@rks00

Very detailed and compelling analysis indeed.

A very quick glance into the investor presentation page 19 (http://www.biocon.com/docs/IR_Prstn_Feb2016.pdf) shows that lot of the original drugs for which Biocon is creating biosimilars, lose their patent rights by 2018 ( In fact the big ones - Humira and Lantus with a total revenue of $22 Bn expire by end of 2016) . Wont this make Biocon compete with the generics instead of the original drugs and thereby lesser pricing ?

Already enough pressure on Lantus due to entry of biosimilars

My understanding of the industry is very low . Forgive naivety

Sourav, wonderful response. Appreciate the effort. In my attempt to answer your questions you have helped me discover the fact that, there is more competition for biosimilars than what is mentioned in the excel sheet screen shot in my original post. That being said, it is good to know that Biocon in partisanship with Mylan are among the first wave of biosimilar manufacturers along with Amgen Eli Lilly etc. So here is a brief response to your questions.

On Humira (adalimumab) - So adalimumab is a biologic. What you said is true that their “product patent” does expire in 2016, however they do have a patent estate for the same (process patent, formulations patent etc.) Also being a biologic it can not face generic competition. Generic competition is mainly for simple molecular structures, biologics are immensely complex to generasise so a generic adalimumab is not possible. An interesting link on the same, please note that this links highlights far more competition that my originally research foresaw, tat being said it is important to note, that a lot of these companies are still in the phase 3 testing phase unlike biocon that is in the filing stage. Also, another interesting point, there is no mention of generic Humira but only a biosimilar Humira due to the fact that it is a Biologic. - http://www.chicagobusiness.com/article/20151120/ISSUE10/151119787/dont-mess-with-humira-abbvies-ceo-warns

To be fair, Abbvie management threatens to sue biosimilars and hope to delay biosimilar versions of the same for 5 -10 years, chest thumping or hollow threats? Can’t comment! Only time will tell, but historical precedent seems to suggest the latter. I think they see the writing on the wall! (This is just my optimistic conjecture, it ultimately falls to US courts to decide and that is like a coin flip, hard to say one way or another, but the article above seems to surprisingly paint an optimistic picture)

On Lantus - I must confess, I am slightly lost on this one, here’s why - so the below link talks about generic and biosimilar glargine (Lantus) curiously though, the generics that this article describes are in FDA phase 3 testing!! Why is a generic going through FDA phased testing? This is unheard off. Bare with me, I’m still digging and trying to get to the bottom of this. If we could collaborate maybe we could seek the answers quicker. What on earth is a generic doing in FDA testing? (Important to note here that Biocon has completed phase 3 testing of the same and is about to file) But that aside, there’s something going on here that is different to other generics (or as we know them), this doesn’t make sense why this should go through FDA testing. Any help on this will be appreciated!

Binu, great note, just to clarify you need to look not only at Biosimilars, but any innovator company here in the US to check / verify whether or not they capitalize the final stages of their phase 3 trial that has been validated in another market or not? Additionally, this is not so relevant IMHO.

Whether they capitalize it or not would be a rounding error if the potential of their pipeline is as described in my original post. I must confess here, I grossly underestimated the competition, there are at least 2 - 3 other companies trying to manufacture biosimilars that are in either phase 2 or phase 3 stage for most of the drugs, some behind Biocon & some at same stage, but still, in the interest of a balanced discussion this recent revelation must be brought to light.

So I guess the focus should be on, what is the true potential of their pipeline, what are the risks that would prevent fruition, alternatively what events could expedite the same, the expected timeline of FDA approval etc.

On Humira…Torrent had launched Adfrar as generic biosimilar for adalimumab in Jan’16. This was second biosimilar for Humira after cadilla in the world. seems many players vying for Humira’s market($15bn) which is losing its patent this year. Not sure how Torrent and Cadilla planning to foray in US market for this blockbuster drug.

Thanks Naveen for pointing this out. Torrent & Cadila’s biosimilar is only for the Indian market, they have not started FDA testing in the US. Amgen filed in Nov 2015 a bio similar to Humira, the verdict is expected in Sept 2016 so looking forward to that.

As outlined in the link below, Phase 3 trials may be needed for bio-similars given that unlike SMD (small drug molecules) they aren’t exact copycats of innovator drug / original drugs. So efficacy, stability etc. needs to be established.

I think they are using the term generics and bio-similars interchangeably in the article about Lantus.They mean Biosimilars . Any more light on the competitive angle / moat ? I think we need to breakdown biocon’s pipeline and do a thorough understanding of total market, competitors , what phase are competitors in and then make some safe assumptions regarding the potential market share (and $ revenue upside) we can expect Biocon to make in the next 3-5 yrs. I will try spending some time on this through the week

" I think we need to breakdown biocon’s pipeline and do a thorough understanding of total market, competitors , what phase are competitors in and then make some safe assumptions regarding the potential market share"

True Sourav, couldn’t agree more. I have made a start in my original post, mapped out pipeline, market size, Biocon phase in testing etc. I am falling short on the competition front and haven’t yet mapped out the competition in its entirety. Any help will be appreciated, also any sources (ex: Orange book, purple book etc.) you could recommend that would be a good place to start mapping out competition?

Good write up on Biocon. I have been watching it for a couple of years now. Indeed, Biocon appears to be the main vehicle to play the biosimilars game. It has the largest pipeline of drugs.

Your write up talks about the potential opportunity and size of the US biosimilar markets and also the 4 main ANDAs which it expects to file in the coming months (Pegfilgrastim, Adalimumab, Trastuzumab, Glargine)

But, as per my understanding, Biocon has already sold the commercialization rights for these biosimilars for the developed markets to Mylan in return for cost sharing and profit sharing. I do not have the details of profit sharing, need to dig out more details. As per their deal with Mylan, Biocon only retains rights for biosimilar in the emerging markets.

You’re right Capwise, Mylan has exclusive rights to file ANDAs (incur all risks & legal costs) and market the same in the US while Biocon maintains rights else where. This is a profit sharing agreement, and the terms of these agreements are never known and are kept confidential. Biocon has done this as it does not have its own sales & distribution network in the US. This is standard practice of all Pharma companies outside the US that don’t have their own S&D. Example Alembic (till now at least, they are building their own S&D) etc. If one were to make an estimate of the profit shares one could look at other companies that have such similar arrangements with US companies (based on market share data & price data) can estimate total revenues & the % shares with the Indian / Foreign manufacturer. This profit sharing varies from 65-35 to 50-50 in most cases is my uneducated guess, as these are never disclosed publicly.

Hope this helps

To help on the pipeline competitiveness, i am sharing couple of documents from the JPM Health Conference 2016 which is considered as the top healthcare analysts meet.

Unable to retrieve the original link which i found through Google. Highly recommend to read the below doc to get better insight. 111315 Biosimilars Primer_compressed.pdf (834.6 KB)

Basically, AbbVie is confident of facing the biosimilar challenge on its blockbuster drug - Humvira.

The above link and the ppt explain in detail why AbbVie is confident.

IMHO, interchangeability and the BPCIA Patent Dance are key issues.

Couple of ongoing litigations should give more clarity with respect to BPCIA.

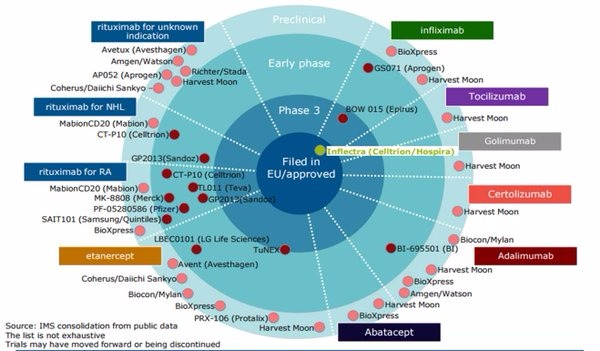

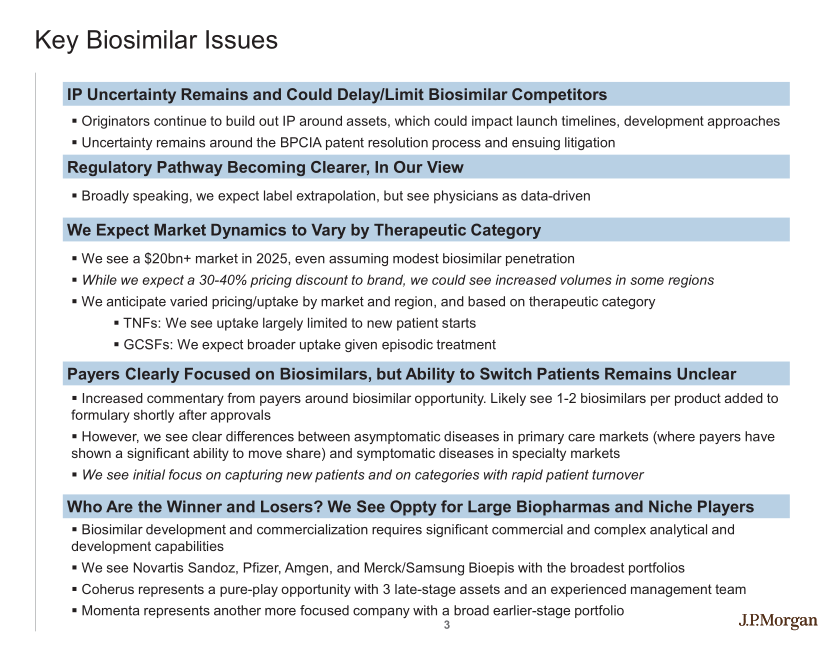

Given the intense competition illustrated in the above 2 heatmaps, i would prefer to wait to see how Mylan-Momenta biosimilars perform since they are likely to be marketed ahead of Biocon’s.

Vishnu, great stuff! Incredible research, thanks for sharing. Feel the same, waiting for closure on some of the on going litigation in the biosimilar space here. September will be an important month in that regard, and will help set a precedent, so waiting till then.

Excellent article on the current status of Biosimilar Regulatory Pathway in US.

FDA had just released the overdue Labeling Guidance last week.

Lack of Resources (Qualified Reviewers)

24 reviewers for 57 BLA receipts in FY15.

Review of Biosimilar Biologic Product Applications - Study of Workload Volume and Full Costs

ERG’s data has been collected in tables at the beginning of the report. While the number of total biologics submissions has increased every year from 33 in FY13 to 57 in FY15, and total workload has increased from about 86 FTEs (Full-Time Equivalents) in FY13 to about 126 FTEs in FY15, some aspects, such as the amount of time spent by FDA on Science and Research, and Training, have gone down. Overall, ERG estimates that FDA has spent a total of $81.7 million on biosimilars-related work over the first three fiscal years of the program.

BSUFA

Implemented at the the same time as GDUFA, Biosimilar User fees are aligned with the same payment terms as innovators pay for PDUFA, which is reasonable given the more complex nature and inclusion of Phase 3 clinical data.

It is due to expire in 2017 and FDA have started re-negotiation meetings for BSUFA II with industry.

Tried to create a conservative estimate of Incremental revenue for Biocon + Mylan from biosimilars factoring in competition and price decline . Assumptions

Revenue figures of 2015 from various annual reports of innovator company were taken

Only phase 3 filings by Biocon considered (probability of approval is higher)

Assumed prices will drop by 25% and hence the total market size will drop by 25% (Lantus biosimilars in Europe are 15-20% cheap )

Assumed innovator drug will retain 50% market share due to brand name and the remaining 50% will be split EQUALLY among competition (It may be aggressive. No precedents in bio-similars, Can be more conservative here)

Assumed no growth in demand from 2015 (to be conservative)

With all these assumptions, if we consider only the drugs whose patent expire by 2016 , Biocon+Mylan’s expected sales from Biosimilars could be in the order of $1 billion (I would think it will take 3-4 yrs for all this to happen post FDA approval)

@rks00 - Any idea about the split between Biocon and Mylan ?

Disclaimer - Not trying to forecast revenue but just trying to get a very crude estimate of opportunity size. All assumptions are questionable

Great work Sourav, I like how you presented your thoughts and your ball park estimate in an easy to follow method.

My estimates for Biocon’s incremental revenue world wide (not just US) is between $1.2 - $1.5B as compared to your conservative estimate of $1Bn just in the US. Again this is pie in the sky stuff, no one really knows how things are going to play out, legal delays if any etc. So your guess is as good as mine or any other’s for that matter. There are too many unknowns (regulatory, IP) & Mylan Biocon license agreement (which is confidential - the usual precedent varies from a 40-60 to a 50-50 ) so estimating numbers with any degree of certainty is going to be hard.

That being said, the larger point is that whatever be the end outcome, (your estimates of $1Bn in sales, mine or those of Morgan Stanely ) The 2 key points are

a. The potential of the pipeline is orbit changing,

b. As seconded by Morgan Stan in their recent report, the ,market is totally ignoring the pipeline, and will one day value it appropriately. I interpret that as a favorable risk reward. If it wokrs out and gets approvals, great! If not, dont see too much downside as the market is not pricing the pipeline to begin with. The MS report presented a wonderful comparative study of Biocon with Celltrion of Korea. Same story there, market ignored pipeline all the way till FDA filling (not approval) eventually got a few of their ANDAs approved, stock up from a $1Bn Mcap to $10Bn in 3 years. I wish I could share the MS report, its around 8MB (32 pages) the max limit of sharing a file here is much smaller.