This successful trial by Roche can potential shrink herceptin market. Can somebody quantify the impact considering market sizes of herceptin and pergola ?

@rks00 ?

Perjeta has to be administered with Herceptin. Therefore Perjeta will have no effect on the usage of Herceptin. Ms. Shaw commented a few days back on TV that given a choice for generic Herceptin doctors may in use instead of brand.

Sharmasks,

Thanks for sharing the link, I saw this article a few days back. The article seems to be mixing up several issues,

The following is based on my understanding of the issue and my prior fact finding on the same, and therefore could be inaccurate

- Biocon has exclusive rights for CanMab in India. There is no revenue/profit sharing on the India sales with Mylan. In so far as RoW goes (except developed markets) Biocon has coexclusive rights, the right to partner with other companies (does not have to partner with Mylan) ex - Lab Pisa in Mexico etc.

- This is where I’m not a 100% sure - Mylan was involved in this case as the combine Biocon & Mylan were using Roche’s Trastu data in package inserts in their respective markets to prove safety and efficacy of the drug. Roche challenged the use of this data. The lawsuit was filed in India to get Biocon to stop manufacturing the said drug.

- The court ruling opens up 2 additional applications for the use of CanMab in India only (so far) which should be revenue accretive, by how much? I’m not sure, need to find that out.

- For impending sales in the US & EU (after approvals) Biocon will have to revenue share with Mylan in those markets, as Mylan will be the marketing and distributing partner and will incur costs for all further legal challenges in those markets.

This is my understanding of the ruling, I could be wrong. I guess we’ll have to wait for the next con call to get clarity

Thanks

@sharrmasks

Both Canmab (Biocon) and Hertraz (Mylan) are the same Trastuzumab developed by Biocon-Mylan partnership, marketed in India as two different brands under coexclusive marketing. Both will be competing for the same marketshare and i assume there wont be any revenue sharing in India and ROW (excluding Europe , US and few others).

Regarding Perjeta (Pertuzumab, Roche,Aphinity trial) : perjeta is effective only if given along with trastuzumab, so it wont be a big problem for Biocon unless Roche give a deep discount for perjeta combined with their own herceptin. Biocon will need to price their Trastuzumab more aggressively then. Also trastuzumab itself is 90 % effective in EBC (early breast cancer), so addition of perjeta has to show a significant survival advantage to swing the opinion of prescribing physician ( Aphinity trial data regarding how much perjeta improves survival is still not publicly available)

2 Likes

Mylan-Biocon can launch Trastuzumab in Europe as soon as they get EMA approval.Europe patent for herceptin expired in 2014.

US launch by 2019(patent expiry date) post FDA approval.

Fear of litigation delaying launch averted.

http://finance.yahoo.com/news/mylan-announces-global-settlement-license-120000482.html

3 Likes

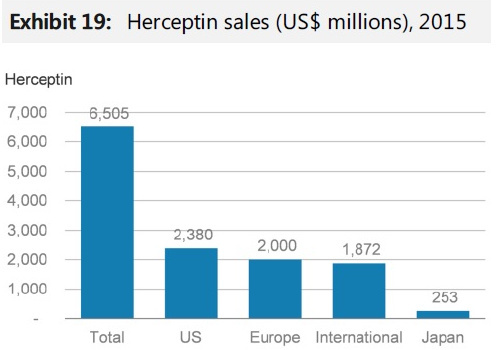

We know that global market for Herceptin in 2016 was around $7b. I could not find the break-up regionwise. What could be the sale in Europe?

Also do we know what will be the break-up of revenue between Mylan and Biocon, once the medicine is launched in Europe?

What could be reasonable estimate of revenues flowing to Biocon because of Trastuzumab in Europe and US?

Any pointer how we could be make a reasonable estimate will be helpful?

- European sales of herceptin for 2015 was 2 billion$.

-

Details of revenue sharing between Mylan -Biocon is confidential. Your guess is as good as mine

-

With the recent ‘global settlement and licence agreement’ between Mylan and Roche, launch of biosimilar Trastuzumab will definitely happen provided they get FDA and EMA approval. Also, the Biocons Bangalore facility needs to clear the coming FDA and EMA inspections ( March-April).

Although the ‘license effective dates’ are confidential, it is reasonable to expect European launch by 2017 -18 and US by 2019-20.

Two questions that troubles me are

1 )Will Roche enter in to similar licensing agreement with other companies planning to launch biosimilar trastuzumab ( Samsung-Bioepis, Celltrion, Amgen)?-probably yes.

- Is Roche is very confident with their APHINITY trial data that they feel biosimilar trastuzumab won’t be a threat to their franchise?

Perjeta (with Herceptin) is already the standard of care in more than 30% of HER2+ breast cancer case (Neoadjuvant and Metastatic). The success of APHINITY trial could potentially allow approval of perjeta in the ‘adjuvant setting’ also. Adjuvant chemotherapy account for the majority (60%) of breast cancer chemotherapy followed by metastatic (20% ) and neoadjuvant (10%). With the success of APHINITY study, Perjeta, in combination with Herceptin, has the potential to become the standard of care in 90% of HER2+ breast cancer. This will allow Roche to sell Perjeta and Herceptin as a package at same price point as current herceptin alone, but majority of total price in future will come from perjeta and not from herceptin any more. This will seriously dent the prospects of any biosimilar competition. So your third question ’ What could be reasonable estimate of revenues flowing to Biocon because of Trastuzumab in Europe and US? will depend on whether perjeta- herceptin combination become the standard of care. In that case the prospects for biosimilar trastuzumab won’t be as bright as I previously thought.

Since the Biocon management has given a revenue guidance of 200 million from biosimilars in 2019, they might have already factored in all these and gave a conservative estimate. Also being potentially the first to launch, Mylan-Biocon can garner good market share and revenue before the impact of Aphinity trial kicks in.

3 Likes

Thanks @drmithunraj

If Roche launch Perjeta only in combination with Herceptin & the results of combination are far better than Herceptin alone then doctors will have no option but to go for it. In this scenario the option of going for Generic Herceptin with branded Perjeta do not exist. This could be a really big threat for Biocon. I fully concur with you.

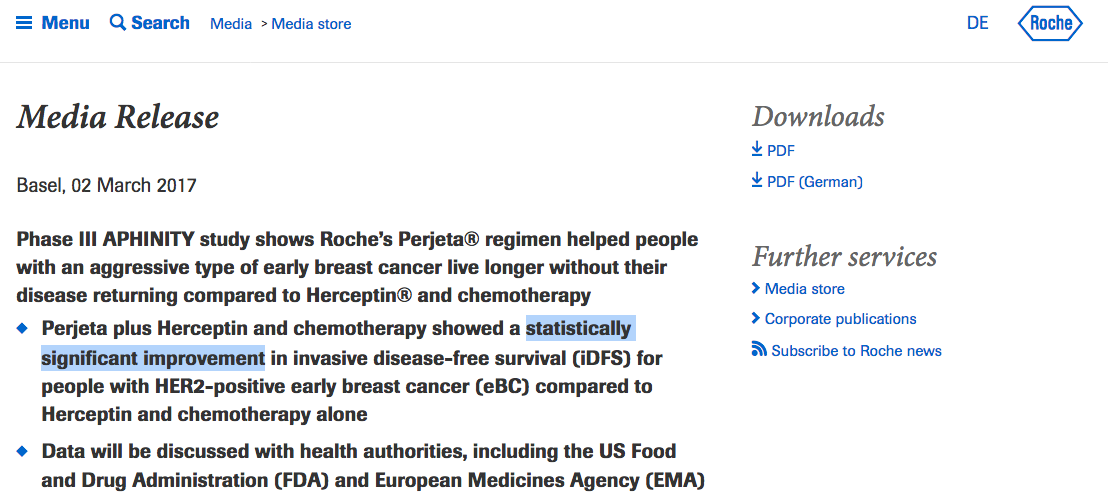

I found this press release where Roche has said that the combination has shown statistically significant improvement.

Why Biocon does not reveal the arrangement between itself and Mylan? I think the agreement is biased in favour of Mylan.

There are many if and but at this point. We need to wait to see if Biocon will be able to make any reasonable money out of this. The the has run up to much on expectation.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=f2056a0b-ed4c-4910-8b36-62314d3ee6de

Biocon considering bonus issue in April 27 2017 board meeting

Thanks

Biocon recommended 2 bonus shares for every one share and a final dividend of Rs 3 to shareholders.

Thanks

The top line has decreased (or at most remained steady) as compared to both previous quarter and last year.

As per the results, the revenues for the Month ending

Mar 2017 - 6321 M

Dec 2016 - 6550 M

Mar 2016 - 6459 M

Considering the approvals, especially for Biosimilar for Trastuzumab over the last one year, I had anticipated a steady growth in top line. Especially considering the untapped market for the same is huge and margins are good. In fact, for December results (with impact of demonetization), the revenue was reasonable. From January onwards, we would have wished it to go higher (by January, many of the cities at least, which would be a market for Biocon), the impact had reasonably minimized. But the sales are less. I am not too impressed with the results; my expectations were higher. Anyways, this is only my perspective; I havent gone through the report in detail and will read it soon.

The profit is looking high because, they have recorded an entitlement of Rs. 1042 M in its standalone results (MAT credit on sale of equity shares of Syngene)

I don’t bother much about the bonus; it’s more of a mathematical re arrangement.

Disclosure: Invested.

I agree I was also disappointed by the numbers and had hoped for a better quarter. To some extent this quarter was also impacted by fire in the syngene facilities.

Disclosure: Invested

I think the impending US and EU approvals are more important than quarterly numbers. That’s the only reason why we are all invested (I’m presuming) as that would be truly orbit changing.

Additionally, I don’t stress too much about quarterly performance, seasonality or the Syngene fire impact, if you look at the full financial year, they had a great year & I’m more than pleased with their performance.

4 Likes

What happened to the EU inspection? It was supposed to happen in April. Any news!!

Agree with @rks00 . The only reason I have invested is with the expectation of exponential growth following US and Europe approval . Things seems to be on track for the same. Expected glargine filing for US this quarter and adalimumab for US and EU shortly.

@Gaurav_Agarwal, FDA (and I assume EMA also) inspection of Bangalore facility is over. The management didnt comment directly regarding the outcome, but what I could gather from the conference call transcript was that there was no major issues.

Another recent development was US FDAs tentative approval (TA) for fingolimod (gelenya) in multiple sclerosis. Its a 2 billion opportunity opening up in 2019, although there are already 8-10 players with TA. Also whether Biocon has a para 4 filing with potential for 180 day exclusivity is not clear.

Investor presentation, April 2017, uploaded on biocons site is very informative regarding competitive landscape of various biosimilars that biocon is involved in. Attaching the link below.

2 Likes

Hi,

My understanding is US FDA inspection was due only in Sep/Oct-17. EMA inspection was supposed to happen in Apr-17. If inspection took place and information is not in public domain I will be surprised!

If such is the case then we should spend time on EMA website to look for information.

Could someone throw light on valuations. It looks expensive. Thanks

Form 483 USFDA for biocon

None of the observations looks like a show stopper to me. But then I have zero knowledge in interpreting it and my opinion is biased.

Anybody with experience please comment. @rks00

This is very disappointing. This just shows once again that companies cannot choose to differentiate in quality within its own plants. Quality should be a culture. You cannot choose to have one set of quality for plants exporting to the US and another for plants catering to developing economies. The chain is only as strong as its weakest link.

3 Likes