcb846-ed25-4566-b972-18642debf64a.pdf

Nice growth both quarterly and yearly.

1 Like

Conference Call tomorrow

The results look good with primary contribution from lower finance cost and higher fees/charges which the management expected to happen in Q4 due to customers switching to lower ROI. But does anyone feel that the disbursement growth could have been better? Even Gruh posted higher QoQ disbursements. Having said that, the management seems to very confident about higher loan book growth for next year - from 13300 crores to 17000 crores, which is almost 3700 crore increase. To achieve that, they may have to disburse 6500 odd crores when looking at past trend.

Can fin in FY17 paid taxes at the level of closer to 37% whereas Gruh paid at closer to 33%. Any idea why there is a difference in taxation? Shouldn’t both be 34.61 % net? Any Clarification will be of great help

I fetlt the same, considering it the last quarter of financial year, I expected this quarter to be solid loan book growth, I dont knnow if it was strategic to slow a bit. However, they achieved what they had targeted for FY16-17, a 13500 Cr loan book. But operating performance and NIM improvements are very impressive.

Yep. But for the disbursement growth (which is not bad  ) everything else looks good. One aspect I am not able to get in detail is the difference between increase in loan book size in the last year compared to the full year disbursement. The loan book has grown by 2700 crores vs disbursement of 4800 Crores. Does anyone have a view on this?

) everything else looks good. One aspect I am not able to get in detail is the difference between increase in loan book size in the last year compared to the full year disbursement. The loan book has grown by 2700 crores vs disbursement of 4800 Crores. Does anyone have a view on this?

Roughly, 1/6 of the book runs every year. The average book size was ~12,000 crs during FY17. So, about 2,000 crs of loan book would have runoff during FY17. So, even though disbursements were 4,750 crores, the growth in loan book was 2,750 crores.

Increase in loan book (2,750) = Disbursements (4,750) - Runoff (2,000)

3 Likes

Thanks. So I guess they have to disburse roughly 6000 Crores to increase the loan book by 3700 Crores to meet 17000 Crores target for FY18. That doesn’t sound unreasonable, as it comes to average of 1500 crores per quarter when they are already doing 1200 crores even with the demonetization impact. Also I hope that the supply side in affordable housing increases. Gruh management was quite positive about future prospects based on affordable housing related activities being done by government.

MD Mr. Hota’s interview with ET now. He says Jan & Feb had seen some slump from demonetization and from March things got better. So hopefully disbursements increase moving forward. And they are still confident about 35000 Crores loan book by 2020. The answer to the last question shows their confidence. Of course, they are betting on the affordable housing push by the government - http://economictimes.indiatimes.com/markets/expert-view/we-will-achieve-our-target-of-rs-35k-crore-loan-book-by-2022-sarada-kumar-hota-md-ceo-can-fin-homes/articleshow/58375221.cms

1 Like

Is that the target by 2022? because they have to grow loan book 37% y-o-y if they want to achieve it by 2020.

35000 crore loan book target is part of their Vision 2020 statement. It is for FY20. To achieve that, they need to grow big, hence the questions in that interview and the response.

The guidance FY18 is 17000 loan book which is CAGR of 26% i think that is what he is driving towards and 35000 is more of vision.

To get to 35,000 Cr loan book by FY20 they will need a CAGR of 38%. If the target is to be achieved by FY 21, it will need a CAGR of 27%. Both are higher that their current run rate.

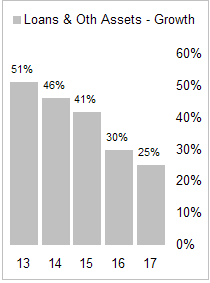

Not only current growth rate is lower than their own target, it is also decelerating. Growth in loan book has dropped from 51% in FY 13 to 25% in FY 17.

Source: Company IR Presentations.

With everyone getting into home loan business and targeting salaried home buyers, Canfin will have tough time growing at 25% let alone 38%.

16 Likes

Thank you Yogesh for putting together this data.

I think we need to look at 35K loan book by 2020 as a big long hairy ambitious goal. Mr. Hota has told twice in the last four earnings call that he is not worried about achieving this 2020 goal, and he would rather focus on ensuring that they achieve the goals set for every year. On the other hand the macro situation for the HFCs is not too bad. We have been hearing about many new HFCs coming into the game, banks pulling the housing loan accounts from HFCs and slowdown in the IT sector for few years now. One can argue that is the reason behind the loan book growth rate coming down for Canfin, but I am unsure about it. Following are some reasons why I find hard to accept this theory

1- The primary (target) customers of Canfin are not necessarily the IT people. It is salaried non IT class.

2- Last year everyone felt the pinch of Demonetization. The 25% growth by all means is great in such macro environment. Now I am not claiming that the growth in the current year would be better but I do not have any reason to believe it would not be.

3- The government interest subvention schemes for the affordable housing has created a good tail wind for the sector.

4- I do not expect that new HFCs who are setting up the shop now would overnight become a threat to existing HFCs. We need to look back to find out how much time it took for Gruh, Repco, PNB Housing and Canfin to become a sizeable HFC and reflect that learning on the perceived threat from new HFCs.

5- Banks snatching loan accounts from HFCs. I am sure that we would continue to hear even 2-3 years down the line. So far Canfin has not got impacted because of it.

Let us closely watch the loan book growth over the next two quarters and if indeed the growth would be less than 25% then accept it as new norm.

Cheers,

Krishna

10 Likes

lets not ignore the bottom line growth which was 41% and my guess is will be around same for next couple of quarters…and even if it does 20-25% top line growth it is not expensive PEG wise…how many stocks assure that kind of growth with that kind of valuation ?

Board to consider sub division of equity shares

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=c75914d3-4066-4510-851d-f14aa0036eb2

Wonder who the board is trying to attract with this stock split? At 2700, don’t know which retail folks can’t afford this - it’s not like Eicher Motors at 27k

Always believed that a stock split would lead to increased price volatility - so actually searched for it on Google and found this and it’s a proven fact

Anyway - the increased price volatility generally only plays into the hands of intelligent investors

1 Like

106171_AR_&_Notice.pdf (1.9 MB)

Surely Canfin Homes is moving slowly in league of HDFCs.

If I have 10 shares before stock split that I bought more than a year ago and now if it becomes 20 due to stock split, will the purchase date of the additional 10 shares be the same as that of the original 10 shares OR will the date on which the new 10 shares are allocated to our demat be the purchase date where I need to hold them for 1 year to avoid short term capital gains tax?