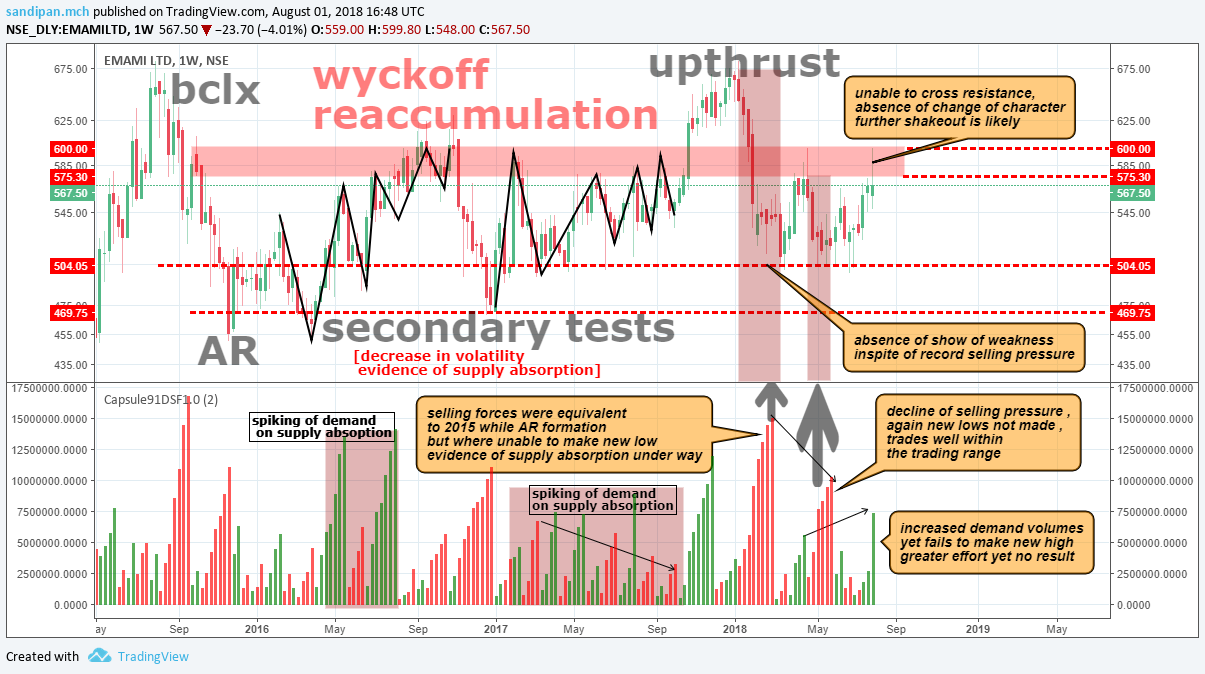

2 cases of excellent accumulation worth tracking…

emami and greaves cotton…

both i believe are at the exact same position in their accumulation phase, which is the phase d

the ultimate phase of the schematics…

and both faces the same challenge in their trading range…

none have shown the ultimate breakout change of character…

I track the fundamentals of greaves cotton,

management discussed Greaves 2.0 strategy, a 5 year plan to de-risk engine business by becoming fuel agnostic and reduce the share of engine business to 40% in overall revenue by growing aftermarket and other segments. In an effort to de-risk engine portfolio, Greaves is transforming itself into a fuel agnostic player. For this, Greaves has partnered with Pinnacle Engines of US for launch of CNG & Petrol variants and for Hybrid and Electric variants it has partnered with Altigreen Technologies of Bangalore.

Greaves has indicated that technology demo for Hybrid and Electric variants are

complete and further evolving of specs for the final phase of development is under

progress.

With Pinnacle it is planning to launch two engines one for 2 wheelers with

range between 110-115 cc and for 3 wheeler Greaves is planning to launch product

in the range of 200-240 cc which it believes would take about 2-3 years to bring it to

mass production level.

Greaves has signed with major OEMs for BSVI diesel 3W engine which is coming to

force from April 1, 2020.

the company launched two new powertrain solutions at the Auto Expo 2018 one of which

is a new family to multi-cylinder turbo-charged intercooled engines which are BSVI compliant and a lithium ion battery based ev powertrain for 3 wheeler

Engine business accounts for 51% of revenue,

Aftermarket accounts for 25% and rest all account for 24%.

.Auxiliary Power segment market share has increased

from 3.5% to 6.5% and has increased the range from 500KvA to 1250KvA.

In the farm equipment segment it has 45% market share in the Petrol/Kerosene pumps

and is planning for electric & solar pumps in near future.

Aftermarket accounts for 25% of revenues and the

portfolio can address 80% of 3W ecosystem with Greaves own parts and multi

brand spare parts as well. Greaves Care an asset-light service model aimed at

addressing complete service needs 3W & 4W. Currently 51 outlets are functional

and Greaves is planning to launch the service across India in a phased manner.

Management quantified the annual opportunity size for this segment at ~Rs. 25 bn.

AS of FY18, greaves has EBITDA margin of 14.2% , PAT margin of 11.3% , long term debt free, ROE-21.4% and RocE-18% , 916cr reserves and surplus, 238.4cr operating cash flow , and present market cap of 3571cr…

attached here the lastest investor ppt

the biggest concern to me is , any upgrade by customers to 4W LCVs might disrupt 3W LCV volumes which is the stronghold of GCL.

disclaimer… no position, tracking