Dear All,

I want to draw your attention to two posts on same subject and compare the tone .

So, a situation when the company got the rejection is being touted as a reason to rejoice. Yes - we heard that FDA did not raise questions on biosimilarity or efficacy of results et al. But FDA did ask more data and therefore cycle time goes up (at minimum).

The point I’m making is larger - I saw a similar commentary when the GMP concerns were raised by French authorities . Even the the company spun the story to be a positive one even though there was some 30 odd observations.

Is Biocon becoming one of those companies that is unable to be transparent with its investors?

Disc - I’m invested on the theme that everyone is but getting increasingly worried on reducing margin of safety (as BAU business seems to be going nowhere ) while upside seems elusive .

Agree, reduced my holdings as it reached my valuation target for 18 end already. I guess 3rd Dec approval is already priced in. Will increase my holding if corrects by around 15%.

May I understand your reasoning that the Dec approval is already priced in? We have no information on how much market share the biosimilars will garner at what price and biocon’ s share in it. How did you manage to value this at a 15% price range accuracy?

Thanks Doc for the update. This is good news indeed. On a shorter term basis however, a positive FDA opinion on the Pegfilgrastim biosimlar would really help boost both the top and bottom line for FY 19, not to mention a EU approval for Trastu or Pegfil (as they are both off patent in the EU). Keeping my fingers crossed for that too. The FDA crl for Pegfil was primarily due to non compliance to GMP, Biocon has received an EIR for the facility recently & reapplied. Hopefully the FDA would opine soon on that too.

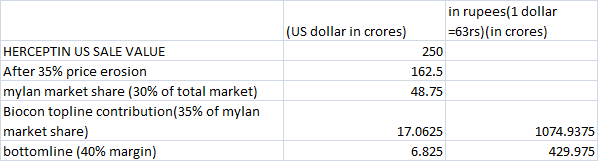

From what I gathered, Herceptin is about 2.5B market in US and given that Mylan has the exclusive marketing right and about 50% price erosion, the fact that Mylan has done some arrangement with Roche already - does this look like a meaningful impact to Biocon? (keeping aside the fact that the price movement would also be linked to having a proof point now).

This is a crude calculation with assumptions in xls ,as most details are not public.

(US dollar in crores) in rupees(1 dollar =63rs)(in crores)

HERCEPTIN US SALE VALUE 250

After 35% price erosion 162.5

mylan market share (30% of total market) 48.75

Biocon topline contribution(35% of mylan market share) 17.0625 1074.9375

bottomline (40% margin) 6.825 429.975

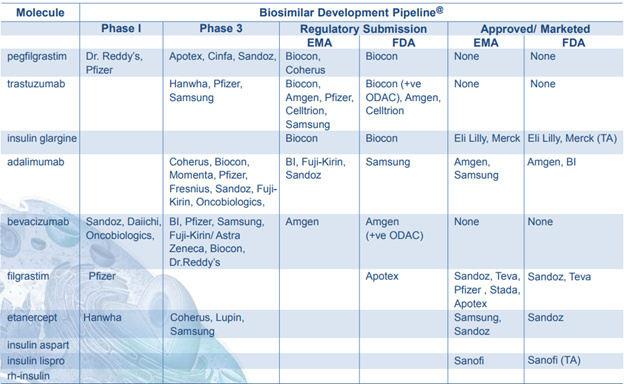

Apart from Roche (herclon), there are 7 other trastuzumab brands in India: Biocon (canmab), Emcure, Mylan( hertraz), Zydus, Lupin, Reliance life science and Torrent ( in descending order of marketshare).

Of these only Biocon -Mylan brand (Ogivri) was under FDA review and was subsequently approved.

There are 3 more trastuzumab biosimilars currently under both FDA and EMA review from Pfizer(Hospira), Amgen- Allergan and Teva- celltrion .

Samsung Bioepis Trastuzumab has been already approved by EMA.

Biocon in it’s annual report talks about their biosimilar pipeline. Interestingly the words used there were “disclosed molecules in our pipeline”. So, I believe we can expect some more “undisclosed molecules” to be disclosed in future? Thinking like a “detective” or just “wishful thinking” ? I can rest my expectations based on readers comments

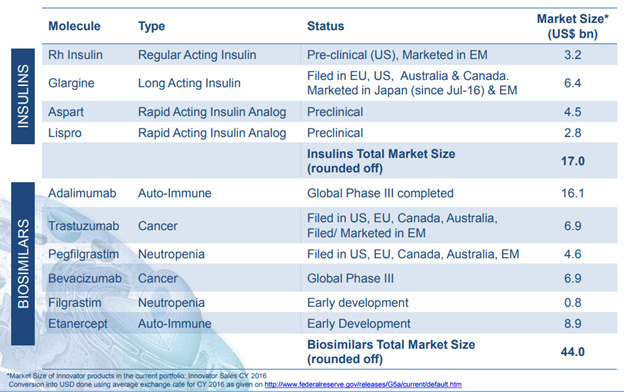

“Biocon possesses one of the largest global biosimilars portfolios, spanning human insulin/insulin analogues, monoclonal antibodies and other biologics with an addressable market size of ~USD 61 bn. Of the 10 disclosed molecules in our pipeline, nine molecules are being developed in partnership with Mylan, a global generics major. The strategic partnership between Biocon and Mylan represents Biocon’s strength in biologics development and manufacturing, as well as, Mylan’s regulatory and commercial strengths globally.”

Brief summary: The aim of this study is to demonstrate similar efficacy and safety between MYL-1501D( glargine) products produced from two manufacturing processes (Process V and Process VI) in combination with insulin lispro in patients with type 1 diabetes mellitus (T1DM).

Any comments on reason for this Phase 3 study ?

To tide over some patent issues with Sanofi

Additional data requested by FDA before accepting the glargine dossier.

As it is a US study, it seems unrelated to pending CHMP opinion.

(US dollar in crores) in rupees(1 dollar =63rs)(in crores)

(US dollar in crores) in rupees(1 dollar =63rs)(in crores)