At the end of Mar 2016, their loan book was 11115 Crores and the same is 11543 Crores now at the end of June 2016. The difference is 428 Crores, which is the increase in the loan book size as against the disbursement of 940 Crores. The difference of 500 odd crores is the repayment / run off number

got it, but market size is too large and also untapped so v look into bigger picture

Yes, market size is large, but there is also lot of competition. I read somewhere that there around 90+ financial institutions (banks/hfc/nbfc…) that give home loans. Not sure how correct that information is.

But on the positive note, the 7th pay commission hikes / arrears are paid from Aug 1st. So the disbursement figures from next quarter (and more specifically from the third quarter onwards) will be interesting to watch for Canfin Homes.

CONFERENCE CALL - from Capital Markets

Targets loan growth of 27-28% for FY2017

Can Fin Homes conducted conference call on 15 June 2016 to discuss the financial performance for quarter ended June 2016. Sarada Kumar Hota - Managing Director addressed the call:

Highlights:

- Loan book of the company has increased 28% to Rs 11183 crore at end June 2016, driven by 30% growth in disbursements to Rs 1052 crore and sanctions rising 36% to Rs 1191 crore in Q1FY2017.

- The company proposes to improve the loan book size to Rs 13500 crore by end March 2016, implying strong loan growth of 27-28% for FY2017.

- About 79% of the total loan book comes from salaried and professional segment at end June 2016.

- Average ticket size of incremental housing loans stood at Rs 18 lakh, while that of non-housing loans was Rs 9 lakh.

- On an incremental basis, the 87% of the fresh loan sanctions were housing loans and balance 13% were non-housing loans.

- GNPA ratio of the company has continued to remain lower at 0.24% at end June 2016, compared with 0.26% at end June 2015. NNPA ratio was negligible at 0.04% at end June 2016 compared with 0.08% at end June 2015. However, the company has always maintained financial year end NNPA ratio at nil level.

- Provision coverage ratio (PCR) of the company has jumped to 84% at end June 2016 from 67% at end June 2015.

- The company has improved NIMs to 3.39% in Q1FY2017 from 3.24% in the preceding last quarter and 3.04% in the corresponding quarter last year. The cost of borrowing for the company has declined sharply from 9.21% at end June 2015 to 8.60% at end June 2016.

- The share of bank borrowings has declined to 19% at end June 2016 from 27% at end June 2015. On the other hand, the share of market borrowing has jumped to 44% at end June 2016 from 28% at end June 2015.

- The capital adequacy ratio of the company was strong at 19.53% at end June 2016.

- The distribution network of the company stood at 120 branches and 50 satellite offices spread across 19 states at end June 2016. The company has added 79 branches and 50 satellite offices in the last five years. The company proposes to add 10 branches and 20 satellite offices in FY2017.

- The company contained the cost-to-income ratio at around 17%.

Disc: Invested.

10 Likes

-

major highlight of concall was that they have guided for further improvement in cost/income ratio as most of branch opening (25 out of 30) was done in April 2016 .

-

no effect of seven pay commission on salary cost .(very obvious)

Though the competition is very high, Canfin Homes operates in a very niche segment - they operate in Tier II & Tier III locations. Big banks, HFCs & NBFCs are primarily focused in metros & Urban locations for funding. Considering the recent regulatory changes:

- Funding allowed upto 90% of the property value

- Increase in the limits for PSL classification - upto Rs.28 lacs

- Passing of RERA (Real Estate Regulation Act),

- Housing for all by 2022

- Credit Linked Subsidy scheme (CLSS)

HFCs are in a very sweet spot. Smaller HFCs like Canfin Homes, DHFL, Repco are expected to grow at 20-25% for the 5 years atleast.

nimish canfin has 35-40% loans in bengalore is it tier 2 or 3

Did anyone attend the AGM yesterday? Any takeaways?

Two interesting things for me in the concal were:

- Average age of their borrowers is 41 years (I expected it to be lower. Don’t know the same for other HFCs operating in similar segment).

- Canfin has got a variable pay structure for their employees (Canfin being a PSU I didn’t expect this either. Again don’t know if PSUs have started having variable pay structure based on performance)

Discl - Invested

Is Canfin really a PSU? The management tried to clarify that I guess in the call. Their promoter is a PSU but that doesn’t mean Canfin is a PSU I guess.

1 Like

Government approves additional investment of Rs 16,641 crore for building affordable homes

Read more at:

http://economictimes.indiatimes.com/articleshow/53396938.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

1 Like

There was a block deal of around 1.25 Lakh shares of Canfin Homes in NSE on Aug 2nd. How do we find who bought and who sold as part of this transaction. When I check the block deal section in NSE, there is no data in it.

1 Like

Canfin has been a great story. We (@Naman) were discussing about the company with some senior investors and when we highlighted about the way the cost of the borrowing has fallen and NIMs have expanded, we were pointed to explore more about it. They were concerned to hear that the company has been going for short term borrowing instruments to expand the NIMs and may be this could result in asset liability mis-match. So it would be great if we all can research on this aspect more:

- Compare the sources and cost of funding today vs 3 years back

- And understand the risks and implications.

Views Invited

Regards,

Ayush

Disc: Invested

11 Likes

yes canfin has been great story .

Phenomenal rise is due to factor double dip that we had profit growth & re rating (we can discuss re-rating part separately and it is widely acknowledged part).

lets look at profit rise (43 to 157 cr) is derivative of (1) Business growth (loan book grew from 2000cr. to 11000 cr (2) Low Credit cost (nil NPA) (3) NIM improvement (again derivative of (a) capital infusion (b) cost of funding going down due to NCD/CP )

now factor 3(b) NCD/ CP borrowing is part of story, and it looks like will continue for some time it will add profitability for some time after that profit rise will be same as business growth (which is 20% , not bad )

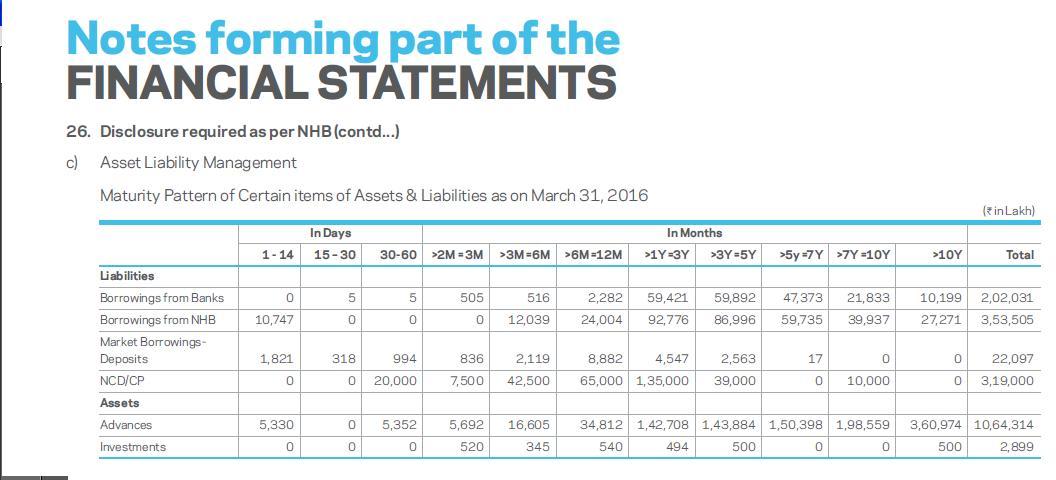

i am posting asset / liability maturity profile from annual report 2016

as can be seen from this screen shot >10 year & >7 year assets(loans) are 3600 cr.& 1985 cr. corresponding liability is 370 cr. and 597 cr. (theoretically point raised by senior investor makes point but their repayment (run -off) is 500 cr. per quarter so this assets may not be there till 2023 or 2026) ![]()

my take on this is , it is important (but not knowable for me). it is hard to predict interest rate for 7-10 years ( imagine likely scenario in 2020-21 interest rate being 200 basis point lower, now we have huge advantage of not tied to long term funding ) . we are having story which played out well in past and can(may continue business growth at rate of 20% for 3-5 years . with some tailwinds from NCD/CP fund contributing profitability for next 2 years and valuation are not that demanding (82-85 Rs. EPS for fy17, PE of 17.5 for current year and 14 times fy18 )

disc: hold canfin as 2nd largest position (had trimmed down position to re balance portfolio weight & bought muthoot finance and aditya birla nuvo 3-4 months back)

5 Likes

I do not have understanding of CanFin business per se but a thought on the larger HFC market.

- I live in Gurgaon and every day witness the urban chaos around. Those living in Bangalore or Mumbai or for that matter anywhere else in India, wouldn’t be much better, I guess.

- Pretty much every individual (who is a potential customer) I know, has at least 2 or more properties already.

- The cost of transaction (TDS, circle rates etc.) for property have gone up across India over last 3 -4 years

- Historically builders left a lot on table when somebody bought a house - intentionally or otherwise. The society I live in is a classical example where carpet area to super built-up ratio is awesome for apartments that came up in phase I and terrible for those that came up in phase III . Today, upside for a buyer (if bought for investment purpose) is quite limited

- Slowly but surely, the frenzy of property is cooling off and I may be wrong, but I think we are in for a very long bear market .

On positive side, we are still a young country where millions of young people are entering workforce who’d buy houses in large and small cities. The question would be, would this demand meet / exceed the investment driven demand.

Canfin generally does not finance the apartments from reputed builders (Sobha, Prestige, Brigade etc.). That is the target market of SBI and HDFC. This end of the market is slow everywhere in India currently.

Canfin generally finances builder floor apartments(G+4) which cost around 30-50 Lakhs for a 2 BHK in cities like Bangalore. There is no dearth of buyers for such apartments. Everyone wants to own a house and people are not able to buy from reputed builders because of the prices. The segment that Canfin serves is buoyant even now and unlikely to see a demand drop in near future. Bangalore, which is the primary market for canfin is 80-90% end user driven even at the high end and almost 100% end user driven at the low end. Investor sentiment hardly matters for them.

6 Likes

Ayush raised a valid point. I had thought that someday I would explore it further. But taking advantage of the snapshot posted by Kunal, it looks like 52% of assets and 15% of liabilities have a door to door duration of >7 years. Canfin has created a serious ALM mismatch to take advantage of declining interest rate scenario and generate higher profits. This strategy can backfire in rising interest rate scenarios. But, that should be some time away. Also, my guess is that the interest rate on about 90% of home loans would be linked to a benchmark like base rate. So, these loans would be repriced too, although periodically. This repricing may not be to the same extent as the repricing in CP markets given the inefficiencies in transmission. Using my elementary understanding of ALM mismatch, I am not sure if it a very big issue for Canfin. In case we are worried about some issue with Commercial Paper market and Canfin not being able to raise funds to repay the CP issuances, then the parentage of Canara Bank should come handy. CanFin should get loans from the Bank at reasonable rates. Profitability would decline a bit, but Canfin would not face cash-crunch like corporates did in the USA after Lehman crisis. In short, Canara Bank can insure Canfin against the tail risk of ALM mismatch.

In fact, now I feel that Gruh should also follow a strategy of issuing more CPs. But, it is possible that HDFC Bank wants Gruh to be completely independent and would not like to bear the implicit guarantee of providing funds in case of a crisis caused by ALM mismatch.

4 Likes

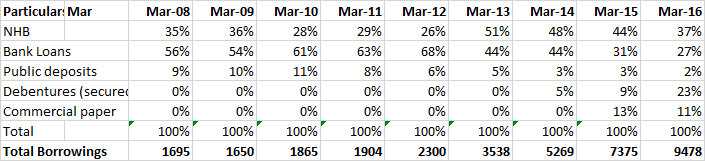

Can Fin has in the last 3 years started raising money through CP and debentures - both secured and unsecured…going from 0% in FY13 to 23% in FY16…and also commercial paper that has increased from 0% to 11% in last 2 years…Bank borrowings have come down significantly, which has a higher interest cost (almost 2000 crore borrowing is from Canara Bank - 75% of total bank borrowings).

Though I need a much better understanding of the ALM, as per AR 2016 a large part of liabilities are short term and assets are of long term…76% of liabilities are of less than 5 years maturity whereas 67% of assets are more than 5 years maturity…If we look at the 12 month maturity, 692 crore assets are being matured, and 2000 crore of liabilities…

However, in the short term this should be taken care of by prepayments, and market borrowing in a declining interest rate scenario we are in.

This needs to be monitored closely as per the Annual Report, CanFin is going to further increase the CP and debentures “Company proposes to increase the share of CPs in borrowing mix during the year to reduce cost of funds further”

& “Your Company is having the plans to raise Non-Convertible Debentures up to a maximum 2500 crore”

I am speaking to a couple of people who understand ALM later this week, and will post in detail.

Disclosure : Invested

8 Likes

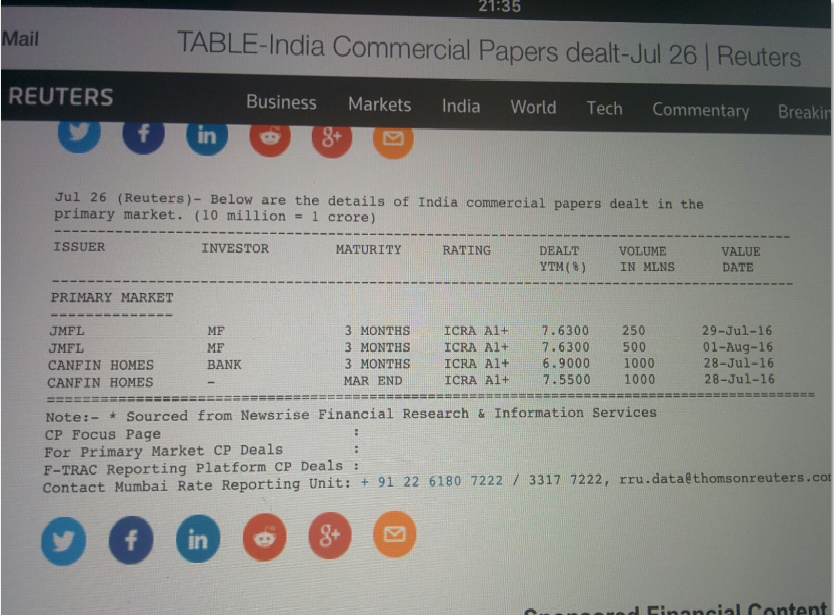

I noticed the asset liability mismatch issue in July end.

I stumbled upon it (trying to check the funding composition in the AR out of curiosity) after seeing the below CP issuances by Can Fin on 26th July as they were issued at attractive rates.

I noticed then, that the difference between asset & liability maturity amounts from the period >3M-6M till >1Y-3Y comes around Rs. 2500 Crs. (outflow exceeding inflows) which kind of tallied with the proposed NCD issuance of Rs. 2500 Crs. (inflows) and hence in layman terms came to a conclusion that in a stable to soft interest rate scenario (which is expected in the near to medium term), along with other funding lines apart from these NCDs, the asset liability mismatch may not be an issue for next 3 yrs.

Below link gives some info on the funding options available along with their credit ratings and also states that "CFHL’s liquidity profile was adequate supported by access to long-tenure borrowings (average maturity of 7-8 years) to match the duration of its assets (average maturity of around 10 years) as well as access to unutilised bank lines to plug the mismatches."

It would however be good to understand it in detail from somebody who is an expert on ALM, etc.,.

Cheers.

Discl -Invested

7 Likes

Thank you guys for discovering it. It could be beneficial in the very short term and risky along the way.

Difficult to predict the future rates. Now that we have figured out ALM mismatch, we could throw this question to management. They have been very transparent and forthcoming in clarifying the doubts. Who know they could be doing it consciously with some mitigation plan.

Thanks-Mahesh