I agree with your observation. I am from Pune. 4 months ago I was searching for gas stove and visited shops. I noticed Prestige as 1st product. Vidiem was really appealing aesthetically. I bought Vidiem and suggested my mom and in-laws in Rajasthan to buy the same.

3 Likes

There is nothing different to red flag in current quarter’s Profit. Only tax is charged negatively and that could be checked. With tax, profit could be lower.

Excise duty is nil now. It was 17 cr earlier. So, somewhere in tax all these will come. If all is going to come on expense then we won’t see this good looking profit.

I was checking relative valuation.

If I see TTK Prestige, IFB Ind, Hawkins cookers, etc then I find that it is not relatively cheap. PE is not comparable but P/S is. Where it stand on relative valuation!

Disc: Not invested.

Q3 result:

http://www.bseindia.com/xml-data/corpfiling/AttachLive/e8356257-dbef-4af0-a81c-b2254cf61845.pdf

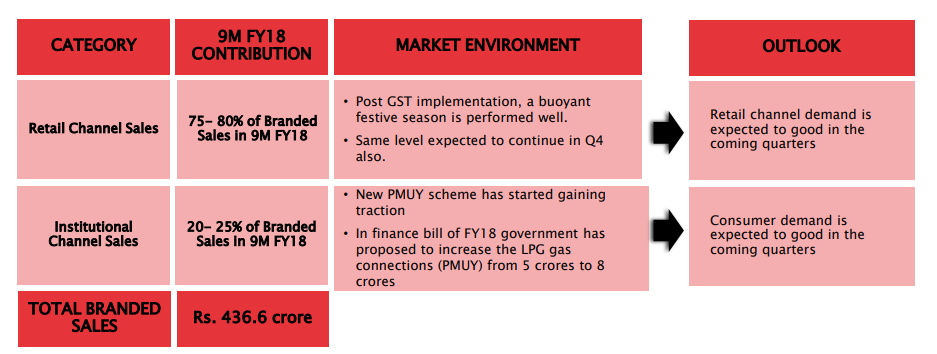

EBITDA margin is down QoQ. They might be offering discounts to counter competition. Please share your thoughts as well.

The difference in margin QoQ comes along with a drop in sales, which is a worry. Unless there is a seasonal component to their products.

Given that Q3 was festive season, sales must actually be higher or even remain at Q2 level. Something might have happened with institutional sales in Q3 as they form 20-25% of the overall sales

Request others to chip in with their inputs.

Investor presentation for Q3:

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=723a7c12-0f48-4d36-a12b-9cf8c8d0dd46

Brilliant results from BGIL…Turnaround story very much on track. Hats off to the management execution.

- Topline growth of 76% YoY ( Complete outlier in its sector)

- Bottomline at 1.9 Crs Vs (26.1) Crs

Slide No. 27 and 28 give a lot of insights into their turnaround plans. Company is on track to achieve a turnover of around 700 Crores in FY19 and 900 Crores in FY20. Continue to believe that is deserves a market cap of Rs. 2000 Crores at least, based on FY19 expected PAT of around Rs. 40-50 Crs.

One of the best operating leverage stories around with ever improving balance sheet.

3 Likes

Thanks for starting the thread. The turnaround story looks good .2 questions

- Do you understand where the growth in recent quarters is coming from ? What are they doing differently ? Is it just renewed focus on Branded business ? What are they doing on ground to achieve that ?

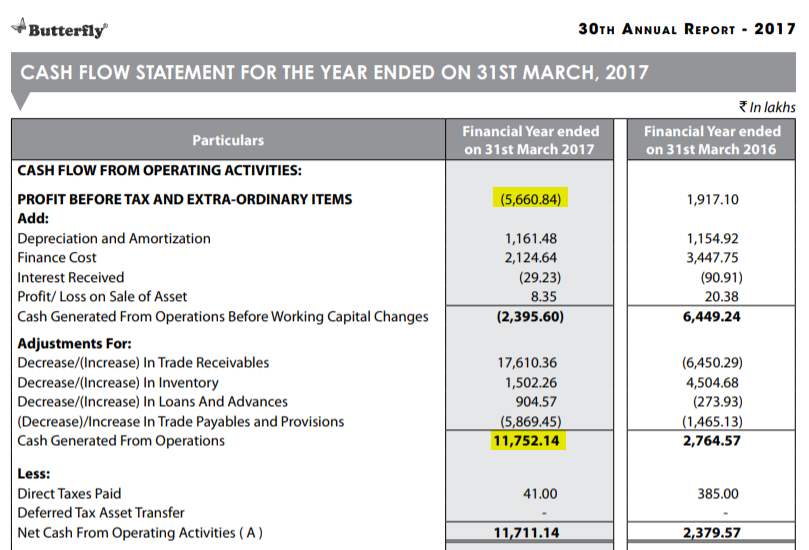

- 2017 PAT is negative but the operating cash flow is positive. Do you understand why .

I am following this thread and trying to understand more . Not yet invested .

Thanks. Most of the increased operating cash flow is because of decrease in trade receivables. Is this because they exited the government business this year ? I would think that is the most likely driver and hoping cash flows will be stronger in the future too .

I have my doubts on all companies (mostly Jewellery companies but there are others too) that had dramatic cash flows in FY17, especially when it wasn’t the case in previous years and when the EBITDA doesn’t correlate.

3 Likes

Can you please specify those jewellery companies? Thanks in advance

So u mean to say that working capital and non cash expenses wer tailored to make the cash flows positive??.

Interesting take…how do u co relate ebitda to cash flows…usually everyone criticise ebitda saying it is not a measure of cash flow etc etc…

But u hv a different perspective…

Looking at cash flows in comparison to ebitda…

Do u look at ebitda/ cash flow for ten yrs and suspect something is cooking if the gap widens ?? Like the ratio was in some range and suddenly left track eg: lets say it was ebitda was around 60% of cash flows and all of a sudden it became 20% …something like that?? …how did u co relate…

what’s our view on how the Q4 results would be?

Decent results and shows a turnaround promise. Despite markets not rewarding. Reason of not meeting expectations or am I missing something hidden under the reported nos ?? Any forensic analyst to decipher the nos ? Please enlighten

Had a glance at 2017 AR and below are my quick notes:

- Cost of material consumed is 26% of last year but scrap sales remained almost same. Was scrap generation increased and if yes, what were reasons.

- Dies and Tools are more than 50% of new addition to Fixed Assets. It means that the company is required to change or maintain it at higher rate. Depreciation Rate is only 11.88% and as on 31.3.2017, Dies and tools value is 50% of Plant & Machinery Value.

- Trade Receivables include Retention Money by TSCSC. Why it is classified separately and not disclosed if it is due for a period of more than 6 months or not. If it is long overdue, what are the chances of recovery and why any provision is not made.

- During 2015-16, purchase of finished goods was Rs 31 cr and at the same time stock of traded finished goods was Rs 41 cr. It means that there are chances of some goods not moving or moving slowly from earlier years. Further, during 2016-17, purchase of Rs 79 crs and closing stock is Rs 26 crs.

- Sales reduced due to only brand sales but still purchase of traded finished goods increased. Why outsourcing was done when you are not fully booked.

- There are related party transactions w.r.t. purchase & sale of goods/services which means other related entities are in same business.

Disclosure: Not Invested. Started tracking.

2 Likes

Hi, the results were a tad below expectations. The turnaround remains on track. Not giving any importance to the bottom-line due to obvious reasons. However, I was expecting topline growth of at least 30 percent (as against around 22 percent posted by the company). However, for FY18, the company closed at around Rs.535 Crores topline which translates to about 30% topline growth. The story remains intact.

FY19 Topline- Rs. 650 Crores (21% YoY growth).

FY20 Topline: Rs.845 Crores (30% YoY Growth).

FY20 Profits: Rs. 50 Crores (6% NPM)

- These are my own figures arrived at by my interaction with multiple industry participants. Please take it with a complete bucket of salt

Ultimately, this remains an operating leverage play but is operating in an intensely competitive environment with an ever improving brand recall. How much should be valuation for such a company? Would you be elated if you get a strong consumer brand (one of the top 3 kitchen appliances players in India) growing at 25% topline CAGR and operating leverage yet to play out at just about Rs. 800 Crores Market Cap, I leave it to you guys to decide.

P.S: Invested and strongly biased.

1 Like

Just saw a TV interview if Mr. Jaganathan of TTK prestige.

-

rural demand is picking up and this they are launching specific product targeted for rural

-

Will increase their advertising spend for rural

-

Looking for and in consideration for acquiring a branded player in their segment.

While the consolidation is good for the industry, I don’t know of any other ( smaller ) player which could be a potential acquisition target other than Butterfly.

3 Likes

Q1FY18 results out:

1.26 Cr vs 0.45 Cr PAT QoQ

30% revenue growth YoY and 12% QoQ

@maverickroger This time there is a 30 percent topline growth. Would love to hear your thoughts on results for this quarter.

3 Likes