Today’s delivery percentage is 85.51% in NSE and 92.46% in BSE. Delivery % used to had around 45-55% range. At 1.72 lakh volume at CMP, this is not an illiquid stock either. Wondering what’s happening

Disclosure: Holding Can Fin and hence my views may be biased

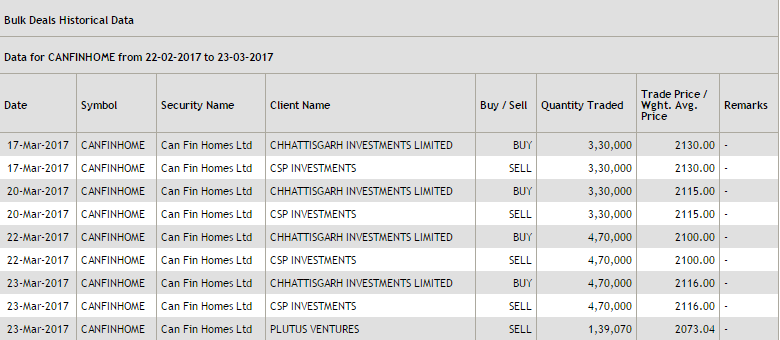

Another 4.7 Lakh shares changed hands today as similar to yesterday. Plus another seller Plutus Ventures. Will that be related to Chattisgarh Investments as well?

Does anyone feel that GIC is going to buy the entire Chattisgarh group company stake? That would make them majority shareholder with over 30% stake, even though not being a promoter.

Also, does anyone know what was today’s meeting about? The company says they had to relook at the NCD plan details to adhere to latest rules from NHB? Could it also be about placing the NCDs with GIC itself?

Won’t be surprised to see Chhattisgarh pare some stake. Buyer can be anybody.

@ayushmit and others - What is your view on NIMs and Interest Spreads going ahead and its impact on the stock?

I think NIMs have peaked out more or less and won’t be easy to expand further from here. NIMs and Interest Spreads may infact contract from here. Canfin benefitted a lot by changing its funding mix which resulted in much lower costs of funds for it. This might not be the case going ahead.

Cost of Funds curve may start flattening out (i.e. cost of funds may not fall as steeply as before) and home loan rates have fallen much faster in last few months (both on new and existing loans). Hence this may result in contracting margins and spreads.

Canfin would still continue to be a stable grower (despite a fall in NII and bottomline) but How do you think the above will impact going ahead?

The disclosure by Chattisgarh & CSP investments mase today is quite interesting.

It clearly shows both are partner firms

Looks like CSP has been holding close to 35 lakh shares, almost exactly 13.45% as similar to what GIC bought from Canara bank. As on date, CSP has sold almost half of that to Chattisgarh as of today and starting few days back

Bit curious about how CSP was able to hold 13.45% stake and the same is not available in the Dec 2016 SHP of canfin homes.

All these transactions are happening post GIc deal. And all put together, chattisgarh and group companies already owns 25% at the minimum. It could be well over or around 30%, if Aditya Mundra who holds 3% is also part of Sarda group. As all these are happening post GIC deal, wonder if they plan to sell their entire holding to GIC or perhaps and preferably / hopefully another big company.

There is also the 5% pledged share disclosure by Aditya Birla Finance in January. So total owned by Canara bank (31%), GIC (13.5), Chattisgarh group (25 to 30 %) and AB finance (5%) = around 80%. No wonder why it was an illiquid stock !!!.Wonder how much holding is really from retail investors like us as there are other MFs, NRI etc holding some stake.

Extract from disclosure to exchanges

" This is to inform that the Company has received intimations under Reg.29(1) & 29(2)of SEBI (SAST) Regulations, 2011on 24/03/2017; (1) from M/s. Chhattisgarh Investments Ltd. under Reg.29(1), that they have acquired 16,00,000 numbers of equity shares (6.01%) of the Company between 17/03/2017 to 23/03/2017 (last transaction on 23/03/2017), from sales made by partnership firm in which the said Company is a partner.(2) from M/s.CSP Investments (A partnership firm with – Chhattisgarh Investments Ltd., Sarda Agriculture & Properties Pvt.Ltd. and Prachi Agriculture & Properties Pvt.Ltd. as partners) under Reg.29(2), that they have sold 681114 (2.56%) equity shares and 802886 (3.02%) equity shares of the Company between 17/03/2017 and 22/03/2017 (last transaction on 22/03/2017,which have been purchased by one of the partners of the firm) and after sale the holding stands at 2094607 (7.87%)"

If you closely monitor, the PAN number of this “Chattisgarh Investments” is different from the “Chattisgarh Investments” from the december shareholding pattern. They are all part of the same group but parking the shares under different sub entities. I am not sure how this cross-selling helps them and they have been doing this for many years now. Interestingly, the disclosures are coming up only now.

If you look at the Dec SHP, there is no mention of CSP investments holding 13.45%.

Almost everything is overpriced at the moment. Gruh trading at 17 times, Can Fin at 7 times, pnb housing at 9 times, IB Housing at 4 times, HDFC at 4.8 times, Repco at 4.6 times. Those that are comparatively cheaper are GIC, Dewan, LIC Housing. But if you look at overall growth, risk profile and loan book quality, Can Fin is only next to Gruh/HDFC which is reflecting in the price now. We talk about Gruh being extremely costly at 8-9 p/b few years back, and look where it is trading now. Yes, this is bull market which is giving these good companies such price multiples. Rationale - Good run way, almost certain growth, good mgmt, good loan book quality, sectoral tailwinds. One of the major reasons this is rising so fast is on-boarding of new big investors.

Range of valuation depends upon the macros. A good company with sectoral tailwinds in bear market may command 2-3 times book value and seem like pricey. The same company, with similar prospects, in maddening bull market might command 7-8 times and still seem to be okay. ‘Semantics (Context)’ matters!

GIC Singapore’s subsidiary Caladium Investments has bought 13.45% stake at Rs.2105. As they are a very big global investment firm, I am sure they must have done their calculations buying such a big stake at such a price. That gives some confidence.

But this is not to say GIC had always been right with their investment rationale as they seem to have bought into US sub prime crisis and incurred losses.

Let’s just hope for the best.

30% stake of Canara Bank and over 20% stake of Sarda Group make it possible for a buyer to acquire the controlling stake in Canfin Homes. Let’s see if Canara Bank has plans to sell their stake. The long-term story of this company would get clear before March 2019, the deadline to raise additional capital to meet Basel Norms by Canara Bank.

I have been holding it for a while(3.5 years) and I am overweight on it. This Chattisgarh investment disclosure of late are bit of nerve wracking. Looks they held significantly high stake (20%??) without disclosing it until now and cant predict what they are upto now since they are disclosing now all of a sudden. The other thing that bothers me a little bit is, this is a PSU, the hard work of the management wont be as incentiwised as in private so at some point of time they might just think why work so hard? (theye have done a phenomenal job in last 4-5 years) I am therefore a bit anxious how will things unfold in near future.

Having said that if magagement predicts it can grow @ 35% for next 3-4 years , its not overvalued. There is sectoral tailwind because of the govt focus on housing and subsidised intrest. Mind you, home loan penetration is still significantly low compared to the developed economies.