FACT (like the infy board letter :-)):

a. In 2015-17 the capacity was expanded from 51 KTPA to 80 KTPA in 2 phases. The gross block increased by 38 crores in 2016 and 17 crores in 2017. The cost of the expansion (38+17)/(80-51) = 1.9 crores per KTPA. I will assume 2 crore per KTPA for future expansion considering inflation.

b. 2017 sales was 704 crores, PAT 35 crores, giving an EPS of 2.10. PAT Margin is 5%. Gross Margin is 22% (Material Costs - 550 crores).

c. Depreciation was at 5.4 crores (3% on gross block) and working capital is 10% on sales (70 crores on sales of 704 crores).

d. Capacity utilisation in 2016-17 was 64.31% or 51 KTPA. Revenue per KT is (704 / 51) = 13.80 crores.

Management Expectation:

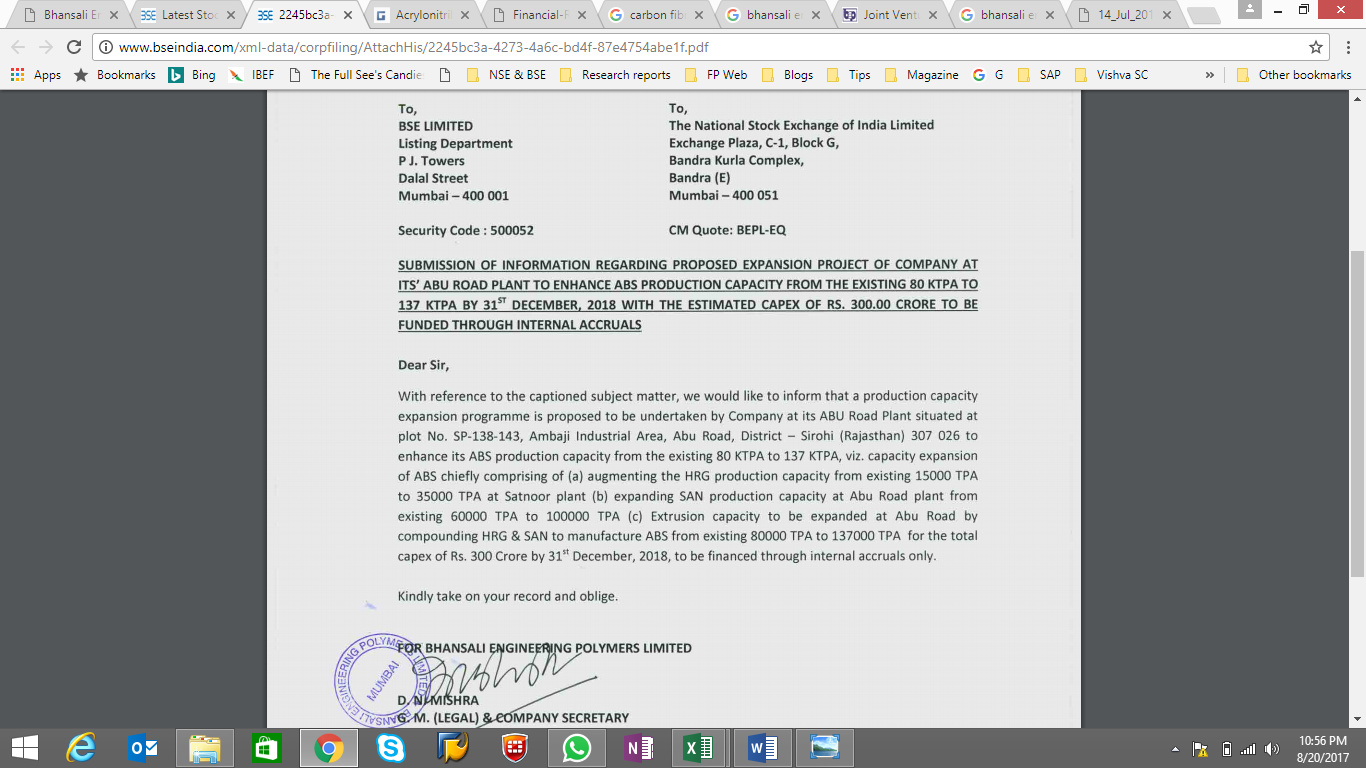

a. To ramp up ABS capacity from 80 KTPA to 137 KTPA by Dec 2018 entirely out of internal accruals.

b. Demand expected to go up at 15% CAGR for a decade. 2016-17 demand is 275 KTPA, Ineos and Bhansali cater to 160 KTPA. This means on a 5 year period average additional demand will be 54 KTPA, not to mention the current demand met by imports of 115 KTPA.

c. To achieve 90% capacity utilisation beginning 17-18 to generate adequate surplus to internally fund future expansion projecs without need for additional funding. It hopes to achieve 72 KTPA utilisation by Mar 2018.

d. To establish a port based greenfield project of 200 KTPA capacity by 2022. This will be through a JV with Nippon A&L Japan.

My Analysis

a. The capacity addition from 80 to 137 KTPA requires 114 crores of fixed capital 2 * (137 - 80) and 80 crores of working capital. Working for 80 crores is [ { (72 - 51) + (137 - 80) * 64.31% } * 13.80 ] * 10%. I am assuming the 80 KTPA works at 90% capacity and the remaining 57 KTPA works at 64.31% capacity.

The incremental profits after tax that will get generated in FY 18 is ( [72 - 51] * 13.80 * 22% * 70%) = 44 crores. In FY 19, it will be 44 + (137 - 80) * 64.31% * 5% = 70 crores.

Against the capital requirement of 114 + 80 = 194 crores, the company will be able to generate (40+44) + (40+70) = 194 crores. Phew! The management will have just about enough funds to fund the growth using accruals. This is assuming their expectation fructifies. They do have to make sure that they keep a close watch on their working capital.

b. Now the 200 KTPA capacity addition will need much more than 700 crores (Fixed + Working Capital) in my opinion. With a run rate of 110 crores cash generation post FY 19, the company will need atleast 400-500 crores to be able to build this additional capacity. Will Nippon Japan fund this?

c. In the short term, there are quite positive indications that the EPS can grow to 6 (105/16.7) odd by end of the FY 2019. The long term story is just playing itself out and we have to wait and watch.