Thanks Vinay. That explains the working capital.

Meanwhile, found this in Twitter space.

Thanks Vinay. That explains the working capital.

Meanwhile, found this in Twitter space.

I think that is an extremely inaccurate statement to make. Why is it then that only in the case of Byke hospitality that negative rewiews are posted and not posted whereas there are tons of hotels where there are barely any negative reviews and tons of positive ones. I have personally seen hotels with no 1 or 2 star reviews at all.

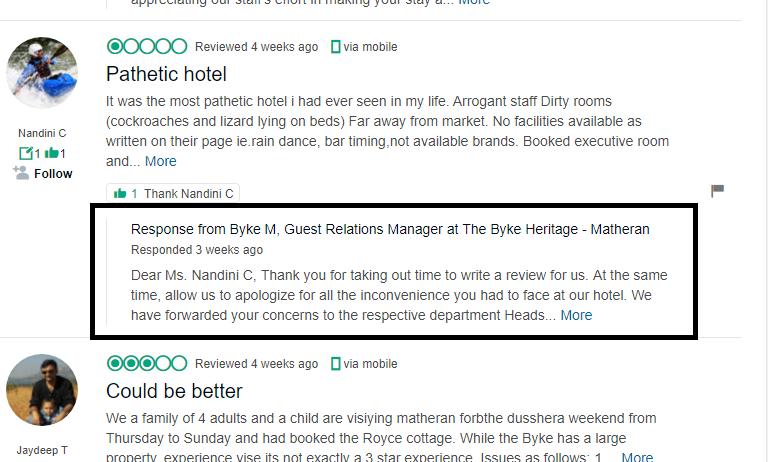

At first glance the numbers of the company look good and worth digging into however, the tripadvisor ratings threw me off. I just cant see how a company in the business of customer service with bad customer service can create long term value.

The cross holding with choice international bothers me. Why pledge each other’s shares? What is the arrangement between the two promoter families?

Also there is a steady decline in the topline for the past several quarters. But that doesn’t explain the sudden drop from 170 to 70!

Anyone has any thoughts…

Byke announces almost flat numbers but lot of hotel acquisitions on lease…and new restaurant opening in Malad

Company changed its accounting method of revenue from gross basis to net basis for room chartering segment from Apr01, 2017. Hence FY18 sales numbers are not comparable to FY17 sales numbers.

Another positive: The management is holding a con-call on Thursday. While that does not change the financial fundamentals, but this is very positive in terms of management integrity and sentiment. Also brings in that management is concerned about the serious wealth erosion and would be willing to address all the investor-pain points and concerns.

Add to that Investor Presentation also brings in much needed information wrt expectations and approach.

The working capital reqt has gone up significantly over the past 3 years. Avg working capital days was 42 at the end of Q2FY16. It is now 124 after Q2FY19. Does anyone know why this has happened. what is changing in their business that requires such an increase in working capital? One of the key diff between Bike and other hotel players was low capital intensity in their business model.

Almost 50% of their current assets is under “Other Advances” as per their AR. Along with steady rise in debtors and inventories this is the reason why their WC has gone up. Are all these 3 related to the room inventory they hold for their chartering business or only the other advances? Can someone pls throw some light on this or if possible raise this in the con call today? If this indeed is all related to their chartering business, it probably is more concerning. I simply calculated the working cap days using their room chartering revenues instead of the total revenues and the increase is much more drastic. Maybe I am doing something incorrectly, but it seems to have gone up from 140 at the end of Q2FY17 to 641 now!

Byke Conference call happened in Hindi. If any of you could summarize the points discussed here it will be great

Yes I was too not able to attend,was eagerly waiting for the same, at last they have done it, it will be really great full if some one can summerise and also give some color how the management was sounding by their tone n all. Thanx in advance.

I attended the Con-call and here’s my summary of the discussions:

1. Management contracts

2. Room Chartering Business

3. Restaurant business

4. Other Points

Overall the management (mainly Mr Anil Patodia) was very upbeat and speaking very positively. I have heard hundreds of conversations, but this is probably the first time that the promoter appeared genuinely nice, greeting every participant in an extremely friendly manner and explaining all the answers in a detailed manner. Sometimes it even looked as if it was a casual conversation with him than an official Con-Call.

Though I too would have preferred some numbers and guidance, I think it is fair that no guidance/made up numbers is given without the actual results of the new business vertical (management contracts and restaurant) till at least a few quarters.

That’s all my notes. If somebody else attended the Call, then please feel free to add any points that I may have missed.

Disclosure: Invested and views may be biased.

Thanks Vinay for the details. I joined the call late. Only thing I would add is: Anil said Nashik Inn is a new property and Byke would be the first one to operate it. The property at Bodh Gaya would need large capex as it is a big property in terms of area(3.5 acres) and it has a large hall for meditation.

Thanx a lot Vinay, well sumerised got the idea overall.Hope their plans workout. It really helps a lot of us in this forum, that ppl like you take the pain to attend and give the summery of the topic. Also I would like to thank @VikasKasturi and @Hrusikesh who are contributing a lot by regularly attending Concalls and agms and keeping us all updated time to time.

Regards,

Rushikesh Kanthamani

I attended the quarterly call, but did not record the audio or take proper notes. Will correct this the next time. So I am going by memory.

I agree. It was fun to talk to him.

Apart from this, slide 17 of the presentation was very useful. 200 more rooms are likely to come on stream in next 6 months.

@Janme, ECL Finance has created pledge on the on shares. This is not exactly a buy transaction.

If the company fails to repay loans, the acquirer would sell the pledged shares causing panic and drop in share price.

This seems to be fresh pledge created by the ECL Finance Ltd (an Edelweiss company) to the best of my knowledge.

Yes I too hold the same view as @Advait_6270, when pledged shares are sold they are not bought by any single entity and are market executed so multiple ppl buy and share price falls drastically down and if we see the oct 5th the stock opened at 86 and closed at 84 which means no drastic change hence it proves the point i guess . Any body with any understanding do comment.

Discussed this with the IR guy, he said this pledging is from choice broking and they pledged it for funding the trading margins

Thanks for the explanation.