Bajaj corp…

WIth plans mentioned in the q1 concall to conduct price hikes in fy19, and crude likely to soften a bit, margin pressures are likely to come down …

Bajaj’s key raw material, LLP, Light Liquid PAraffin, (a derivative of

crude) witnessed a price hike of 46%…

Expansion of distribution network, good monsoon and good rural demand of ADHO , should drive the margins and topline…Light Hair Oil category in rural grew 9.8% in value and 6.7% in volume terms in Q1FY19

rupee likely to appreciate in coming quarters, bodes well for the figures too

traction is expected in the NOmark cream segment also s trade pipeline was cleaned up for Brand restage in Jun 18.Company expects 40% of incremental growth to be fueled by

new innovation and launch which is expected in the next 18 months as guided my the management although A&P spends are expected to rise…

Also the planned increase in direct distribution would increase costs in short run, plan is to nearly-double its direct retail reach targeting to cover 540k outlets directly by end-Mar’19 vs 280k at Mar’18.

in Q1fy19, Volumes for its flagship brand BAD , Bajaj almosd drops, grew 11.2% record high seen in the past 13 quarters and outpaced the growth in LHO (+6.7%).

Domestic volume growth at 13.9% and retail-level offtakes,which are free of base and destocking-related issues, grew 10.2% during the quarter.

Guwahati plant capacity utilization stands at 70%.

Construction of Baroda facility to commence in Q2end and the plant will cater to one third of capacity needed for future. Guwahati plant capacity utilization stands at 70%.

Management sounded bullish about the business in the Q1 call…

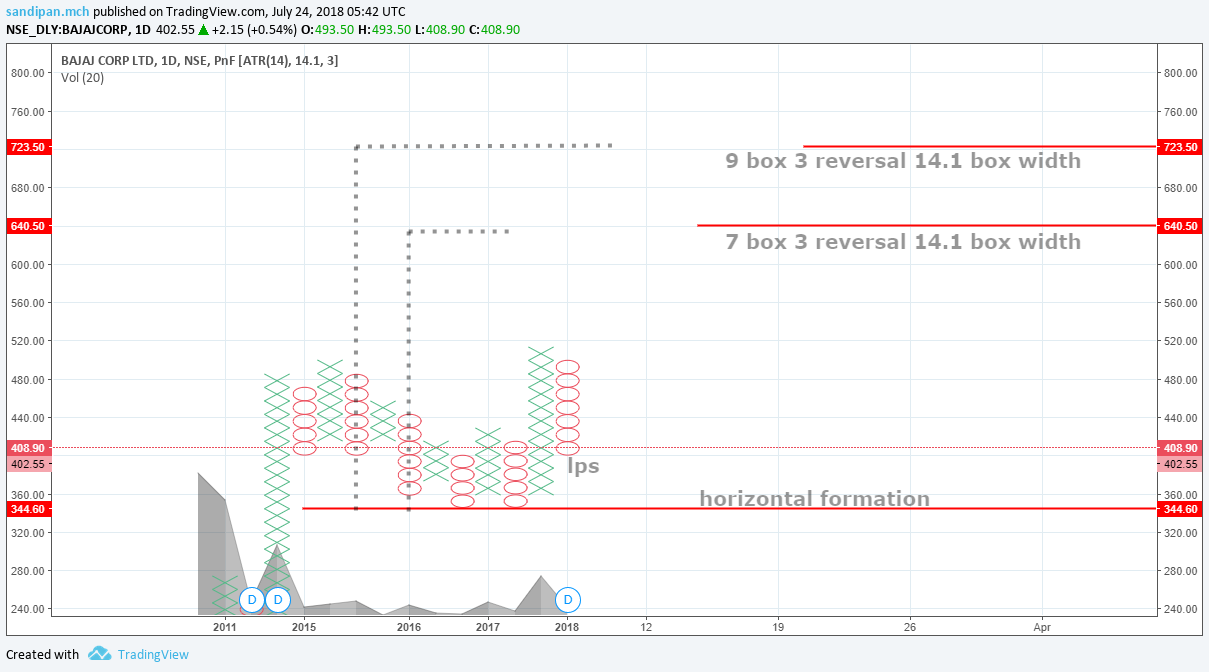

Market seems to have been factoring this in

and hence the wyckoff reaccumualtion spotted in the charts…

wyckoff reaccumualtion

Disclaimer… tracking, no current investment