Yes exactly something like that is what I assumed. So can it be so they want to do away with short term borrowings as they have enough share holder capital to use?

Even borrowing through commercial paper is classified as short term borrowings. Nothing to do with share holder capital. There are three major ways through which a company can fund its working capital requirements - internal accruals (cash profits generated during the year), bank and other borrowings and creditors.

1 Like

so which of these three does this 50 cr fall into ?

Bank and other borrowings.

Q1 results out, pat looks flat yoy… any comments ?

1 Like

Did anyone attend the AGM? If yes please do share notes !!

Notes from the AGM and talking to management after AGM:

Solid performance over last 3-4 years and big jump in sales from FY16(452cr) to FY17(600cr). Major factors for this performance and its sustainability:

The focus is on what the customer wants – purity, quality and timely delivery every single time apart from price. The chemical industry is very dynamic and one has to be on one’s toes and very close to what the customer wants consistently. The company has been able to do that on a consistent basis which resulted in increased orders. There are a few factors which will make the industry grow on a sustainable basis:

a) Volatility in China in terms of shutting down factories is real. This will lead to structural demand flowing down to India not just in terms of certain chemicals/agrochemicals but also because MNCs have genuinely begun to scout for a viable 2nd alternative. BRL has developed strong relationships with MNCs

b) ‘Make in India’ as well is real, in terms of various policy initiatives and import restrictions that can possibly come shortly

The confluence of China related pollution bans, the Make in India initiatives have given the company a large opportunity to tap. It’s up to the company how they execute and capture this opportunity. The company is very strong in its products and has the confidence of the customers due to its quality and timely delivery but the company needs to keep executing very well. The opportunity cannot help the company if it screw things up in terms of product quality or timely delivery

GST impact has been very good for the group, given a lot of spurious products (domestic as well as import) have reduced considerably

Sales breakup:

There seem to be 3 segments to our revenue – Domestic sales, Bharat Group Manufacturing, Off-patent manufacturing (domestic and exports within this contract/off-patent manufacturing and MNCs).

During FY17, the revenue growth was major driven by higher domestic sales.

Particulars FY11 FY12 FY13 FY14 FY15 FY16 FY17

Export sales 28.02 27.89 58.30 117.16 120.89 126.49 152.66 25%(growth in FY17)

Sales to group companies 18.87 18.05 25.73 64.45 125.39 126.65 164.84 25%(growth in fy17)

Domestic sales 45.03 94.26 101.53 176.90 189.00 198.97 294.69 50% (growth in fy17)

The big part of 50% growth in domestic sales has happened due to increased supply to MNCs. The supply to MNCs is both in the export and domestic market.

The go-to-market strategy is very clear for the company. The idea to continue to increase supply to MNCs and reduce supply to domestic customers. Of course, the company wants to continue to supply to Category A domestic customers (with requisite margins), but main focus area is to supply to MNCs. The reasons are 2 fold: i) better payment terms and ii) predictability and longevity of the molecule production (if not one, there will always be another).

The contract manufacturing is scaling up and currently accounts for 20-25% of our total revenues. These are usually long term contracts of 3-5 years atleast (and will continue until the company screws up) with raw material price fluctuations being passed on. These are big volume molecules with contract pricing (margins will vary – some molecules will be low margin while some others being high) and that’s part of the business.

Net-net from a revenue perspective, w Exports contributing 25% (~150 cr), Group companies contributing 25% (~150 cr), domestic MNC customers contributing 25% (~150 cr) and rest 25% catered to for domestic non-MNC customers (~150 cr).

Product and growth strategy, Molecule selection:

Meta Phenoxy Benzaldyhyde (top product- almost 80% market share in india and two competitors)

From a Meta Phenoxy Benzaldyhyde perspective, this is an old molecule with limited competition (apart from these players, there is also Meghmani who manufactures MPB). It has a unique customer (1 customer?) with a decent margin . The focus is to restrict production of this molecule to these levels (100 cr) as there are other more profitable molecules that can be manufactured instead of manufacturing this. The company plans to keep producing around these levels (100cr).

There is good potential in Lambda cylothrin as well.

Molecule selection is paramount (and is mostly guess work than a pure science – some times bets come off good, while other times, it doesn’t). The idea is to select niche molecules where there is limited competition and get out of that molecule (and replace it with another) whenever new competition comes in and margins trend down. Management tries to do a good job of this guesswork, but that’s what it is ultimately

The top products composition has not changed much from last year (MPB, Lambda cylathorin, Chlodina etc.). Competition exists in every thing, and the company tries to stay one step ahead of them. The company does not worry too much about market share calculations etc. The main focus is about utilizing capacity to the maximum and manufacture profitable niche molecules, than worry about market sizes and market shares.

The breakup is about 50% pesticides (insecticides and fungicides), 20% intermediates and 30% herbicides currently (as a proportion of revenue). This is expected to continue (as an aside point, Chinese are very strong in the herbicide market).

Company also started supplying Vet APIs to Zoetis. Vet APIs don’t require as much approvals, and the opportunity in this space is ‘good’.

MNC opportunites:’

Portion of turnover to MNC and long term contracts:

The proportion of MNCs in the domestic market is 25% and Exports is all MNCs. The strength of companies product and delivery (purity, quality, timely delivery) is of paramount importance to MNCs and the possibilities are endless (either in the domestic or export market) as long as the company don’t screw up and continue to maintain and keep up the product strength and timely delivery. It is upto the company as to how they exploit our association with MNCs

Competition in contract Manufacturing:

MNCs are very focused in terms of purity, product quality and timely delivery. As stated earlier, the limits are endless if you deliver these 3 things consistently and over a period of time. There is a large opportunity – contract manufacturing or otherwise – when you deliver these 3 things and our entire company’s focus is to continue to grow the share of MNCs. How far we can capture, how far we don’t screw up – only time will tell. There are other players as well, but as I said, the market is large, the dynamics of the market (china volatility and make in india) are changing in our favor – so, it’s up to us to capture this space.

New launches (by Bharat Insecticides) in partnership with Nissan:

(Read http://news.agropages.com/News/NewsDetail---22505.htm )

It’s a good opportunity and we will benefit because our group company’s has a tie up with Nissan. No comments on how much it will add to turnover etc.

Patent expiry opportunity in next 3 year:

There is a patent cliff opportunity (many molecules going off-patent in the next few years). The company is actively working on some of those molecules.

Export Market:

Brazil opportunity is very large and you will see some traction later half in the year for Brazil. The company is very positive on the Brazilian opportunity and hope to garner good revenues and margins from that market. The company did not give any target numbers etc. There are no plans of entry into US. Europe will be continue to be steady.

China CAC award:

(Read http://news.agropages.com/News/NewsDetail---22007.htm )

It’s a limited market in China for good quality products with high purity etc along with a good margin. China will not be a large market for BRL to supply there due to payment terms etc. The focus is on other large attractive markets in India and Brazil which serves the purposes of margins and revenues well.

CRAMS of patented molecules:

The company already contract manufacture off-patent molecules for a whole host of MNCs. The company will start manufacturing of patented molecules later half in the year and will try to scale this business up in the subsequent years. These will be new molecules for MNCs which they will be give us and not as replacement for another vendor.

Phasing out low margin products and getting into difficult + high margin molecule happening. What’s the overall trajectory in the product profile

The focus is to increase share of MNC molecules as part of our product profile and reduce domestic company molecules. The focus is to maintain gross margins and EBITDA margins (17-18%) in the future as well because of the strategy in the product and customer profile.

Margin profile/margin sustainability:

The effort is always to work at better margins, but the most important for the company, are payment terms. Post payment terms, the effort will be to utilize as much equipment as possible in the plant. The more equipment used, the more complex the molecule and therefore more margins. Given our focus and strategy, I think these margins should be sustainable, but as stated earlier, agrochem and chemical industry is very dynamic and it is difficult to predict much.

Technical capabilities for backward integration/manufacture more complex molecules like say N-3 / N-4:

Yes, it’s definitely possible. It takes time to build the capabilities, hire the right people and train them but can be done. We are doing 40 cr capex in backward integration, so that should tell you enough.

Capex plans:

a) 40 cr capex will be a brownfield expansion in the existing Dahej plant and civil works have already begun. The plant should be completed next year and should reach 100% capacity utilization within the following year post completion. This capex is exclusively to manufacture intermediates and really to backward integrate to i) avoid any China related import risk ii) better margins iii) currently about 55-60% of our RM is imported and we will reduce this dependency drastically due to the 40 cr capex. There is ready demand for the products and selling output from this capex is not a problem. This capex will add to the margins.

b) 200 cr capex will be a greenfield expansion and are scouting for land in the GIDC area. Although there is land space in the existing park, the company completely want to avoid the one-plant-one-area risk and hence would like to go for a greenfield expansion. This would be spread over 3-4 years and nothing immediate. There were no comments on ready customer demand or not for this capex. This capex would be manufacturing intermediates and technicals. There’s been a new rule stating that any factory in a designated chemical area with < 100 acre campus will not have to go for environmental clearance – the new capex will fall in this category, so the company expects that it will not face much delays from environmental clearance (but then again, things are dynamic).

c) 40 cr capex will be one-time. 200 cr capex will be done in phases. First, have to buy the land. Then will do 50 cr capex and fill customer demand and then do subsequent capex etc. The company is very conservative and would like to do incremental capex than do big capex big time and let the capacity sit idle.

d) 40 cr capex will be out of internal accruals. 200 cr capex is still under discussion – if we should do QIP, or fund gradually from internal accruals or take along bank debt. The board is still discussing it and has not made any decision on how we are going to fund it.

Others:

Bloated receivables in Sep qtr, bloated inventory in Mar qtr:

Receivables are not bloated as such. The company is very strict on payment terms, and there is no debtor greater than 6 month period. The company can be flexible on margins but not on the payment terms.

Inventory might be higher in March quarter as the company might have stocked more raw material in the face of China RM uncertainty. There is no drastic surprise as such. It’s business as usual.

GST impact for Bharat Insecticides and in turn Bharat Rasayan:

GST impact has been very positive for the entire group as such, given the spurious products (domestic and imports) have taken a large hit. It’s positive for the group, and very positive for BRL

Total capacity and utilization:

Utilization is around 90%, but utilization is a function of what products manufactured. Product mix can be changed at the same utilization to achieve higher revenues and margins.

Dividends and liquidity:

Liquidity in terms of stock split and bonus has been the complaint of many shareholders and will definitely looked into.

Dividends – no comment (but generally, not pro-dividends as there is debt, and we are going for capex. Possibility of a drastic increase in dividends is remote)

Disclosure: Invested: No transactions in last 30 days.

Thanks to a friend who helped in compiling the notes.

There may be error in compiling notes based on our interpretation of what was said during/after agm

39 Likes

Are the promoters of Karuturi Global related to this company anyway?

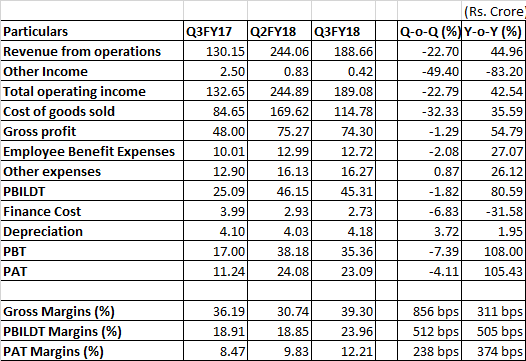

Bharat Rasayan came out with excellent set of nos during Q3FY18. At a time when other listed agrochemical companies have hardly grown their sales by single digit and their margins have been high by RM price increase, Rasayan came out with strong growth in sales of 45% on a y-o-y basis and further improved its gross as well as PBILDT margins on a q-o-q and y-o-y basis. Company keeps on surprising with its amazing consistency. The analysis of the nos is given below:

*Q3FY17 revenue have been adjusted by excise duty

6 Likes

Great set of numbers…Post GST, decrease in excise duty also played a major role

Post GST implementation, the GST directly gets deducted in revenue. There hasn’t been any reduction in excise duty (GST now) rate.

1 Like

1 Like

Care Rating release of June 2018, shows the Working Capital intensiveness of the business and other interesting information

http://www.careratings.com/upload/CompanyFiles/PR/Bharat%20Rasayan%20Limited-06-19-2018.pdf

1 Like

I have recently started tracking this company. Any idea from experts what will be impact of crude oil prices both on RM and margins. If crude oil prices goes up I believe revenue has gone down in the past even after volume growth, however margins can be maintained. Considering shift in company strategy to MNC supplies might have reduced impact of oil on business.

Bharat Rasayan AGM Notes - September, 2018 (prepared by @ananth and I)

• Top 10 products of BRL constitute 70% of sales in FY17 (vs 77% in FY16).

• Top 5 customers of BRL constitute Rs.223 crore in FY18 (35% of sales), Rs.118 crore in FY17 (25% of sales) and Rs.74 crore in FY16 (22% of sales)

• Out of BRL’s total revenue of Rs.788 crore, Rs.142 crore went to group companies in FY18 (vs Rs.140 crore in FY17)

• BRL export sales was 25% of total sales in FY17 (vs 28% in FY16)

• BRL imports was 50% of total RM in FY17 (vs 54% in FY16)

• Updates on China: Chinese chemical companies are facing environmental issues. However, the impact has been on product to product basis. Some of the products are seeing extreme shortage while some are not facing much issue. Earlier China used to supply 90% of the agro-chemical requirements of the world while India contributed to 10%. The issues in China are expected to change this ratio to 66.67% in favour of China and 33.33% in favour of India. 2 – 3 of our products are also facing higher price increases due to China issue. Even if the China comes back but due to higher employee and environmental costs, the cost for Chinese companies will increase. However, we expect this situation to continue for 3-4 years. This is a golden period for Indian Chemical companies.

• Monsoon and pest infestation update for this year: Most of the formulators were very bullish till August of this season. However post August things have changed. We are hearing reports that pest attacks were less and formulators are not so much bullish now. This year rainfall has been good and although the pest infestation is low but higher rainfall is expected to improve the liquidity of the farmers which in turn will also help in improving the debtor realisation of the formulation players. The formulation players have been able to pass on the price increase in technical to farmers.

• During FY18, we had volume growth of 10 – 12% while remaining growth in revenue was on account of increase in prices and change in product mix.

• One of our major product meta phenoxy benzaldihyde (MPB; where Bharat Rasayan has more than 50% market share in India) has remained stagnant at around 100 crore sales for past three years. Our sales were impacted due to imposing of anti dumping duty (ADD) by China for this product (the company was supplying to China). However, we have entered into a long term contract of 5 years for supply of this product with one of the largest agrochemical company in the world based out of Germany for supply of around Rs.60 – 80 crore (5 year contract, on quarterly pricing). Our sales for this product is Rs.200 crore (understanding: Rs.100 crore for sales, Rs.100 crore internal consumption).

• Updates on Japanese Innovator molecule contracts: We have been talking to Japanese customer for a long time and as you know it is difficult to get contracts from these customers. However, once they start give you contract, they stay with you for a long term and unless you screw up, they don’t terminate the contract. We have ties with three of the large Japanese agrochemical cos for patented products and supplies will start in near term. We do (n-1) patented contract manufacturing for these players. Currently, we have 5% of contribution of products for innovator molecules (we supply some intermediates) and expect this to increase to 20 – 25% over the medium term. This contracts are for term of 5 – 10 years. We want to win trust of this companies and our pricing is such that it creates win-win situation for both us and MNC companies.

• Product basket and customers: We have 23 molecules under manufacturing and supply to 75 – 100 customers in domestic markets and 50 – 60 customers for exports. The German MNC is one of our large customers with sales of around Rs.100 crore. We always focus that the utilisation of our plant should be 95 – 100%. We continuously focus on higher realisation and higher margin products and replace low margin products with them.

• Thought process behind choosing a particular molecule to manufacture: For generic molecules we normally target molecules which are getting off patented and where we have chemistry strength. We are normally the 2nd or 3rd player to get into the market for the product. We also try to be backward integrated for the product.

• Focus on MNC and top Indian companies: Over the past few years, we have been trying to continuously focus more on MNC and top Indian agrochemical companies. Currently, we only supply to top A and B rung agrochemical companies and have replaced top C and D rung companies over the years. We supply to most of the top MNCs and Indian agrochemical companies. In local companies, we supply to most of the large Indian companies. We believe in building long term relationship with clients. If there is extensive shortage of some of the products we manufacture in the market and if we have long term relationship/contract with the client, we don’t try to squeeze our customers to the maximum and give them some discount to the market price.

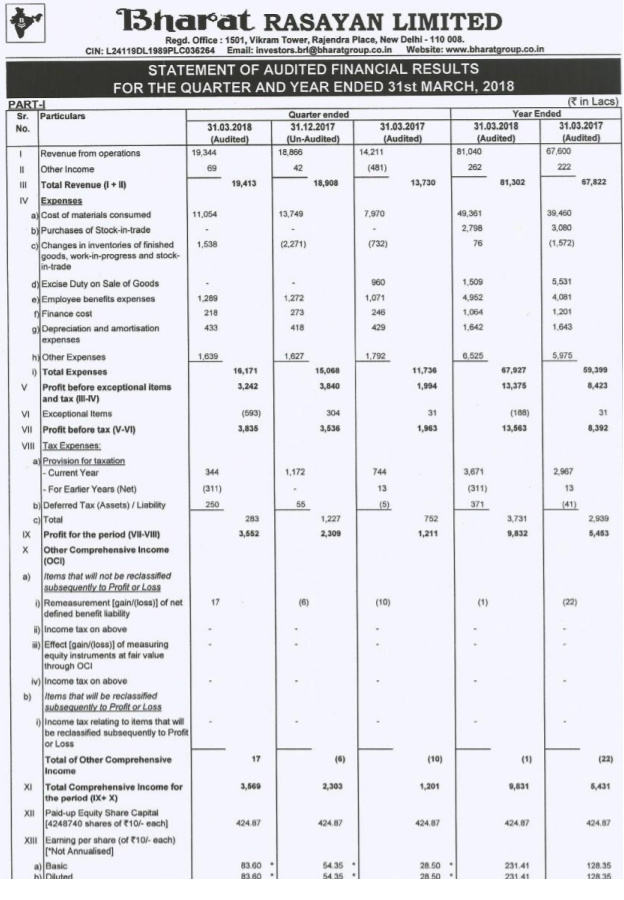

• Increasing working capital intensity especially debtors: There are three reasons which have led to increase in debtors: 1. The whole industry has now started extending credit period of 120 days instead of 90 days. 2. Earlier we used to give cash discount to our customers (1-1.25%) but have now stopped cash discounts given we get 8% finance from banks (vs 12% on cash discounts). 3. We buy most of our raw material on cash. We are amongst the lowest cost procurers of our raw materials in the industry. You will have to understand that China gives a credit period of 180 days and that too without any interest. Furthermore, I can give assurance that there will hardly be any bad debts in these receivables as these are all repute customers including MNCs. Currently, our debtors are around Rs.350 crore (Rs.247 crore of debtors as on September 30, 2017). The working capital intensity is more in the first half of every year as 60% of our sales happen during H1. Currently, we have bank debt of Rs.150 crore.

• Expansion plans: We are expanding capacities for existing as well as new products and backward integrating into manufacturing of intermediates which is a part of brown field capex at Dahej. The expansion at Dahej will come in two phases – 1st phase to come up in June, 2019 and 2nd phase to come up in December, 2019. Our focus will also be introduction of new products post commencement from this expansion. Our target has always been bottom line.We have two expansion plans currently:

o Brownfield expansion at Dahej: We are expanding capacities of technical and intermediates and backward integrating at our existing facility at Dahej. The total cost of capex will be Rs.100 crore and will be funded through internal accruals. The expansion will come in two phases: Phase 1 to be completed by June, 2019 and Phase 2 to be completed by December, 2019. The backward integration will lead to reduction in our costs. Backward integration will reduce our costs by a minimum 15-20%

o Green field expansion at Saika, Gujarat: We want to reduce our dependency on a Dahej plant and that is why we have purchase land at Saykha, Gujarat around 25 kms away from our existing plant. The environmental approval for the plant will be filed shortly. The total cost of capex will be Rs.200 crore and the capex will come up in phases. The expansion will be for expanding existing products, manufacturing new products as well as for manufacturing intermediates (for backward integration as well as for selling in the market). The company is yet to decide the funding of the same. They are open to various options like strategic alliance including foreign JV, PE investor, raising money from the markets as well as debt. They can even enter into technological tie up with other MNC companies.

Post expansion, the company’s dependence on China will at least reduce by 50%. The management for the first time stated that post completion of both the expansions and ramp up of both the facilities, they plan to reach turnover of Rs.1500 crore by FY22/FY23. (My inputs: given their past track record, the projections are conservative).

• Foray into Brazil markets: We have filed 5 – 7 products in Brazil market (the cost of each filing is Rs.5 – 7 crore). The approval product for these market is long. We expect to get approval of atleast one of the product this year. Brazil is a focus market for us as it’s the largest agrochemical market in the world and in the medium term we hope to derive 10 – 15% revenue from it. Despite focussing on Brazil, there shouldn’t be any negative impact on our working capital.

• $ and crude are 2 variables which affect us but given increasing change in composition of revenues (more MNC and less spot basis), we expect all of this to be passed on to the customers.

• Long term break up of revenues: We expect 40% of revenue contribution from MNCs through strategic alliances/long term contracts (both domestic and exports) and exports and domestic market to contribute 30% each. Over the medium term, we expect patented products to contribute 15 – 20% to our revenue from existing 5% (we currently supply some intermediates for patented products).

• Updates on veterinary APIs: Not much change compared to last year (they supply to Zoetis).

• Reasons for our success? Our manpower and chemistry skills is a key contributor for our success. Customers including MNC companies come to us as we have built trust with them to delivering quality products within the given timelines.

Has complacency set in top management and team post success we have seen in recent years. There is no complacency set in the promoters as well as employees. RP Gupta said that the promoters are involved in the company 24X7. He still knows even the number of every machine installed in both the plants. If the top management is motivated, the employees become motivated too.

• Key Risks: Safety hazard is the major risk in our industry. We are very much focussed on that and take measures to avoid any mishaps at the factory.

• You cannot look at our company from the topline perspective. We can make strategic product shifts based on the demand from our customers and margins available. We can change our product mix based on market conditions and the needs of our customers. We are a bottomline focused company

• There is a golden opportunity for multiple Indian players who have Size, Trust and Ethics to partner with MNC players as MNC players are now desperate to strike partnerships as a second source here. If Govt. doesn’t play spoilsport, then we will have very very good days and years ahead of us – not just for Bharat Rasayan but the entire agrochemical manufacturers.

(Disclosure: Invested)

36 Likes

Investors should be cautious and seriously contemplate booking profits.

Bharat Rasayan has been in ASM segment for some time. There are a bunch of corporate bodies who own more than 12% of shares.

Rithesh projects private limited is one of the large share holders of Bharat Rasayan. There are atleast three other companies associated with Rithesh and who hold shares in Bharat Rasayan.

Rithesh has been called an ‘exit provider’ by SEBI and had been investigated for manipulating share prices of other companies.

http://www.watchoutinvestors.com/PRESS_RELEASE/SEBI/1472218822636.pdf

https://www.sebi.gov.in/sebi_data/attachdocs/1418994552337.pdf

4 Likes

I have been following the company for the past many years. I have met the promoters twice at the AGM and they value corporate governance very highly. Have even seen their Dahej plant from outside. Their quality is appreciated by not just customers but even competitors.

About shares being in ASM - there are lot of companies which are doing well and run by able management whose shares have been put in ASM category. Dont think its an issue.

On Ritesh Securities being a shareholder of the company, its been there for more than 3 years now. Promoters are not looking to sell out their shares in the company and looking for an ‘exit’.

6 Likes