Topline growth is 43.8% as excise duty needs to be adjusted.

But bad news is that its CEO Mr. Prakash Iyer has resigned.

Let’s see who will be the incoming CEO.

Investor presentation for Q2 results - The new product line up looks interesting

3 Likes

1 Like

This counter was badly beaten down in mid n small cap mayhem.

Bcoz valuations were too high.

But from last one year the management has become quite active. There is continuous improvement in sales,margins,Wc days etc.

N they are really expanding geographically.

In north region butterfly was an unknown brand but from last few months , i hv come across alot of Butterfly brand hoardings outside prominent stores.

Though competition is stiff n its not easy to gain Market from existing players, but it all depends what strategy they are applying.

Advertisement hv been mostly limited to hoardings outside stores only.

But yeah something is happening as far as geographical expansion is concerned.

2 Likes

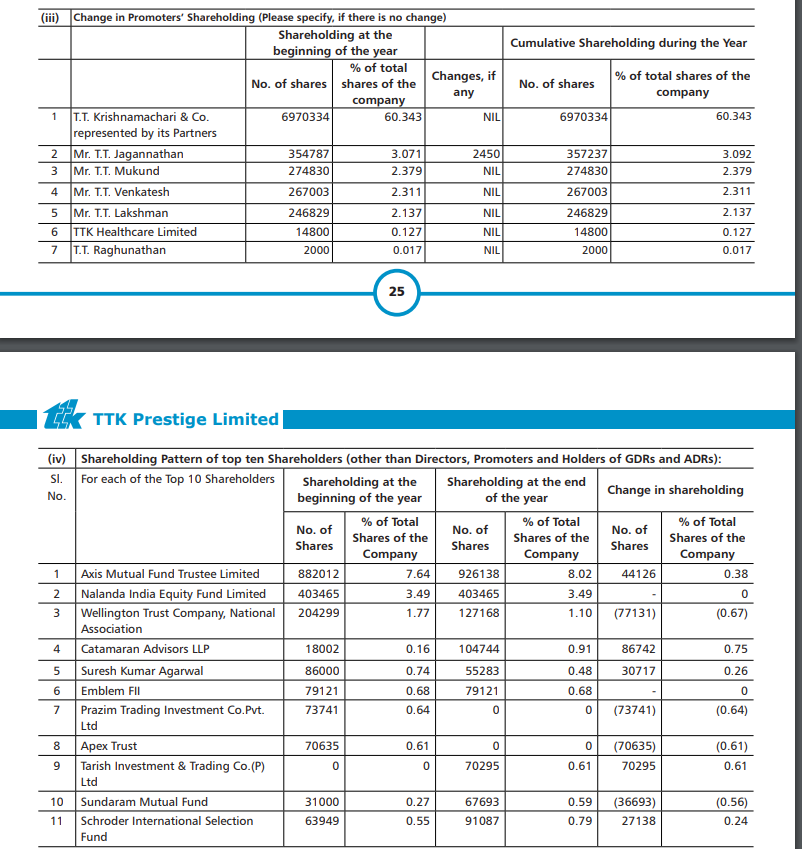

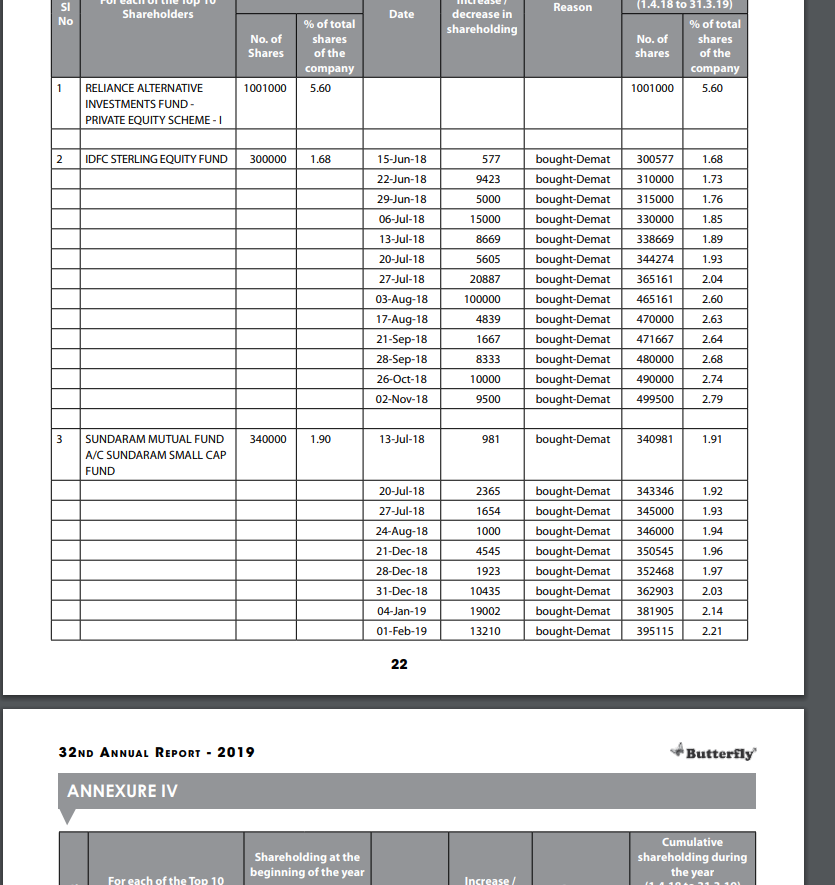

I think there is error in icici report… checked in both companies AR…dont find TTK holdings in Butterfly AR…

TTK AR page 24-25…

Butterfly AR page 22-26…

1 Like

Removing my post. Need to check again. I just glanced through the report. Thanks.

Looks like will do 13 cr PAT in fy 20. 34x P/E. Margins are half of peers. Prakash Iyer left in 2018. on financials company seems to have done well, delivered growth and margins. View : indifferent to buy here.

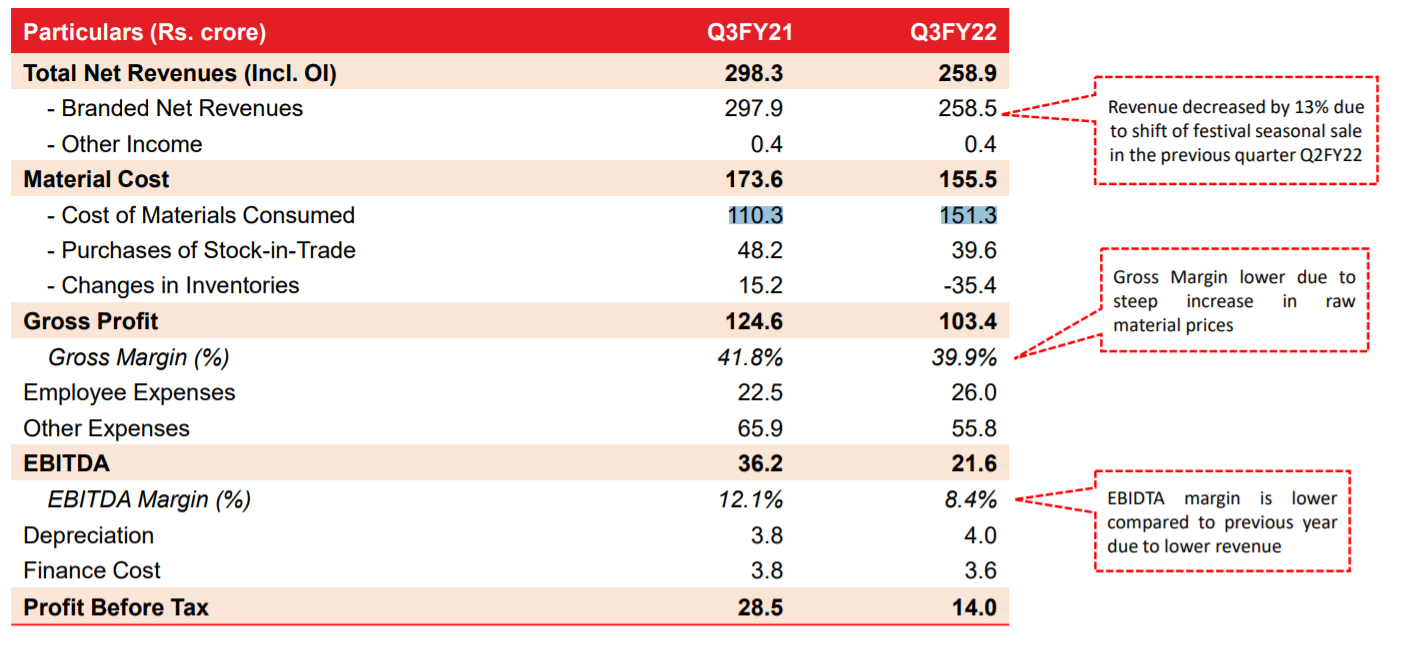

The Pent Up Demand effect or sustainable Recovery?

Rev 289crs vs 241crs up 20%

Ebitda 34.6cr vs 21.39cr +61.7%

Ebitda % 11.9% vs 8.9%

PAT 17.19crs vs 8.37crs +2x

EPS 9.52 vs 4.50

CFO - 133crs vs 12.78crs

Co used all its FCF in paying of debt of 103crs.

And after 4 years they will be paying dividen of Rs.1.5/share

2 Likes

Q3 - Result came out. In line with Q2 performance. Highlight for me is - Interest cost reduction by about 45% against Q3’FY20.

UAFR31122020.pdf (2.7 MB)

Q3FY21

Rev up 70% to 298crs vs 175crs

PAT up 16.85x 18.71crs vs 1.11crs

EBITDA UP 2.8x 36.22crs vs 12.86crs

EBITDA% 12.15% vs 7.3%

Pat Margin 6.2% vs 0.63%

Pat margins r effected due to high tax rate 35%

wats astonishing is that it was a non-seasonal quarter

Their online presence esp on flipkart is really strong.

Though mgt doesn’t share the share of online rev but i think it has become significant now.

2 Likes

Company is providing the guidance for 10% Ebita. They already have revenue run-rate close to Rs.300 Cr/Quarter. At 120 Cr. yearly EBITA, What does it mean in terms of upside/downside potential to have Rs.1,000 Cr. market cap in this Industry(Consumer durables with TTK prestige being closest comparison).

TTK with about Rs. 300 Cr yearly EBITA trades at Rs. 9000 CR market cap

1 Like

Impact of lockdown in TN. The Q1 would be difficult for the company from demand side, raw material increase and plant shutdown

Q3 results announced!

To me results are lack luster compared to previous quarter. But the stock is up 10%. I am puzzled.

Exactly my point. Operating leverage in reverse is playing out and profits are down 50% YoY. So wondering why the stock didn’t react on a day when the whole market was down. On the contrary, it was up a huge 10%. So what are we missing.

Investor Presentation - https://www.bseindia.com/xml-data/corpfiling/AttachLive/87e7dea1-3865-41d1-ac08-fbd5f93d9073.pdf

So for those who do not want to go thru the whole prezo, this slide seems to tell the reason for the decline in sales this quarter:

I think reason-respecting bias is at play.

While declaring Q2FY22 results, ‘shift in festival’ was not mentioned as a reason. The reason stated was: Revenue grew by 40% led by growth across all Channels and all product categories.

Also, I am uneasy on reading the note (on slide 14) - Bill Discounting: Successful implementation of bill discounting facility has reduced the debtors by Rs. 33.1 crores. The bill discounting facility can go up to Rs 50 crores in the medium term.

The moment above amount is added back, below note becomes Null and Void (no progress in Debtor days):

Relentless focus on improving Branded business debtors days have now started yielding results

➢ Currently stands at 41 days in 9MFY22 vs 52 days in 9MFY21

Disc: No position, but reviewed to sense the sectoral drift.

3 Likes

Am wondering if the markets got wind of this and that is why the stock is holding out despite weak results:

And so it happened! The offer price is close to current market price. So no big benefit for small shareholders.