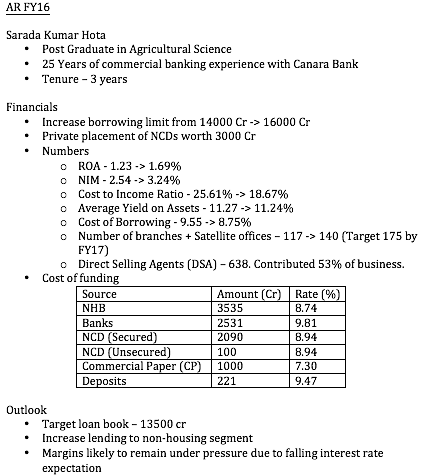

Notes from AR FY16

Disc - I hold and continue to average up on declines

Notes from AR FY16

Disc - I hold and continue to average up on declines

CD EquityResearch raised target to 1488

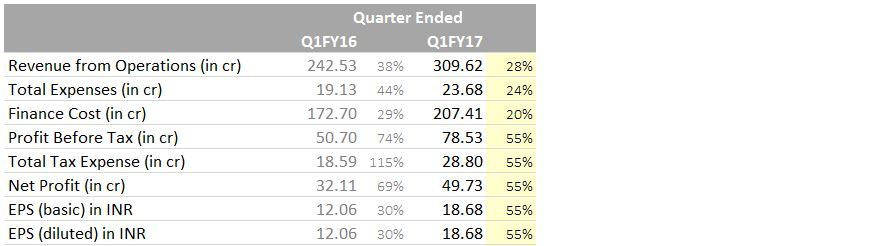

Good going continues for Can Fin in Q1FY17.

In Q1, the loan book has increased by 540 Crores whereas the disbursement has been 1052 Crores? Is the difference only due to higher pre-payment / closure of loans OR there is a lag effect between disbursement and loan book numbers?

Can fin has put up their latest Presentation on their website. It’s good to see ROE and ROA improving.

http://www.canfinhomes.com/Investor%20Presentation%20300616.pdf

some observations

No. look good yoy but qoq looks growth is tapering , but closer look at no. will get 10% growth in profit (as provisioning increased from 1.41 to 5.5 cr)

loan book growth of 5% qoq (very achivable) will get eps of 82-85 rs. for year next year eps can be >100.

roe jumps above 20% for first time and will stay there if current nim(spread) are sustained

funding mix (most importatnt factor driving spread &profitability) improves further qoq change in bank funding at 19% vs 27% . ( recent fund raising by REL jio , NCD at 8.32% for 2000 cr from bse platform is to considered cost of NCD may come down more) prev. year ncd cost was 8.94%

canfin looks cheap at 15 X fy17 and 12.5X fy18

disc: hold canfin since last 4 years . have reduced stake to re balance portfolio weight

Kunal Shah

I found that about 1/6 of the portfolio runs off every year. This number has been constant for previous few years. This implies that about 450 crores would have been the runoff and about 60 crores may be higher prepayment. This adds to prepayment of only about 0.5% of loan book.

To add, tax provision is higher by 4.2 crores on account of DTL. This would be discontinued after fy17, resulting in higher profits. If the current profitability is maintained throughout fy17, then Canfin is trading at about 13 times fy17 p/e (ignoring DTL provisioning).

Hi Pranav

What does run-off mean?

Sorry for not explaining properly. If the portfolio is 1000 rs at the end of fy15 and Canfin does not disburse any loans in fy 2016 then at the end of fy16 the portfolio would be 5/6 * 1000 rs. 1/6 of their loan book gets repaid during a year.

I calculated it using: Runoff = (portfolio at the beginning of the year + disbursement during year - portfolio at the end of year)/portfolio at the beginning of year

you can use this to check if portfolio runoff has increased during the previous year or previous quarter when compared to earlier periods.

pranav two points

run off is part & parcel of business. and what would u like compounding receivables like infra/micro finance or return of capital.. and net advances (loan book) no is after run off . so it is not of much importance according to me till book grows 20% yoy. there are companies like muthoot finance whose entire book is short term finance ( a typical gold loan tenure is 4 to 6 month). disc: i bought muthoot when it was 170 some 5 months ago. and hold it

tax provisions (DTL) are of two types one is on special reserve which was already there (pre fy15) which was to be provided from balance sheet (int three tranches). second is on current amount going to special reserve so what we see in P&L will be there forever (and will grow with profit growth) . but this is just accounting entry i see no HFC withdrawing amount from reserve . so actually u have liability which is (small) float. and can be added to profit also for calculation of actual profit.

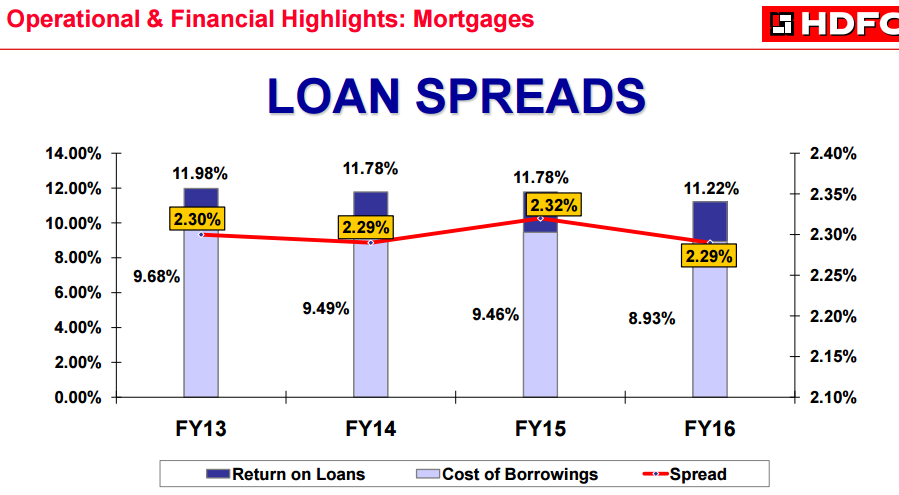

Fellow boarders, In the FY16 investor presentation of HDFC, it shows their yield is 11.22%, cost of funds is 8.93% and hence the spread is 2.29%. I just wonder how HDFC could manage a yield of 11.22% when they offer loans at a very competitive rate (on par with banks at around 9.5% now) and especially when they don’t lend (much) to non - salaried class (at high rates) like its subsidiary Gruh?

Its good see new management started Conference calls after Q1 2017. It’s on ResearchBytes. https://www.researchbytes.com/webcast.aspx?WID=97730

Hi Kunal,

I agree with you on the first point. My point was that even if the prepayments / foreclosures have increased, they are still small. Infact, I heard Mr. Hota saying that approvals increased by 36% this quarter over previous year. That’s encouraging. A 25% to 30% growth in disbursements should result in the loan book of 13500 to 14000 crores at the end of fy 17.

Thanks for letting me know about the two types of DTL. I was not sure about it. I hope that markets would give credit to HFCs for the accounting expense of DTL.

Why did i start looking at run-off? because it gave a good sense of growth in loan book when the company was establishing new branches. It is not easy to extrapolate growth in branches to growth in loan book. But it is easier to project the growth in disbursements for established branches and for new branches separately. It takes about two years for new branches to stabilize. Run-off depends on door to door maturity of the loans and does not change substantially for mortgage loans. An idea of run-off provided good projections of asst book when company was growing fast.

Thanks for the earnings call link…

Additional Notes from FY16 AR:

Couldnt be more pleased with the results. Investor presentation is very informative. I am a little overwhelmed with the way Canfin Homes has transformed in last 3-4 years. Especially, investors meet, transparency and the reports. Now they also started concalls. I kind of think, they have exceeded expectations on that front. Listened to the entire concall, the new MD sounded very enthusiastic and showed lot of energy. I think starting 20 out of 25 new branches in the beginning of the year was strategic to get the results quicker. Interestingly, Canara Bnaks housing loan portfolio also grew about 30% as per the MD Mr Hota. For a while I thought, why couldnt can fin forward all housing loan applications to Canfin? atleast the under 20 lac. May be its my wishful thining…I am noticing more and more of non salaried loan, I think, they have to increase that to keep the pace. Dont know how risky is that, makes me little nervous. Impressed by the reduction in interest cost and operating cost. One of the investor appreciated this part. MD was humbled. They deserve applause. Hope this turns out to be a great wealth creator.

In Q1 FY17, Gruh has disbursed 940 Crores but the loan book has grown only by 430 Crores resulting in re-payment / run-off etc at 500 odd Crores. Pretty much similar to Can Fin.

pardon me but how did u calculate that repayment number?