Bharat Rasayan looks very interesting on the surface so I wanted to take a deeper look. The return ratios are spectacular for the sector the company is operating in, the promoter holding is around 75% and D/E is reasonable and P/E as well looks fair. All good so far. The next step was to look at financials, the top and bottomline have grown at a very good pace - topline around 15x and bottomline around 100x in 10 years. Very good again, am certain it looks good on a CAGR basis as well. Perhaps too good, perhaps the best, compared to peers like PI Industries, Dhanuka Agritech, Insecticides India, Rallis etc. which piqued my interest further and also kindled my suspicions on the possibility of cooked numbers.

So, to verify I set about the usual process of checking cash flow, receivables, cash conversion, dividend payout etc and this is what I found.

- 10 Yr FCF is -25 Cr. So in the long run, this company is not generating FCF. However in the last 5 years, there is positive FCF.

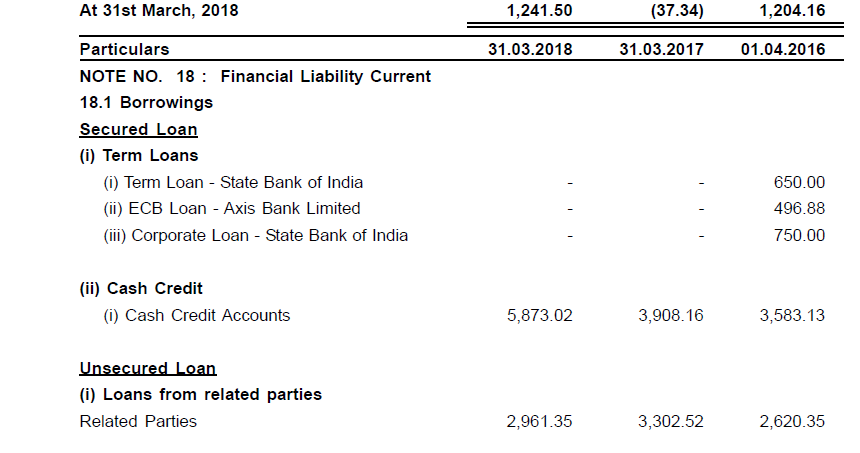

- Receivables are high at 345 Cr. Receivable days are following an uncomfortable trajectory from 50 days 5 years back to 77 days at present. At the same time Payable days have also deteriorated from 32 days to 15 days while inventory days are improving and overall cash conversion cycle is pretty poor, from 66 days to 102 days in the last 5 years.

-

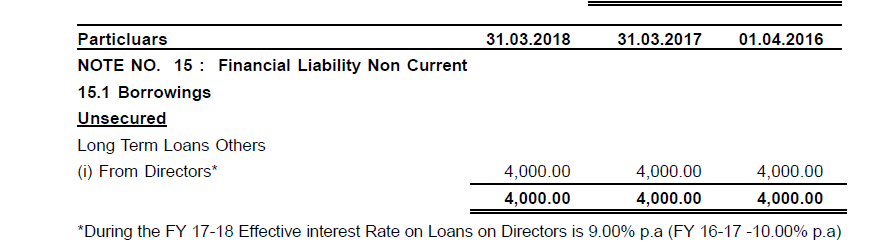

The D/E looks to be improving in the above but the E part of D/E is growing mostly through receivables, so I am not sure how we should perceive that.

-

This company has phenomenal return ratios so I expected the company to be throwing out cash but this has not been the case when looking at dividends in the last 5 years. Dividend payout was a abysmal 2% between FY14 - FY16 and 0% in FY17 and FY18. Thats not a good sign

I was a bit ambivalent about the genuineness of the numbers because it was outperforming peers but the same was not coming out as dividend but being locked up in receivables, though the incremental PAT growth corresponds to the reinvestment (incremental capital employed) and reported return ratios.

I could have ended it there but wanted to look at a SHP analysis of the company.

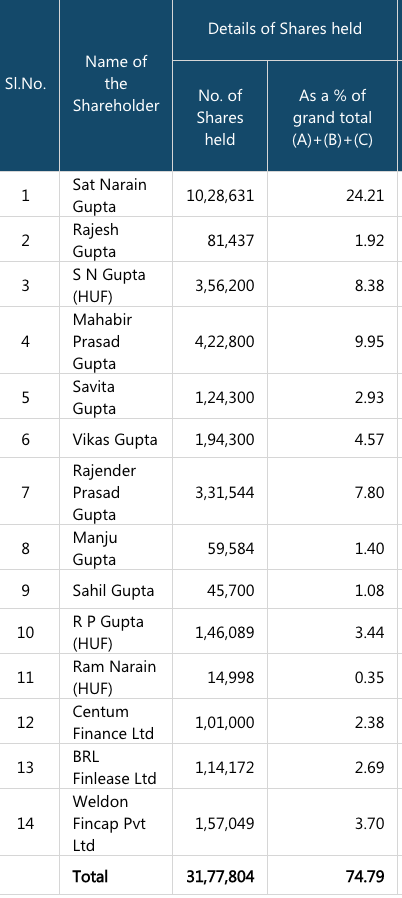

These are the promoters holding the 75%.

Unfortunately, this company has not been dispatching SHP to BSE since Dec '15, so I couldn’t take the shortcut of analysing via phreakonomics.in. I had to do this manually by looking at the SHP on NSE (its a pain). Even there its not showing up when I want to look at recent public holders so I got the xml which was there that held the SHP and figured out who held how much from there.

The majority holders are

Ambaa Securities Pvt Limited - 4.94%

Ritesh Stock Broking Pvt Limited - 4.70%

Shiv Shankar Securities Pvt Limited - 1.92%

That did not give me a good feeling. Why are stock broking/trading firms holding 12% of the company? So overall it looks like hardly 10% is the floating stock in this company.

Even among the promoter holding, these three firms got my attention

Centum Finance - 2.38%

BRL Finlease - 2.69%

Weldon Fincap Pvt. Ltd - 3.70%

Long story short, Ravi Kumar Newatia is a director in Ambaa, Ritesh Stock Broking and Shiv Shankar and this Ravi Kumar Newatia looks to have been involved in money laundering/tax evasion in Mishka Trading & Finance - https://www.sebi.gov.in/sebi_data/attachdocs/1429273159211.pdf

This Ravi Kumar Newatia is also a director in Dynamic Portfolio Management which was also involved in the above scam of laundering/tax evasion and interestingly, this company shares address with Weldon Fincap which links this shady chap directly with the promoters.

Also, this Rajesh Gupta who is a promoter in Bharat Rasayan holds stake in Dynamic Portfolio Management Services https://phreakonomics.in/shareholding/index/DYNAMICP which again places strong links between promoters here and big holders classified as public to the money laundering/tax evasion unearthed by SEBI in Mishka. I think this is the same Rajesh Gupta who is the promoter of Bharat Rasayan because holdings of Rajesh Gupta have an overlap with the holdings of

Weldon Fincap Pvt Ltd (Some trading companies, gems and jewellery companies) which is also a promoter entity in Bharat Rasayan. Again this is a mess of cross-holdings similar to the one I encountered in Byke. I was simply following a hunch looking at the numbers and price-action and to me few things here look very questionble. Your mileage may vary.