Any sign of manufacturing numbers like vakrangee or manpasand?

I think you are following this company for 2 yr. I have just invested inspite of agreeing with your comment about management quality.

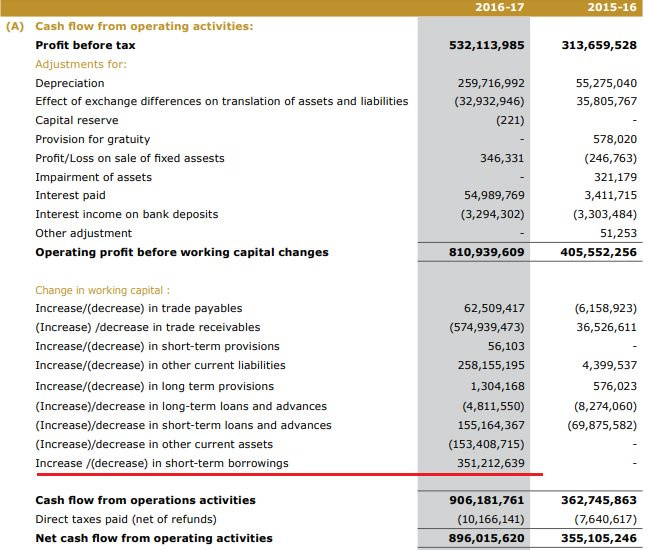

If they are having reserve of 164 cr why they have borrowed 44.6 cr during 16-17 and they have paid 5.4 cr of interest. They have received interest income of 32 lakhs on their investment.

Not able to understand. Could somebody explain? Thanks in advance.

I think the cash held by this company is parked in their UAE subsidiary. If they bring this cash to India they will have to pay substantial tax on it. I have found management reluctant to get that cash in India.

I am very new here and still taking baby steps in increasing my knowledge. So please let me know if I am making any error in the following observations:

The GOI has recently increased the validity of eVisa from one to two months. Further this eVisa can now be applied two times in a year across three categories: tourist, business and medical. Earlier it was tourist only. This will certainly impact the visa business of BLS as the number of eVisas has gone up substantially.

It may also be useful to try to obtain feedback about their services. A relative of mine living abroad is very angry and upset saying that their service was very bad. I understand reviews about the various embassies on Google may help. This may have a long term effect on grant of future contracts to BLS.

On the other hand, the margins in these services are quite good which could add to the bottomline, especially with the UK contract.

Be that as it may, I personally feel, even after having a look at the company financials and projections, earlier high levels of stock price may not be seen for a long time.

Regards

Sandeep

Disc: Not invested and do not intend to

This definitely needs further analysis…

But in a reflex to answer to this, i remember asking them about this in q3 concall about the possible threat to the visa outsourcing business by evisa in the segments bls operates…

There was a surprising reply as to that the evisa process is actually done by the outsourcing service providers themselves, so it is not something that goes out of the market share of the companies… And the margins in the evisa processing , if comes to become the mainstay, can be even better…

This is not correct. The Government of India operates an independent website for eVisa. The payment made on this website goes directly into GOI coffers. Any outsourcing agency can offer assistance to an applicant in filling an online application, which has to be done at their centre, but the charges for this assistance cannot be greater than the service charges agreed as per the contract. There are hundreds of look-alike websites presenting themselves as GOI visa websites which charge significantly higher fees than GOI website. . It may be that some of the outsourcing companies too operate such websites, but I doubt if they would include these profits in their main company.

Does that give a fairly reasonable explanation?

Regards

Sandeep

Disc: no holding, just want to contribute to the learning which I myself am taking a lot of!

All cash in overseas subsidiary, large debt and large receivables. This is reminding me of 8k Miles, going just by the balance sheet.

I see that debt jumped in FY17 and that they took this up as they couldn’t bring back the cash from foreign subsidiary (?). I see that fixed assets jumped from 24 Cr to 78 Cr in that year but in current year, the fixed assets down to 40 Cr. What happened there? I see something about Pubjab e-Seva project and the govt.'s inability to settle the receivables. What has happened here to the fixed assets?

A lot of distribution seems to have happened going by the shareholding pattern. The cosy govt. link, G2C business and the run-up post demonetisation and the eventual distribution, seen along with the what seems to be big write-offs, along with piling up debt, overseas cash and large receivables etc. are enough red flags here I think.

Yes, since the finance costs are almost zero, so it makes sense to inflate cash flow, for no reason at all, just to make people who do not read ARs (and somehow still know and care about the Cash Flow), happy!

This is on a much smaller scale…

The management in concall.didnt give guidance regarding what kind of revenue to expect…

But there are some positive from this renewed contract…

Now the revenues will be received upfront and no receivable dues issues will be there and from that they are going to share some portion of the revenue with the government , again no numbers share whats the gov share of this…

No new capex required for this and it will be ebitda positive from the start…

The uk contract should adjust the loss lf punjab revenue and add some surplus…

Also they refused to disclose ehats the share of sofra in the uk contract and said they are under strict nda…

The italy contract should be negligible in addition…

With starfin acquisition, neither already generated revenues of the organization was shared, nor eatimates of the contribution , but mentioned that the investment will breakeven in 2 to 3 years… so that gives a rough estimate about the earnings from there…

Withlower margin pu jab contract, out of the mix…

With uk addition, the emargins should become better going forward…

Punjab dues to be recovered within next quarter and debt repayed by then, was the guidance given…

100cr of the receivables came in this quarter from the gov…

15 tenders are upcoming in next 2 years in the visa business…

Regarding domestic egov they mentioned same old 8 to 9 tenders but no time line shared regarding bagging them…

Regarding cash in the balance sheet, they mentioned, they need to keep the cash to apply for tenders and growth objectives and since th3y were sure the receivables would come back they didnt want to bring it to india and pay the debts and inturn pay tax to that… Better dividend payouts increases tax outgo hence they prefer to conserve cash in the oversea subsidiaries…

Revaluation of asset was done in fy18 and hence the depreciation costs have come down…

They gave some vague exolanation regarding y thr cost of services have come down saying the quality of the services has become better and also increased vas contribution has led to lesser cost of services, dont know what they were trying to say…

From starfin the revenues come from sbi and is received within 30days …

Attending the companies concall isbecoming increasingly useless as they are more interested in tell stories rather than numbers…

Been a consistent follower of your posts and gained a lot of insights from you, thanks!

I started following BLS international a while ago due to its attractive valuation.

Could you please elaborate on your point - “A lot of distribution seems to have happened going by the shareholding pattern. The cosy govt. link, G2C business and the run-up post demonetisation and the eventual distribution”- further?

GOI has now announced that eVisa will be valid for one year, with multiple entries. This extension is valid for Tourist and Business visa. This obviously has the potential to affect the revenues of BLS from this segment. Further, the business from Punjab govt. is just another business from a govt entity. Such businesses suffer from the vagaries of the bureaucracy (delayed payment, lesser than expected revenue owing to “overheads”, change in policy etc). Personally, I remain unconvinced about the valuations of this stock, as I feel that this is fully valued at present. I also have reservations about the management, particularly after the transcript of the concall posted above in Aug '18. On the other hand, the growth rate and the returns given earlier are, I must admit, attractive. Overall, a bit of a risky venture, for me.

Comments, especially critique, welcome, as I am still learning.

Attended the concall. Management did not inspire confidence.

Initially guided for 10-15% top-line growth in FY20. When that led to more questions by investors, they revised it upwards to 15-20%!

Complete lack of clarity on the huge cash balance of Rs 180 crores. No buyback, and dividend payout is still ~10% only. ‘Needed for upcoming tenders and business development’ was the vague answer. Points like ‘increasing people on the ground’ etc etc doesn’t explain much.

The management at one point actually said they did not want to disclose much strategy on the investor call. Lol. Why hold one then?

Approx Rs 34crores of other income due to sale of fixed assets (related to the Punjab contract) to the government. Apparently the government has yet to accept this valuation and the auditors have qualified the audit report in this regard. They have recorded the amount anyway, and claim to have begun receiving payments for it.

No satisfactory explanation as to why the margins have dipped so sharply, despite being asked by a participant. Rs 12 crore of one time expenses were touted as a contributor, but in-spite of these, EBITDA % would be sub 10%.

Segmental margins were given as 10-12% for government revenues and 17-18% for visa processing! Disconnect??

On the plus side, Punjab receivables down to Rs 118 crores, with a further Rs 25 crores received in 1QFY20. Punjab revenue was Rs 15 crore for the quarter, Rs 52-55 crore for the corresponding quarter last year.

New countries added to visa bouquet include Vietnam and Lebanon.