You are absolutely right! The pre IPO shares were locked in for 1 year and it got unlocked earlier during February 2018. The board took notice of the situation and approved the buy back at a very opportune time - when the free float was expected to increase significantly.

Considering BSE is not allowed to have a promoter group - the long term holders can exit at any point in time. Boards decision to buy back should have ideally protected any downward risk - but surprisingly in this case it is working out in a totally different pattern with price falling by more than 15% from the time buy back was announced and now the delta between the approved buy back price and market price is in excess of 25%. I guess either we are not aware of ‘something not so good’ which is cooking in the background(and a few big investors who are selling now are aware of it!) or just that this company is having few large investors who are in desperate need for money and ready to liquidate at what ever price they can get.

Small share holders are the real beneficiaries when the company has a reasonable number of strong and deep pocketed investors who hold significant majority of the shares through thick and thin(indirectly creating scarcity premium in market) - TCS, Maruti, HDFC, DMart etc good reference points for this. Hope BSE is able to attract the attention of quality investors investors soon.

Disclosure: Invested in BSE and have added during the current fall!

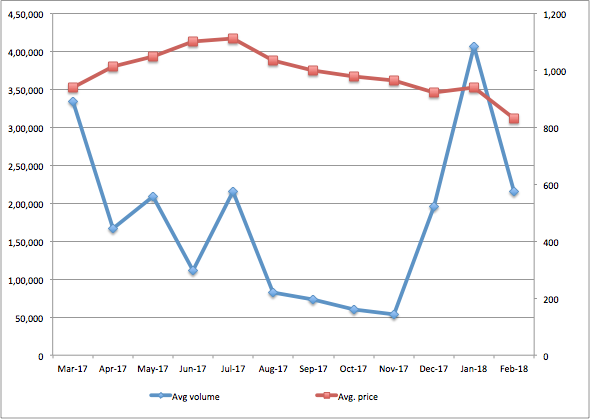

I was intrigued by sustained price erosion for BSE in last couple of months. Here’s is the plot of BSE average price and average daily volume:

Pls note that I’ve not take first month of listing (Feb’17) in this chart as volumes were unusually high.

Referring to this post :

The spike in volume is from November 2017 as can be seen in the graph, and price continued to be coming down unabated since Aug 2017. So there’s something more than the unlocked pre-IPO shares here.

Regarding buyback, BSE is steadily buying back its shares (roughly 15k per day since Feb 2, 2018) which is only 7% of the daily average volume, which, in my opinion, should not impact price trend much.

Any comment from technical point of view by veterans?

Disc: Invested, and added in last one week.

With the beating it receives on a day to day basis despite the management’s foray into several new segments of business, ongoing buyback what is that retail investors like me should or failing to see?

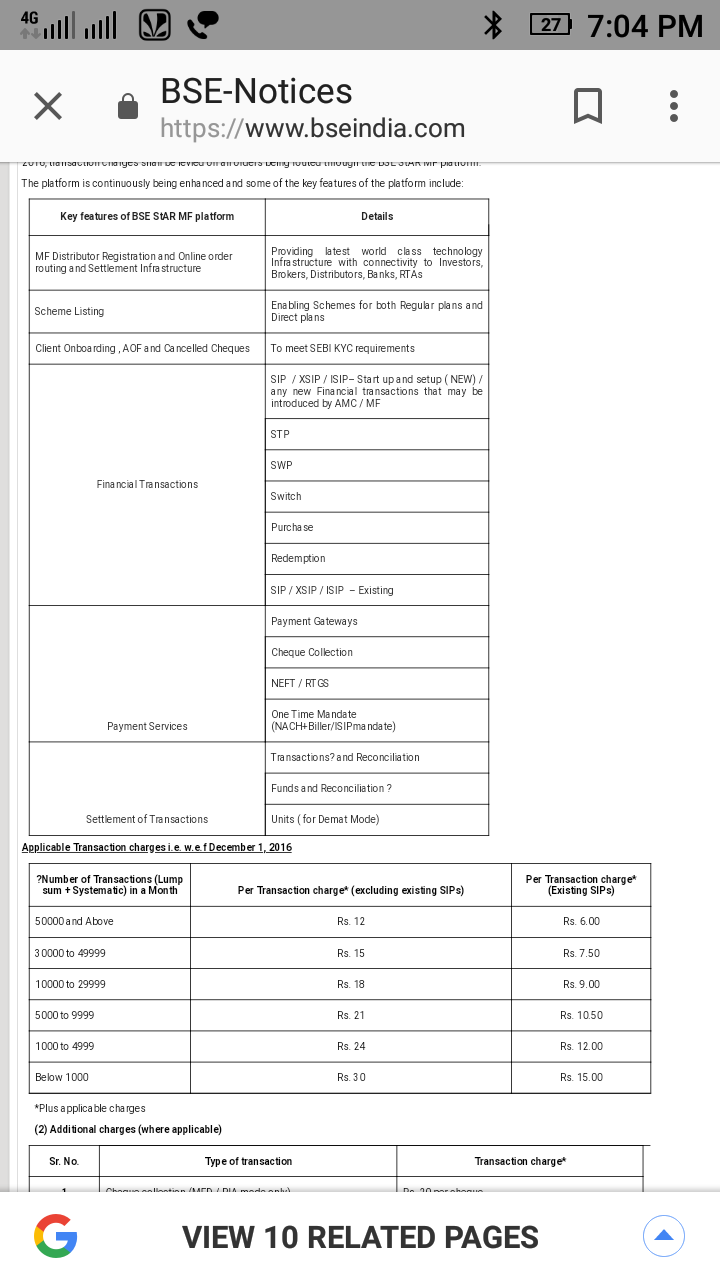

Anyone knows who all brokers are using BSE star MF platform ?

How it works ?

All the MF direct platforms today like Zerodha Coin use these kind of platform ?

Lockup period is over, so insiders/pre-IPO investors are running for the gates. Those that bought during IPO with blue sky dreams and comparison to NSE’s P/E ratio might also sell due to price action from lock up selling, so downside can be very high for such a stock in such a market.

Disc. Not invested, tracking to see if I can get stock 30-50% cheaper

This stock will not come below 600 in any case, Market capitalisation is half way secured by cash on balance sheet.

company had chosen buyback policy very well taking into consideration the unlocking of shares ,buying shares in lots thereby increasing number of shares that can be bought and therefore it will increase future valuations. If it will trade 50% from this price then dividend yield will be same as bank FD.

The commodity business will add further revenue after October onwards. Transaction charge will be Rs 1. at start.

The way INX volumes are surging, definitely derivatives on which bse was lagging behind will start giving revenue soon in this year itself. ( (avg contracts traded : 18000* TC 8-9rs *22days )*12 - 18 crores expense ) annually ( avg contracts traded on DGCX singapore and ICE exchanges are 80000 contracts,out of which rupee dollar contracts share is more than 80% which is yet to start on inx )

Assuming Rs 8-9 (12 cents) from above message as transaction charge of sgx and Dubai exchanges are charging approx .096 dollars. In investor presentation it was wrong written as .96 dollars.

The best thing which I noticed that members of inx are trading on s&p BSE sensex50 index even though nseifsc giving them nifty50 to trade.

Approximately 100000 Transactions per day * 6-30 TC avg:15 *22days *12 months =39.6 cr annually revenue will get added from bse star MF platform.

If only we could be so sure about life. Markets are without an iota of doubt unpredictable and often irrational. I won’t comment on the investment worthiness of BSE. But, I’ve just one thing to share- Expect the unexpected in markets which are seldom efficient, governed by the emotions of the various moving parts. When markets fall, people can rarely resist the temptation to sell, even if it’s a loss, because there’s the desire to conform with the larger group- the group of sellers. When people become irrational prices also can become irrational.

In last few years , in best of times company has made 250 cr profit n in worst of time 150 cr approx (considering cyclic nature of overall operations ). If one considers normalized earning somewhere in between ,it comes around 200 cr. 1600 cr on books is pure cash so deducing this from market cap, we are left with almost 2400 cr . So , basically at 0 growth we are getting it 12 times earning. Considering oligopoly business with lesser chances of disruption , survival years should be in top 25rh percentile on grading of companies . There are 3-4 new initiatives where company is building leadership position and not generating any revenue but spending 10-20 Crore annual will sooner or later start generating profit or in worst case will be shut down which means approx 15 cr of additional profit . So, chance to lose money looks lesser . Rest time is best teacher. . Disc : 3.5% position around 770 Rs. Accumulation in progress

Saurabh, if you are removing the cash from the market cap. then you will have to remove the investment income as well that is generated from this cash to compare the reduced market cap. to reduced earning. Then you will get the PE for the core operations.

Abhinav’s point was : let us say i want to own BSE . I know market cap is 4000cr ,so, to buy whole BSE , I need to pay 4000 cr and I am getting 200 cr of normalized annual profit . But I am getting 1600 cr of cash on books . So , indirectly I am paying net net only 2400 cr. But when I take net net 2400 cr price which I am paying , I should not consider 200 cr of annual normalized profit because a part of that profit is also coming from the other income generating from interest generated out of this 1600 cr cash on books. Let us say the interest on this 1600 cr is 5% which is 80 cr. So if I consider net price being paid as 2400 cr. My net annual income is 200-80 cr =120 cr . I pay net 2400 cr to b.So,my valuation multiple changes from 2400/200 to 2400/120 which is a big change n more logical. Though I ve not done detailed calculation , I will tweak it a bit. In order to calculate true normalized annual income , I must reduce other income from worst year and best year and then take a normalized core profit and then add other income based on current cash on books and then final total annual normalized profit. As now other income forms significant part of total profit , I think even normalization need to be dealt with care as normalizing total worst n best overall profit vs normalizing worst n best core profit plus other income can make good 10-20 percent difference in calculation n it’s the core business which is cyclic n hence only that part of profit need to be normalized. Will check AR numbers n do the calculation but broadly n this is what he meant n this is what I am going to do .

Saurabh, it is also advisable if you work at a PBT level because taxation of investment income and operating profits are different. It will not be as simple as removing the investment income portion of the other income from PAT. Some of their investments are tax-free while some are not.

As it has been discussed here, most of the cash and investments on the B/S are from deposit and margins, an investor will have to consider it as part of the core operations as it is encumbered capital. So 1600 cr is what can be theoretically taken out so we will need to see how much income only this money makes and reduce that.

I believe even this 1600 cr is not removable, here is a verbatim note from AKC’s 21st Feb interview on CNBC, "Financial institutions need to be robust with capital to build confidence. There is a certain amount we need in regulatory capital. For us we require around 100 cr capital, but INX requires 500-600 cr regulatory capital. Trading side requires minimum 100 cr, clearing side requires 300 cr. There is a framework of a waterfall for the risk management in clearing corporations where a large portion of capital goes from stock exchanges. We have close to around 1800 cr capital left after the current buyback. We may have 400-500 cr extra on our balance sheet, but if you consider the regulatory capital requirement for the next 2-3 years, it is not much. It is not that we need to use that capital but it needs to stay on the balance sheet. Because of that, the board has taken a call over the last 4 years that operational profits get redistributed to the tune of above 90% and will continue going forward.

Overall, we don’t need to raise capital from markets and we have buyback and we have a framework where we give out most of our profits."

. Disc : 3.5% position around 770 Rs. Accumulation in progress

. Disc : 3.5% position around 770 Rs. Accumulation in progress