@aveekmitra 2015 AR talks about their performance despite weak global economy. During AGM, did they talk about their vulnerability from weakening global environment considering they are market leader in few products.

hi, have been following this company for few months and have some questions on P&L . I wrote to company but received no answers. Wondering if any of the fellow investors has answers.

The other expenses of September 2015 quarter have risen to 37% of sales whereas in the previous quarter they were 32% of sales. Is it due to some one time expense incurred by the company, which could have led to this increase? what is the amount and nature of such expense.

In the september 2015 quarter (2QFY16), the sales seem to have declined QoQ from Euros 14 mn to Euros 12mn. Is it due to the seasonality of sales? If not, what is the reason of such a decline.

In March 2015 quarter (4QFY15), the revenues posted a steep growth (India as well as international). Is this due seasonal buying pattern of users? were there any large orders that may not repeat?

As per annual report of FY15 page 124 Consolidated accounts CFSL incurred cost of Rs413.28 lakhs as exchange fluctuations and Rs834.35 lakhs as bad debt written off. break up of these costs for every quarter is not available. I assume it will impact “other expenses” in a big way. What is the amount of exchange fluctuations and bad debt written off in 1Q FY16 and 2Q FY16?

Thanks in advance

@sumi00 It seems CFS has achieved growth in sales in recessionary environment. Please read annual report of last 4 - 5 years. The company has done lot of incremental capex in last couple of years

Hi @aveekmitra, As I understand from the annual reports going forward Company is eyeing the incremental revenue from the HQ, Vanillin and Ethyl Vanillin business post commercialization of the proposed Dahej Plant. But the game changer will be Vanillin & Ethyl Vanillin. The global demand for Vanillin (Natural and Synthetic) stands at ~ 20,000 MTPA. But the problem I see is , Even though there are only few players, demand is already filled up with the existing players.

Below is the production capacities of the largest players (all fig. in MTPA)

- Solvay (erstwhile Rhodia) - 12,600

http://www.icis.com/resources/news/2003/07/11/502966/rhodia-s-f-f-operations-optimizes-manufacturing/

(its a dated article before Solvay took over Rhodia, post acquisition Solvay has increased the capacity by 40% in 2014) - Jiaxing - 6,000

http://www.chinafooding.com/297/Vanillin_applications_at_home_and_abroad - Wanglong - 5,000

http://www.wanglong.com/ - Liaoning Shixing - 3,000 (Vanillin), 1000 (ethyl Vanillin)

http://www.lnsx.com.cn/index_en.html - Anhui Bayi Chemical Ind Co - 3,000

http://www.bayichem.com/gsjj-en.html

I hope Company had done their research before entering the market or am I wrong with the current market size.

My apprehensions are

- Company is entering into a sector with such a high capacity (6000 MTPA), will the company be in a position to utilize the entire facility and sustain the margins (from competition).

- What is the growth expected in Vanillin sector (Couldn’t find anywhere)

Will do further research and post the relevant things…

Disclosure: No position, Under watch list

3 Likes

Humble question - Is Camphor and Allied Products in the same space as SHK and CFS ? It appears to command less premium than SHK. Whu?

The global vanillin market is expected to register a double-digit CAGR for the forecast period. Depending on geographic regions, global vanillin market is segmented into seven key regions: North America, South America, Eastern Europe, Western Europe, Asia Pacific, Japan, and Middle East & Africa. As of 2015, emerging region Asia Pacific dominated the global vanillin market in terms of market revenue. Asia Pacific & Japan are projected to expand at a substantial growth and will contribute to the global vanillin market value exhibiting a robust CAGR during the forecast period, 2015?2025

1 Like

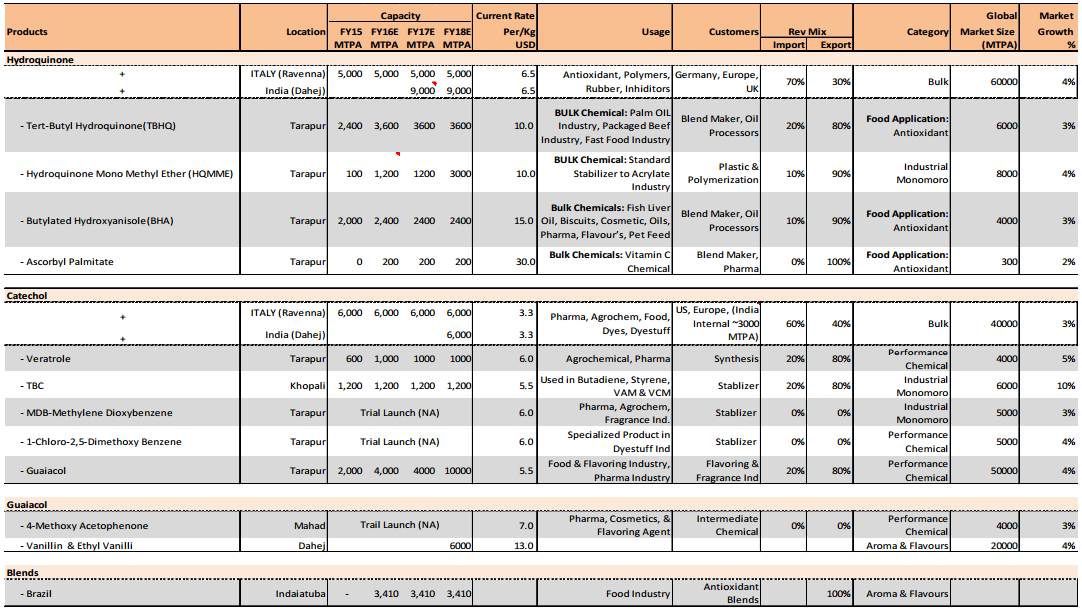

The table on page 8 of this report is quite informative in terms of capacity, global demand and pricing of CFSL’s products.

http://www.indianivesh.in/Downloads/635798102875790000_NiveshDaily_-_5_October_2015.pdf

Vanilin market is stated to grow at 4% according to the table. Source: Indianivesh.

1 Like

Thanks Akshay, its product portfolio are on the track.

Lately there is downward movement in the stock price…Any play from the promoters…?

Disc - Not invested

Latest shareholding pattern shows exit of Ashish Kacholia from camlin fine.Source BSE 21.1.2016

Pl reply if anybody knows who bought that stake.[around 1189000 shares]

He has massive 5.73% stake maintained in Pokarna which has been beaten out of shape. How would you explain that?

Camlin Fine Sciences Limited has informed the Exchange that the Company’s subsidiary CFS ANTIOXIDANTES DE MEXICO S.A. DE C.V., Mexico (CFS Mexico) has entered into a share Purchase Agreements to acquire 65% stake in a entity in Mexico along with its proposed group companies, which shall be subject to certain conditions being fulfilled prior to the said acquisition

Ashish Kacholia had 1.24% in camlin fine - all of these were acquired in Sept Q. In Dec Q, one does not see his name on BSE site, however this does not mean that he has moved out completely as he may have moved a portion of his holding to his wife’s name and if individually one does not hold more than 1%, the name is not declared. There is also a possibility that he has sold off a small % of his holding. In general, Ashish is known to buy after a lot of research and holds his stocks for 2X - 3X returns…Camlin Fine is a good company with good growth prospects over the next 2 - 3 years, one should not worry too much with this stock…

Disc : Holding since a long time…

Q3 FY16 Results:

http://nseindia.com/corporate/CAMLINFINE_results_12022016180823.zip

1 Like

Vivek,

I personally admire your contribution on several threads, I feel simply commenting on the direction of price movement is not adding any “value” to this forum. What we expect is to put out an analysis on which segments have underperformed and your understanding on why that happened, if its one off or if it is going to be a trend.

Thanks you for your understanding.

Regards

Disc: not invested

One reason for bad result being cited is that EUR movement against INR during the last year hitting margins. Their European subsidiary supplies raw material to the Indian plant. This is unlikely to change in very short term till new supply gets repriced.

Explanation for the higher tax rate for 9M FY16: 11Cr vs 1.2Cr

The explanations are good for analysts but common investors would look at earnings and EPS in this kind of market like what happened after Q2.

Disc: Invested

As i was reading through @Mahesh excellent research posts on Adi Finechem, i wanted to have a look at the other side - synthetic antioxidants market. I have been pretty impressed by Camlin’s journey in the past 10 years and the next phase looks very promising and FY18 could possibly be the next inflection point.

While there is an increasing demand for organic food, synthetic antioxidants continue to have the dominant market share at 60-40 and looks to sustain it in the near term atleast due to the cost advantages primarily. Besides, synthetic antioxidants have applications in various other industries which CFS has targeted through Bio-fuels, Pharmaceuticals, etc.

Being a pharma guy, first thing i did was check the downstream API’s that are catered by the Performance chemicals such as Guaiacol, Veratrole, etc.

Source: http://www.camlinfs.com/pharmacueticals.php

The reason i have highlighted the Indian co.s is that i could not find extensive export quantities in zauba, which makes me think most of the uptake is taken care of by these cos.

And this also explains why they posted impressive sales growth of 40% last yr.

On Veratrole from AR FY15 -

Supplies to major customers in India and international market have commenced and the product has been well accepted. The aim is to capture 70% market share in 2015-16.

@aveekmitra Donald had mentioned that u had done extensive work on Granules. Would like to know if you had come across CFS as among the key suppliers for Guaifenesin?

Rest of the Performance chemicals such as TBC and HQMME have equally promising oppurtunity size, while not being related to FMCG/Pharma end-use.

But coming back to the Pharma angle, it bodes well that they cater to both bulk-drug API/Intermediates as well as relatively more complex drugs like Donepezil.

On Management

Came across the below ET Profile on the Founder and MD, Mr. Ashish Dandekar.

http://www.camlinfs.com/press/press_eco_times_26_06_2015.pdf

(BTW for a small cap it has got a very good website with nice disclosures on key information)

Below 2 quotes stand out and exemplifies the management’s obsession with operational efficiency while at the same time doing prudent capital allocation.

“My strategy focuses on cost leadership. Global leadership creates a comfort zone which leads to the dilution of focus on cost leadership”

Camlin Fine Science’s underlying business philosophy could offer a way out: size does not matter as long as you are in control of your costs.

Also while ironical that he dropped out of Science degree and eventually ended up running a Chemicals company, it stands testament to his abilty to wrest the market share from Eastman for TBHQ and BHA as mentioned in the above article.

-

Value Migration play from dominant raw-material player to a complete value-chain integrated finished products player.

-

Decent R&D Spend of above 0.5% of sales in last 5 yrs. FY15 was 2.77% due to one-off expenses to setup new R&D lab in Tarapur plus addition of new equipment. (Vinati has spent 50 and 80 lacs last 2yrs which is much less than 2.7 and 2.5 cr. done by CFS)

-

Mgmt impetus on reporting Cash Accruals Metric (Operating Cash Flow) is a big thumbs up.

http://www.camlinfs.com/docs/Camlin%20Fine%20Sciences_Final%20Investor%20Presentation.pdf -

When i went through the interviews back in 2011 at the time of Borregaard acquistion, management had under-committed to 160 cr. and 290 cr. sales in FY11 and FY12 resp. while they had actually over delivered with 171 cr. and 335 cr. in reality. I had much prefer this than the opposite.

http://www.moneycontrol.com/news/business/borregaard-deal-to-fetch-camlin-chem-rs-90cr-revenue12_533218.html

Mgmt interview with Frost and Sullivan back in 2006.

On US ventures -

Camlin has just set up a Linkedin Page to announce the below news.

You can also visit the link to view the official press release.

https://www.linkedin.com/company/solentus-north-america-ltd

The new Iowa-based facility will house company sales and marketing staff and research laboratories, noted the company. It also will provide stability trials for customers.

The move marks a step in an ongoing program to know customers and end product users better, said Jennifer Igou, vice president of sales for the North America division at Camlin.

“We’re the backseat player,” she told FeedNavigator. “They’ve been using our products for a long time in animal feed and pet food but we’ve been the ingredient supplier so nobody knows our name.”

“We’ve been selling [products] to blenders.

“We hope that our customers see the value of that with the vertical integration [because] it gives more assurance of quality and supply," said Igou.

Future expansion

Additionally, the use of antioxidants to extend feed stability is growing in North America, both for traditional and natural antioxidants, she continued. Calmin produces dry or liquid antioxidants treatments that can be mixed into feed for poultry, cattle and pigs. Additionally their products can be used to treat aquaculture feeds.

However, the Iowa-based facility is not the only US project for the company, said Igou. And the current feed additive antioxidants are not the only products planned for US distribution.

On Mexico acquisition

http://www.indianivesh.in/Downloads/635905265281406250_NiveshDaily_-_4_February_2016.pdf

-

The combine companies have large products portfolio, proper sales mix with relevant processes and equipment in operation along with adequate installed capacity for operations to support future growth. It markets its products through its own sales force directed from its headquarters and its branches and a network of distributors in North, Central and South America.

-

The company is having presence in Bactericide, Antioxidants, Human Consumption, Disinfectant, Linea inhibitors, and Several. Under these segments the combined companies have +55 products catering to various industries.

-

Dresen & group companies have total revenue of Rs.909 mn ($14.8 mn) with nearly 15.5% and 11.2% of EBITDA and PAT margin, respectively in CY14. CFSL has acquired 65% stake in Dresen and has option to acquire additional 35% over next two years. The transaction will get completed by the end of Q1FY17E. The total acquisition cost is $7.8 mn (Rs 514 mn) for 65% stake in Dresen & group companies.

-

Based on the transaction value, the total company is valued at 0.81x of EV/Sales. The target company does not have any debt on its balance sheet.

Personally, there is a deja vu feeling on how similar it is to Borregaard.

Acquired on dirt cheap valuation.

Gaining additional technical expertise on downstream blending.

Gaining an established sales-force and distribution network.

Investment Rationale

Company is truly progressing at a rapid pace in its plans to ensure all the necessary contracts or client relationships are in place when the Dahej capacities come online in FY18.

To that end, the establishment of Food application and Blending laboratories in India, Brazil and US now looks a great decision in hindsight.

Interestingly along with the existing Xtendra customized blending of synthetic antioxidants, CFS has launched this year “NaSure” customized blend of natural antioxidants.

http://www.camlinfs.com/food.php

Our Nasure plant-based antioxidant products offer you a natural alternative in shelf life extensions. Rosemary extract, Green Tea and Mixed Tocopherols are just some of the natural ingredients we use to encourage high antioxidant activity and to ensure that your food stays fresher for longer.

Another important point is that, they have labeled their Vanillin and Ethyl vanillin products with a brand name - Vanesse and Evanil. This aligns with their off-the-shelf ready-made solution strategy and gives scope for creating a brand/marketing strategy around it in the future.

Ultimately, i perceive that management has built up assets with a strategic architecture to provide disproportionate returns in the future.

IMHO, it can be a type A stock while not necessarily a A+.

Risks:

Negative interest rates across Europe is worrisome as it implies a negative growth rate for the economy. Need to figure the sales breakup by Geography to see how much impact this may have.

On the other hand, Latin American economies have their own set of issues and currency risks.

At the current price, i feel downside is limited and upside remains potentially “yuge”. ![]()

PS: Sorry Mahesh, you have lost me to the Dark Side ![]() (Depending on which side u are)

(Depending on which side u are)

May the force be with u.

And thanks to Aveek again for providing another excellent idea.

Also, Excellent report by Phillips Capital provided a nudge in the positive direction.

Disc: Had bought a small initiating position on market close to complete the above analysis. Will add incrementally over the next few weeks as capital becomes available.

15 Likes

Hey @crazymama , thanks very much for collating everything and putting in a coherent manner. Interestingly, their quarterly accounting numbers are all over the place while cash flows remain solid. Any management would be tempted to smooth out and look smart but they have done the right thing by disclosing cash flows and leaving PAT volatile. . I have not heard if the construction of Dahej plant has started. They were waiting for environment clearance.

Risks: Demand growth, Chinese suppliers, Currency movements

Disc: Holding since last 6 months and keep adding on corrections

1 Like

Another acquisition…