Management’s reply on this… They are not worried more about negative comments or ratings as people who have liked the stay and positive don’t go and rate hotels in most of the cases. But they have promised to take action to make sure there is response from management on those negative comments and further improvement.

This was one of the questions asked and suggested

Reason was not given due to lot of answers together and shortage of time but they were positive on hosting concall

This was partially due to lot of cancellations in room chartering business last quarter (in northern region) and there expenses on 4 new hotels have started without hotels being operational…so… partially due to that…you can expect similar margins in coming quarters unless those 4 hotels are operational

They don’t see Oyo as competition and they have started work on online booking portal too.

Why there was a huge cancellation that too in northern India, any specific reason?

Secondly they dont see oyo as competition but camon we all know the real competition is from Oyo and as far as their online portal is concerned ,I had a detailed chat last year with Anil sir, he told it will be rolled out soon, its been 1 year and still they are saying the same, I am not telling that management is misleading, m just telling that lets understand the reason for the delay and all the new steps they are taking to counter competition.

Regards,

Rushikesh

How many years OYO will get free VC financing?

Not so sure about the reason…I guess some disruption in North India

Any more questions in AGM and on the stock price reaction ? Are there plans by promoters to buy shares of the company?

But I see many positive views on various resorts on trip advisors and those are really helpful to decide which one to book.

Trip advisors, Glassdoor and similar websites are TRUE form of democracy and I respect that and that separate the BAD from GOOD… This answer from the management is not inspiring as this is “lame” excuse…

2 Likes

Hi Ashish

I respect your views but i agree with management on a part that the customers who are actually happy, don’t go and post review online. But the one’s who have had bad experience due to some reason, there are more chances of them posting review online (you know to take revenge sort of that i want to spoil the name)

This is something which as a customer, even i have done for some hotels. I never posted for places which i liked.

No doubt, times are changing. And these days, apps have made it compulsory for people to rate (atleast they show lot of pop ups to rate the place if i have booked online)

So i think, we should see customer satisfaction from ratings going forward.

Management has promised that they are going to keep an eye and reply on terrific or bad reviews for sure.

Moreover they will be hiring specialised people for this even if it becomes costly for them. So yes be ready to see more manpower costs going forward to improve Byke as a brand

Disclosure: As i hold shares, views may be biased.

A simple apology and assurance that such things will not repeat will suffice. People are reading reviews to buy mobiles, same thing happens with hotels. Many will read the negative feedback and will not stay at the hotel. People usually visit these places with families, the safety and comfort of the families will be the top priority, so if the management does not take these negative reviews seriously, they will lose some customers.

Are you buying at these levels or just holding to previous purchases?

1 Like

Are there any other important questions raised ? Are there any plans by the promoter to buy more shares from the market ?

I attended the AGM, they ran out of time before my turn came to ask the questions but most of my questions were asked by others and I could catch up with the CFO Mr Bajaj and the MD Anil Patodia afterwards.

Paresh Sarjani, were you there? We should have met!

Here is what I recollect:

Status of Byke Delotel: Because of the Kamala Mills fire, OC(Occupancy Certificate) got stuck. There were new fire safety requirements and the company has got the NOC from the fire department and has applied for the OC which would be given in next 2-3 months time.

In the last year AGM the company had said they will surely achieve 25 hotels by 2020 but now they say they will double the number of property in 3 years. Currently they have 13 properties(11 leased and 2 owned). This year they have already leased 4 properties, signed MOUs for 2(Delhi and Kochi) and they have 3-4 properties in advanced stages of negotiation. They have exited couple of smaller properties. They said they are going to focus on bigger properties.

Byke acquired Brightland-Matheran property in an auction. The company paid about 8.5 crores for this 63 rooms, 7 acres property which is worth about 40 crores(according to Anil). Hence they took the loan.

They didnt admit it but looks like their room chartering business is not doing well. The CFO said the margin in room chartering is 30% usually. Last quarter(dont know whether he meant Q4FY18 or Q1FY19) was not good because of a lot of inventory(room chartering) didnt get sold, especially in north India. They did say that they would focus more on new leased properties to compensate or the decline in the room chartering business. They said they are working on an online portal for the room chartering business and it would be ready in 2-3 quarters.

I asked Anil Patodia about the reduction in number of agents in the network and he said this number goes up and down periodically and it is not a concern at the moment. The agents get a margin of about 10-11%. He said even the online travel agents like Makemytrip and Goibibo get the same margin. They are trying to make the company’s website more polished to get the customers to book with them directly.

Many people asked Anil about OYO and he kept repeating that the competition from OYO and the likes doesn’t matter because the market is so big.

Somebody asked about the break-even occupancy rate for leased hotels and he said typically 50% occupancy covers all costs.

Few people asked Anil about increasing the promoter holding, he said he would if he had money, and he said he increased his stake slightly sometime back. He didn’t answer anything on the share buyback question. (My personal opinion: I don’t like a company to buyback the shares to shore up the share price unless it holds tonnes of cash like Infosys.)

They are trying to establish another revenue stream: fee income from hotel management. He said they have teams in active talks with various hotels in this regard.

Various speakers asked about the bad reviews in TripAdvisor: Anil said that, typically people post their bad experiences, not the good ones. But he assured that going forward he will ask all hotel managers to reply to every bad review.

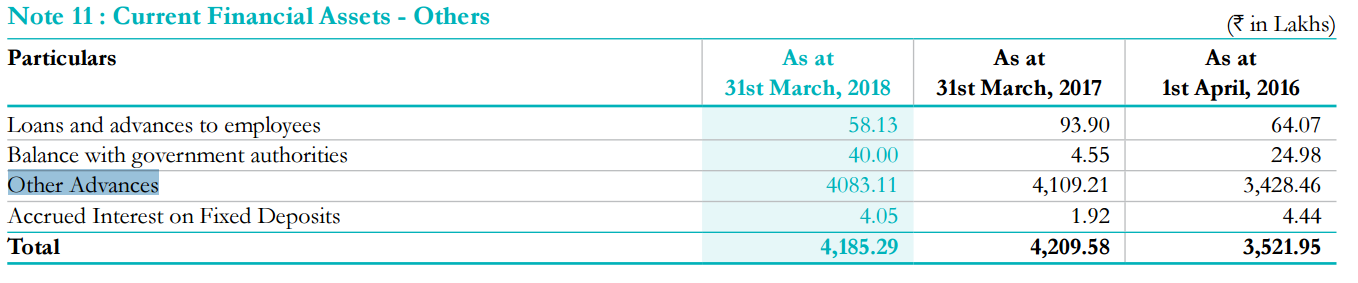

I asked the CFO about the loans and advances:

The one in currents assets (Note-11), about 41 crores, represents the advances given for room chartering

The one in in non-current assets(Note 6), which has increased to 8.45 crores(from 0.8 crores in last fiscal) is the advance given to one property(I think he said Borivili property but not sure).

The company agreed to hold quarterly conference calls going forward. They said they stopped the calls because they didn’t have bandwidth. This didn’t sound convincing.

Disclaimer: The above notes are based on my scribbled notes and my biased memory. it is possible that the management said something and I wrote something completely different, please forgive me for that.

Disclosure: I am invested in this, from a much higher level (of course!).

11 Likes

Did the management touch upon the promoters’ pledging shares? Though it is in small proportion, what is its significance? Any idea?

Somebody asked this question but I don’t think they replied to it. I just saw on the BSE website that there is a new pledge(shares held by Choice Capital Advisors) created on 24th september giving the same reason: Choice Finserve’s working capital.

Since the stock price has tumbled, I think the bank(or whoever has given the loan to Choice Finserve against these Byke shares) must have asked for additional collateral.

The shares held by Chioce is pledged for their own need, should be ok, no?

As long as the bank doesn’t invoke the pledge and does a fire sale, it shouldn’t matter. And if the bank sales in a distress it will affect the stock price in the short/medium turn but shouldn’t matter to a long term investor.

A fellow forum member asked me privately how I felt about the company in the AGM, did I find them genuine and my opinion about the fundamentals of the company and the long term view.

I am posting this here because I have the exact same questions in my mind and I want others to chime in. (When a stock is at a higher level we usually discount a quarter or two of underperformance but when the stock tumbles with the broader market then we start questioning the fundamentals!)

I have started investing in Byke since Feb-2017 and my average cost is about 171. Since I do concentrated investing, Byke forms about 12% of my portfolio.(Disclaimer: I may add more or I may sell some or I may completely exit this position and I have no obligation to mention my intention/activity here.)

Strange thing is: when I reached the AGM venue about 20 minutes earlier, the AGM for Choice International was going on, and speaker after speaker were shouting high praises for that company. Sunil Patodia(looks like Anil’s brother) urged(from the podium) everybody not to sell their shares as Choice may become a 10 or 100 or 1000 or a 1 lakh bagger in future. At the end of that AGM, the Choice shareholders gave a big standing ovation to the bosses of their company. This is the same Choice company which owns the entity which is pledging Byke shares for its working capital! The whole thing looked a bit shady.

In Byke AGM also, a lot of people kept praising the management and took up a lot of time, the reason why few of us couldn’t ask our questions. But there were at least 3 persons who asked probing questions and Anil answered most of them from the podium.

Later, when few of us told Anil that we have some questions, he actually sat down and answered all questions. He just said “Don’t ask me numbers, I will make a mistake. For accounting questions go to the CFO.” He was very candid while answering, except once: before the AGM couple of us asked him about Byke Delotel and he got annoyed and said “Everyone is asking about it. We have everything ready and waiting. You don’t have to believe me, why don’t you guys go and see the property yourself, it is nearby only.” He explained the Delotel issue from the podium and in spite of that I saw a lot of people asking him the same question after the AGM

I saw him going around and talking to people for over an hour after the AGM and later during lunch time. By the way, the lunch(all veg) was delicious!

The CFO also answered few questions and was giving out his email/mobile number to all those who asked.

I met few analysts and few investors. Everyone was trying to figure out if this company is a real deal! One investor was sure that their room chartering business is on the way down and hence they are looking for alternate revenue source. We were talking about the sharp decline in stock price and one guy(I think he represents a fund company and Anil seemed to know him personally) mentioned that Wasatch(the foreign fund which is holding a good chunk of Byke) is selling. I should have asked that guy “Why is your company not buying if Byke is good?” but I didn’t.

Here is my personal opinion: this is a company with almost no debt, has pretty good numbers, the management seem to know what they are doing, they look market savvy( not tech savvy though) and they appear to be hungry for growth without taking on debt or diluting equity.

But, is the company/management honest? And does it have good long term potential and does it have the wherewithal to achieve its potential?

If I thought otherwise then I wouldn’t be staying invested in this stock. But I can be wrong as I have been wrong before about many companies.

Why would a big investor sell in a hurry, does Wasatch know something which we don’t?

Sorry for the rambling post, I just didn’t know how to answer the questions/doubts concisely.

(Disclaimer: I may add more or I may sell some or I may completely exit this position and I have no obligation to mention my intention/activity here.)

15 Likes

Great Response Hrusikesh !!! . I also saw similar response from Equity Master as well where they mentioned that the fundamental are intact and no negative views. ( Wont be able to post it here due to subscription issues ). Hope conviction pays

Thanks Hrusikesh. I attended the AGM as well. And here are some additional points.

1. Room Chartering going down. Anil Patodia did not answer this question, may be due to shortage of time. What I gathered during lunch was, that as a combination of GST, competition, unable to sell room inventory due to Shimla issue (don’t know what this was), they think this business will suffer. Hence to make up for this, they are aggressively adding properties. Sunil Patodia also mentioned, during lunch, that they may bring in some sort of an IT solution to have lesser manual touch point.

2. Building ‘The Byke’ brand. Anil Patodia did mention that they want to build a brand as it will help them sustain them in the long run. They apparently do have a good brand name and recall, despite Trip Advisor ratings etc. They apparently have won awards from Make My Trip and Ibibo as well.

3. New Properties. 3-4 properties (including Delotel) have been added but are yet to start generating revenues. Secondly, like retail, new hotels initially have low occupancy (like 30-35%) and take time to reach a 60-65% level. Therefore, once they mature they will add to the bottom line significantly.

4. Debt/ Debt Free. Anil Patodia mentioned that the ST debt that we see was essentially overdraft facility. They used this line of credit to purchase the property in Matheran. But as such they are almost debt-free.

5. Dividends/ Buybacks. A lot of shareholders asked for bigger dividends, buybacks, bonus shares etc.

6. Choice International. A funny/ strange thing was that the Poddar family that runs Choice is a promoter in Byke and the Patodia family is a promoter in Choice. Poddar family has pledged Byke shares and Anil Patodia has pledged Choice shares. (This I saw in the Choice Annual report.)

Following points are my purely personal opinion:

-

I raised the issue of management not responding to Trip Advisor ratings. I even took printouts to show how Royal Orchid and Lemon Tree respond to poor reviews and how there was no response from Byke to similar reviews. Both Anil Patodia and his wife, came to me after the AGM and thanked me for pointing it out. They thought that their team was responding and promised to take corrective action.

-

On Anil Patodia. I found Anil Patodia humble, approachable and open to criticism. One of the factors that weighed on my mind last year was that he himself was buying from the market regularly for the past 3 to 4 years. Of the universe of investment choices that he had, he chose to invest in his own company. Adding more skin to the game.

-

If you see the track record, they have repeatedly gone into new and more profitable areas of business- focus on F&B, MICE, room chartering and now project management. If you compare the 5-yr numbers, you will see that the bottom line has grown much faster than the top line.

-

I don’t think the company has lush funds to buy back or pay bigger dividends. It’s a small, growing company and is going to need capital. The business is generating close to 30-35% ROCE and should therefore reinvest in themselves.

Maybe I am not skeptical enough, but I couldn’t find too many red flags with Byke.

disc: Invested.

10 Likes

I don’t see anything fundamentally different for the stock to take such a beating. This seems to be a good company, with good management, an asset-light business model, having less debt and cautiously expanding. Of course, some hiccups in room chartering. But, may be I am not seeing something what others are seeing / scared of. I had a re-look at the annual report with some more pessimistic feeling that the market could be right ![]()

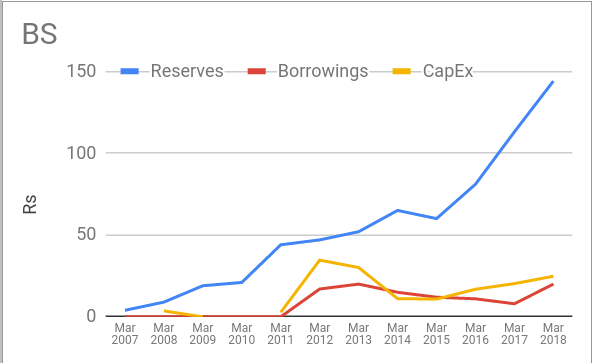

Balance Sheet

I think BYKE has the means to see through any adverse market conditions. They have ample reserves and little debt.

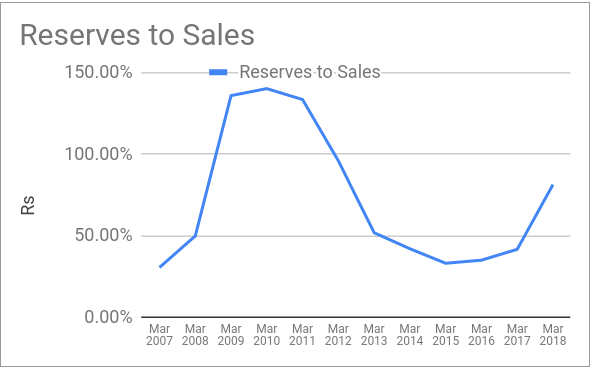

To get a better view of how the reserves stack up against sales, I plotted the graph below.

The last increase in the ratio is because of the drop in sales number due to the IND-AS accounting. Nevertheless, what we can see is that the company always needed to maintain a significant book value at all times.

This prompted me to see why this is the case. A simple look at working capital would show it to be 45Cr.

I tried to balance off some of the components in the working capital:

Trade Receivables: 30Cr against a trade payable of 4.2Cr and borrowing of 19 Cr

Cash: 11Cr and Deposits/FD: 18Cr as against current liabilities of 24 Cr (excluding borrowings)

What I am not able to place is this part: Other Advances: 41Cr

At this point, I am still not able to find out what “Other Advances” would mean. Meanwhile, I also found this in their AR:

Would this mean that they are accumulating the contingent liabilities part as “Other Advances”?

3 Likes

I think this was clarified by Hrushikesh from the CFO

2 Likes