Hopewell has officially changed to Borosil Limited.

With the competitor’s margins normalizing in the future and Borosil’s market share increasing it will be an interesting tug of war in the opal space.

The management has been explicit in acknowledging the tail wind of adoption of glass and conversion from plastic to glass and in this concall anecdotally he says that a lot of office goers are adopting glass boxes which in my opinion is quite true. Additionally the ecommerce channel will be the major point of sales for this office goer category. The contribution from this sales channel is expected to grow to 10% this year and they are hoping it will reach 1/5th of the sales in a year or two. I feel it could be faster seeing online adoption.

They seem to be doubling down in a startup fashion to grow the consumer side albeit rationally to always be profitable.

And it is our belief that in consumer products, it is important to first achieve momentum and market

penetration and then focus on containing cost to gain economies of scale. Of course, it will not be growth at all costs. We will be profitable. The growth eventually has to be sustainable and has to be sustainable for our channel partners as well. We will continue to invest in brand building so as to create a strong consumer pull for our brands.

In this concall he even calls out the good feedback Borosil products receive on Amazon. Borosil’s 400ml box is Amazon’s recommended choice for lunch boxes with over 3000 reviews. The next best has roughly 1100 reviews.

I have also been observing Larah gift packs being gifted for purchases during Diwali at places like Max Retail stores (instead of say a cahsback or discount). I dont know how the feedback loop would have worked there akin to ATL advertising I believe?

Rgds

Deepak

disc: have increased position in recent market correction. views might be biased.

Recently, I got a chance to interact with CIO’s of 4 big mutual fund houses and I asked them what do they think made most of the returns for them. I want to write it out in the context of Borosil here.

Management Change - The example I got was how his fund house made money in Indusind Bank when the management guard was changed.

Alignment of promoter’s interest with shareholders - The management is in midst to merge its all unlisted and private subsidiaries. The example I got from the CIO was of Minda Industries.

Revival of Strong brand - The company is trying to leverage its brand strength to grow its consumer division which is clearly visible in numbers also. The example I got was of Eveready industries when it was trading at 20 odd rupees.

Alignment of interest of management with the company - Company introduced ESOPs for its top management. No example was given as such for this.

Finally, the intent of the promoter & its integrity - Borosil’s promoters were guilty of dubious activities. With the change in guard, all the issues have been resolved point by point. The intent of promoter is clear that they want to grow the business. It is visible in sales, market share and product portfolio growth.

@ 2200cr market cap, I think this company offers a good runway for secular growth. We will keep have to check the growth numbers continuously and if the management walk the talk. However, if management is able to achieve what they have said by 2021(margin expansion towards 18% EBIDTA and combined sales growth of ~18%), the company can double from these levels. I will post my calculations in due time.

Disc. Invested (5% PF currently) from quite a while and have traded in the stock in last 90 days.

It seems Borosil management is really focused on simplifying the corporate structure of the company. In addition to the plan of merging Hopewell , Vyline and Fennel investment into Borosil as well as separating Gujarat Borosil from Borosil Glass, now company has wound up two Dubai based entities - one fully owned and another one in which wholly owned subsidiary held 49% of the shares. Big to the management for walking the talk…

A week back ICRA had reaffirmed its ratings with a watch for Borosil Ltd (Hopewell).

They point out the positive areas as strong parentage of BGWL & operational efficiency improvements. On the negative side - the capital intensive business. Report is attached.

Specific paragraph related to Borosil reads as below

The chargesheet adds that the UCC modification was done without the consent of the investors.

“UCC modification was done rampantly through two conduit accounts, without consent of account holders. ARCL used the account of its client Borosil as the conduit account to buy commodities without consent of the client…… trade modifications worth Rs 1,061 crore were carried out in the account of Borosil.”

Not sure if this means possibility of any financial gains to Borosil as stock is up 1.3% today after a long time downward trend. Can anybody decipher this?

My concall short notes jotted down during Q&A session today. Hence listed in the sequence of the questions asked during the call.

• Adv and promotion expenses 8% of the consumer business

• Klass pack – growth of 21%

• 15 people at Borosil Technologies for new and innovative products.

• EBITDA grew by 32% to 64 Cr for 9 months.

• Adv and promotion higher by 10Cr for 9 month period.

• PAT growth of 10.6%

• Process of restructuring, NCLT hearing on Feb 12th. Hope to complete in next 6 months.

• Lunch box category could be Rs. 1000 Cr

• Margins will increase as economies of scale accrue.

• Total 12,000 outlets – 55% to 60% will be for Opal and others for glass, volume discounts given to retailers/trade as sales promotion

• Pricing – anti dumping duty helps, no price increase taken. Idea is to increase penetration, to improve capacity utilization, to motivate people to move away from plastic.

• Borosil Ltd will remain unlisted for 2-3 months till they reapply for listing.

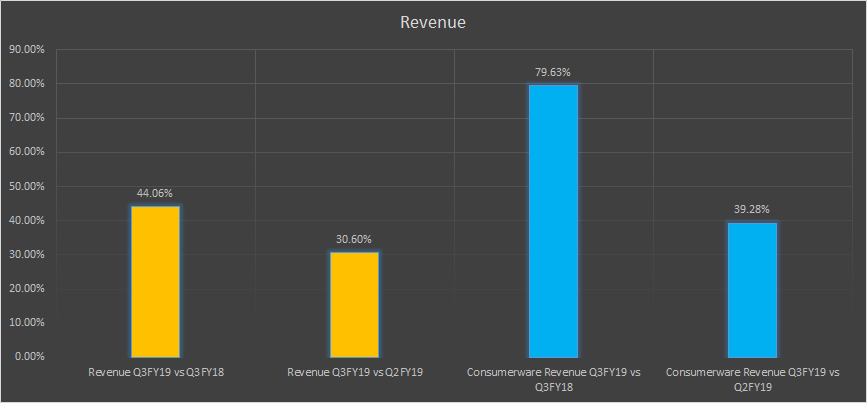

• Larah has grown 48%, volume growth would 42%. Some market share growth. will wait for La Opala results. Market growth is very good.

• Interest cost is higher this quarter for small working loan taken at 9-10%. Mostly returned by now.

• Net cash on books – 110 Cr

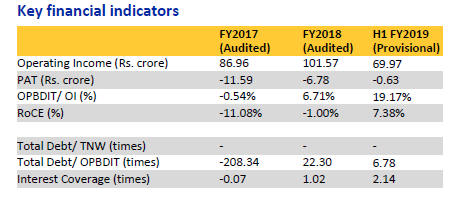

• 9 months results - Hopewell – 117 CR/18% EBITDA (79Cr/7% EBITDA last year), Klass pack 31/4% EBITDA(25/12% EBITDA last year )

• Spend around double amount that of TTK prestige for advt and promotion. Once volume grows, adv spend as % will reduce. That will improve net profit margins. No change in gross margins

• 75%-80% capacity utilization as of now. We can go above 100% capacity by squeezing productivity

• Next Capex planning may have to be done by Dec 2019

• Other expenses – 51 to 73 Cr for 9 months. Most of it from selling expenses. Freight also gone up in line with increased sales. Impairment of investments also there (mark to market? ) Legal and professional fees more this qtr due to merger and demerger related activity.

• Sales - 117 CR Larah (79 Cr) – 9 months , EBITDA – 20.8Cr (8.5 Cr) – 9 months

• Hopewell - Loss of 1.4 Cr for 9 months – Int and depreciation

• We would like to be Pan India brand. South we are weak. Like to focus on South – relatively untapped market.

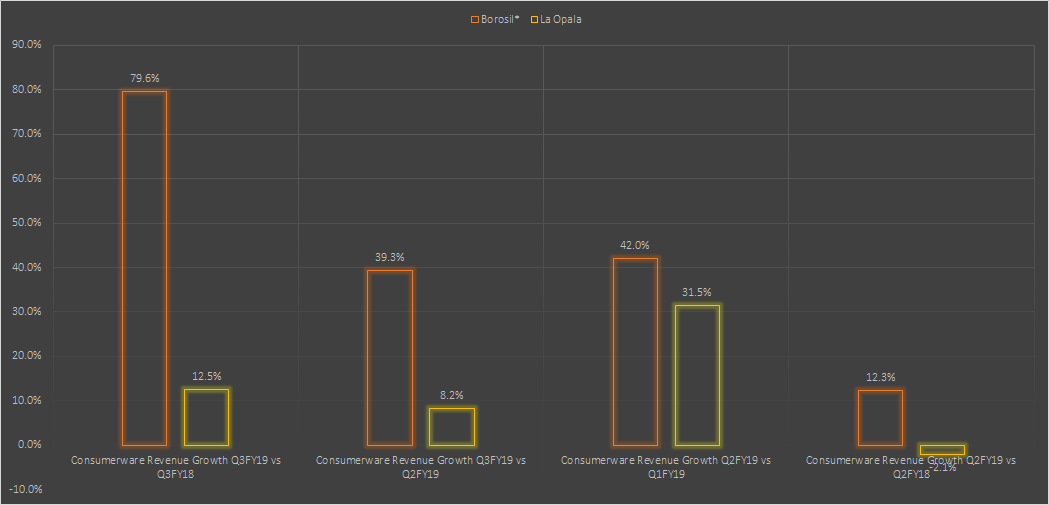

Its true that LaOpala is loosing market share but it raises few questions

They are not yet utilising expanded capacity… even they are expanding their facilities & will be adding more in next 4-6 quarters

They are protecting their margin %

They are not aggressive enough in marketing campaigns

I understand that Laopala management is well aware of above mentioned points.

Are they waiting for right moment or they just wish to protect their EBITDA / profit margin? They must note that it will not be easy to recover lost market share.

True. Agree with you that in this game recovering market share will be perhaps difficult. LaOpala I believe is not spending much on advertisement whereas the Borosil Management in every call has highlighted the willingness. I could not join this quarter’s call due to time constraints nor have I read the transcript yet. @Marathondreams would have a better idea. As per previous calls Borosil management has said that the market itself is growing and that is what they are liking.

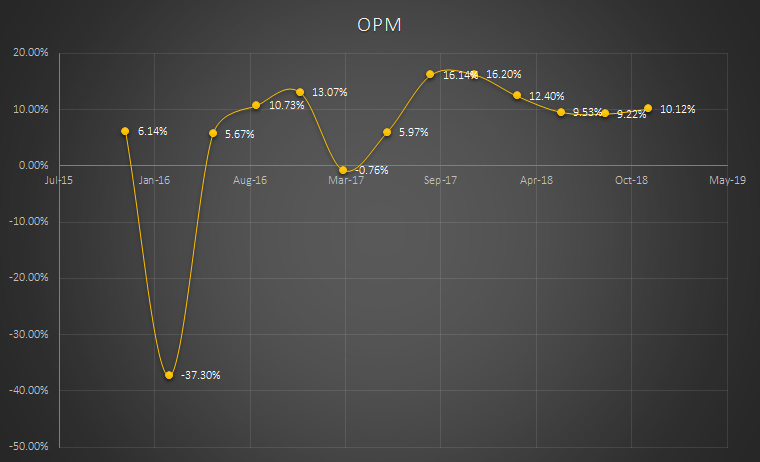

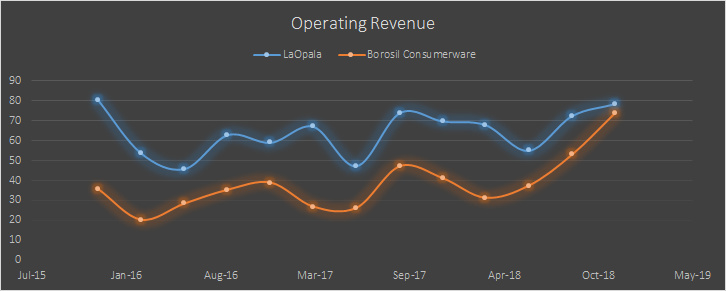

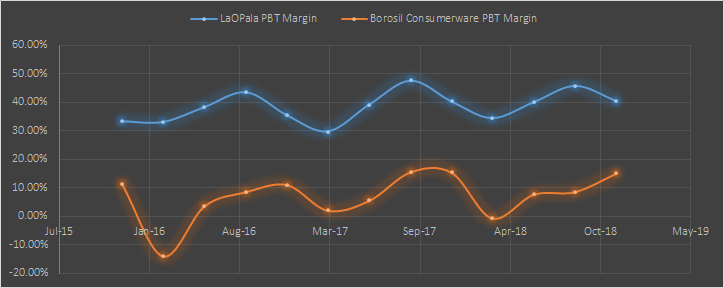

The stark reality comes when we see the below chart.

I don’t have access to operating margin of Borosil’s consumerware business so I had a look at the equivalent PBT margin. Point is to note the graph from April 2018 onwards.

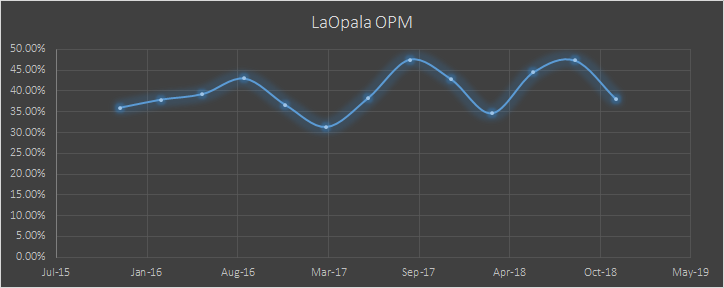

This quarter LaOpala has lost a mammoth 9.3% since Q2 in OPM and 4.3% YoY. On PBT margin terms Borosil Consumerware has almost doubled its margin since Q2 and remained flat YoY. LaOpala has also remained flat on PBT Margin terms YoY but has lost a significant 5% over Q2 on PBT Margin.

So I doubt their margin is getting protected.

To capture market share one must be willing to spend/reduce margins (in this case), to regain market share is an uphill task not only in terms of spending money but replacement costs for already acquired consumers.

It seems La Opala management is pretty conservative and is having “ostrich” moment about its market share. They are more interested in protecting their margins rather than maintaining their market share. On Borosil concall, someone asked Mr. Kheruka if Borosil is gaining market share or is it purely due to market expansion. He was candid in his response. He said although there is no doubt that market is growing, he will wait for his competitors results before calling out his market share gains.

Now since La Opala results are out, it is clear that Borosil is gaining market share as of now. It would be interesting to watch how La Opala reacts to its unutilised expanded capacity, when it comes online.

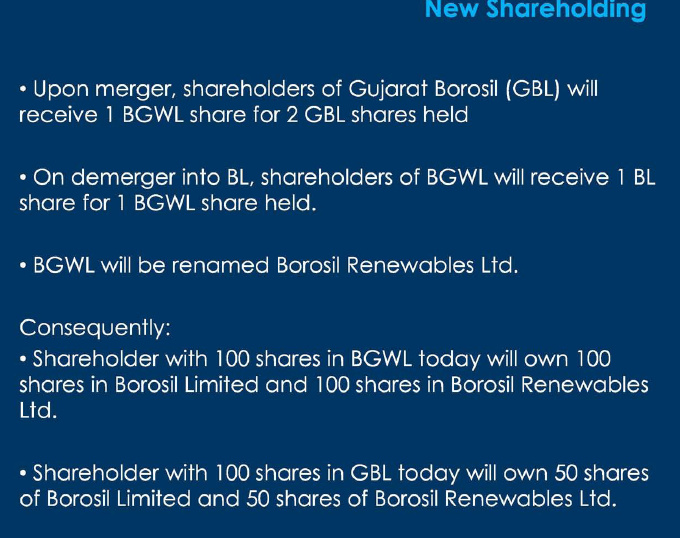

Any further update / clarity on the swap ratio / arbitrage would be very helpful. As per the quarterly investor presentations uploaded by the Company (snapshot below), person holding 200 shares of GBL (cost at CMP ~Rs. 17,000) will end up owning 100 shares of Borosil Limited and 100 shares of Borosil Renewables Ltd. Alternatively, person holding 100 shares of BGWL (cost at CMP ~Rs. 21,000) will also end up owning the same 100 shares of Borosil Limited and 100 shares of Borosil Renewables Ltd. Thus, buying GBL is clearly more optimal, and I presume the crossholdings / pref. share holdings (already highlighted in the thread)vwould have been factored in while arriving at above swap ratios. Is there anything I am missing here? Inputs most welcome.

to the management for walking the talk…

to the management for walking the talk…