ICICI Direct weekly call on BEPL… predicts 92 and higher by the end of the week. Read the call here.

http://content.icicidirect.com/mailimages/weeklycall.pdf

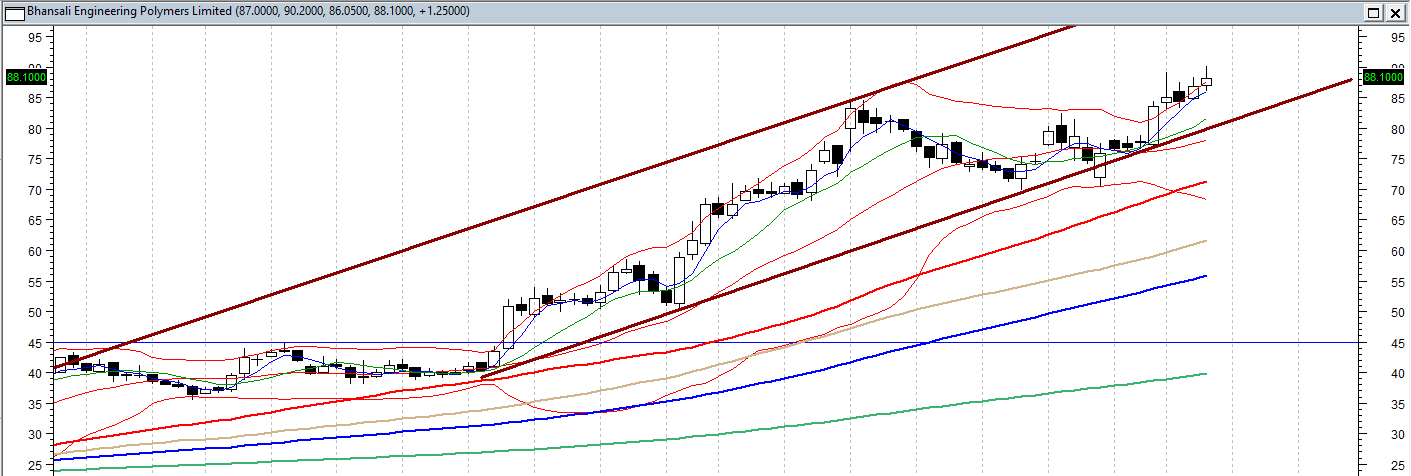

A rising channel

For several months the prices are moving in a rising channel. During August they have again taken support at the lower support line and moved up smartly. The big question is: whether they will move all the way to the upper resistance band? If that happens, the current upmove should take BEPL at least to 110-120 levels before correction brings the prices down. Longer it takes to reach the resistance level, more will be the chances that the prices will sustain at the higher levels. I will feel more comfort, if BPEL remains in 85-99 range during next 10 days.

Disclosure - heavy investment done at 25 level.

According to a news today, seven shareholders, having about 2.5% holding, have been shifted from promoters to public category. Will some experienced member explain the significance of this move for small shareholders and the company?

This news has been given in NSE in 23rd August. This is just 2.63% . Names of Father, Son duo are not there. We need to make comments after verifying all the data. Yes Names of People, ending with Patel is there.

Seems across the board phenomenon in many listed companies. More likely seems like compliance to some new SEBI guidelines or possibly for tax purpose. Since it is across the board in so many listed companies i would ignore such changes impacting business

Its simple .Please don’t think too much.

Any family member or any ane close connected who are not involved in day to day business of the company and have no say would prefer to be in Non promoter category enjoying the benefits of non disclosure on buy and sell.

Following article gives a good hint about why it must have happened for BEPL: https://www.google.co.in/amp/m.economictimes.com/markets/stocks/news/no-legal-hassles-please-some-promoters-keen-to-be-known-as-non-promoters/amp_articleshow/55197522.cms.

It mentions: “In the last few months, many promoters who were not involved in the day-to-day control of the affairs or decision making of the company directly or indirectly or not holding any special rights, have chosen to reclassify as public shareholders to mainly to be eligible for exemption from the various obligations.”

4 Likes

Hi Madhavi, all the expectations of the movement similar to first quarter seems to not be happening. Do you see any threat because of this news? May be the promoters are silently selling after being classified as public and no one really knows as they are no more promoters. It would have been good if the current promoters at least have purchased the equivalent amount of shares that they classified as public. Neither seems to be happening. Where do you see BEPL going forward? Please let us know your thoughts.

Dear @Parthasarathi, Just going by this news, I am not able to conclude that, there is any threat. I can base my judgement only on information available on public media. Unfortunately, I do not see any other fresh news on Bhansali for the past few weeks, other than the above one. In fact, I do not find any weakness on the stock, as it has still risen by 10% in the past two weeks. I assume that, all the fundamentals and expansion stories also remain intact, as we have not seen any fresh news mentioning that, those have changed. True that, we have not seen the euphoria that we saw during the last quarter. I feel that, promoter cannot keep on buying the stock, as he also needs money to buy. I feel that (purely my assumption), some of the money that should have come onto this stock must have got redirected to other similar stocks (though their end products are different) like Himadri, Phillips Carbon, Graphite India, HEG etc. during this quarter.

1 Like

Thanks for the reply. I am holding for now but please do let us know if you find anything new on this. Bhan also needs your hand holding like Arihant:slight_smile:

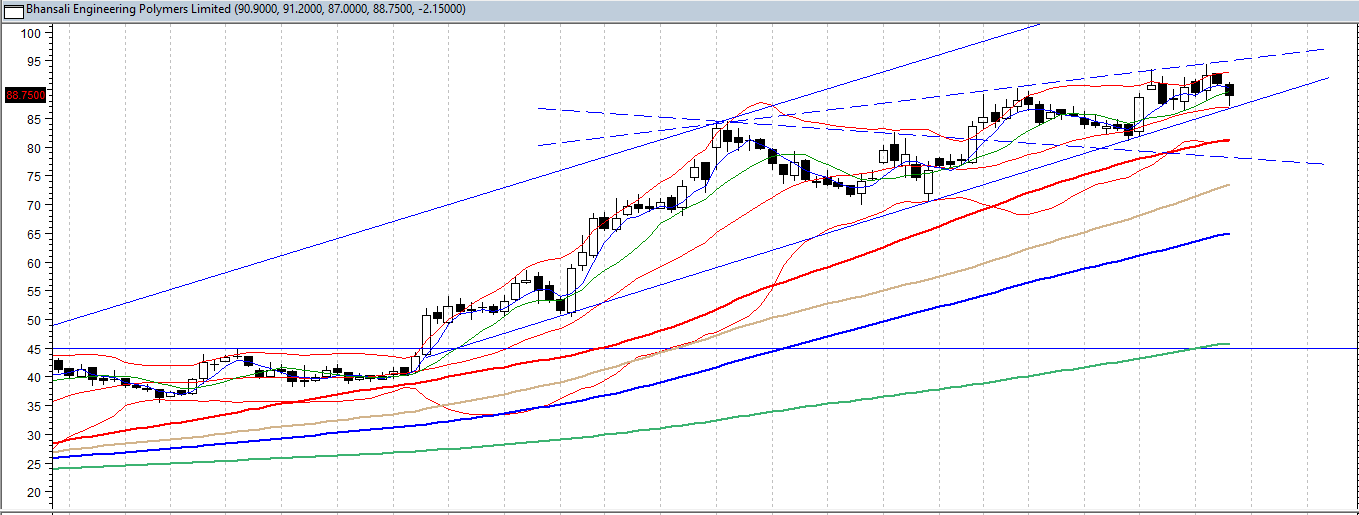

Today and the next week crucial…

Dear @ madhavikkutti and Parthasarathi! Looking at the chart, it can be inferred that the next few days are crucial for the stock. It is moving in a narrowing triangle formation, strictly paying attention to the support and resistance lines. But near the apex the triangle is becoming too narrow, and the prices have to make a decision. Which direction they take can be anybody’s guess, but a sharp correction or big breakout is imminent. It may be a false corrective move first, followed by breakout, but the reverse is less likely.

3 Likes

In my view, the company is announcing the results very early gives public the sign that it would be bumper!

Also, after looking the delivery volume on NSE, it gives me feeling that some funds have made the entry.

In my view, at 104, BEPL is trading at rich valuations. It is more than 40PE. How do you guys feel it will move going forward?

Anyways, have a look at this-https://asia.nikkei.com/Markets/Commodities/ABS-prices-track-higher-on-Chinese-auto-buying

Disclosure-Exited the BEPL above 100.

2 Likes

Bhansali is on the cusp of pretty good results. LT investors should hold on. I am more interested to know how their proposed expansion plan from 80 KTPA to 130 KTPA going on.

With good Auto nos coming and based on this ABS international price hike + Rupee depreciation , BEPL is expected to do better

They even say they want to fund the 130 to 200 ktpa expansion (in that mysterious port city) through internal accruals. The funding for current expansion will give us a clue of how good they are in adhering to statements

ABS price rise is actually positive for Bhansali—till the rise of the finished product remains more than the rise in the raw material prices. This appears to be the current scenario.

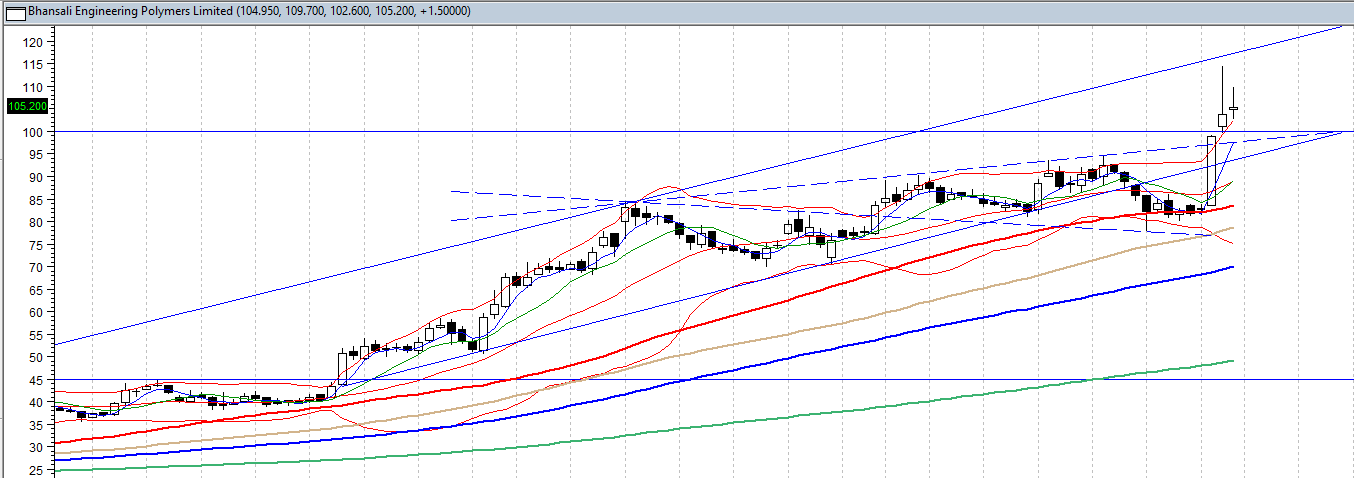

In the next week, if the share price holds above the upper dashed line, there is little cause of concern. If share price moves above the upper continuous line, there will be a bull move, which can take BEPL to 150 and above. In the longer term for the story to continue the prices must remain above the lower continuous line that will shortly cross the century mark. Please ignore the horizontal line at 100.

1 Like

Bhansali only needs good execution

Analysis: Asia ABS, PP block copolymer get support from firm Chinese auto demand

Singapore (Platts)–3 Oct 2017 1210 am EDT/410 GMT

The acrylonitrile-butadiene-styrene margin in Asia is holding near a four-year high despite the fall in prices last week, after riding on bullish Chinese automobile demand throughout the third quarter.

Asian spot prices for ABS, a polymer used in the manufacturing of automobiles and consumer electronics, fell below $2,000/mt CFR China last week for the first time since early September, S&P Global Platts data showed.

ABS was assessed at $1,980/mt CFR China Friday, down $60/mt week on week on retreating feedstock styrene monomer and butadiene prices.

ABS margins averaged at $290.82/mt in Q3, compared to an average of $164.36/mt in Q2, and just $5.02/mt in Q3 last year, Platts data showed.

This is in stark contrast to 2016, when sluggish downstream demand pushed ABS prices to below $1,500/mt until November, resulting in negative margins for non-integrated ABS producers for pro-longed periods.

AUTOMOBILE SALES SHOW NO SIGN OF SLOWING DOWN

A large contributing factor is the increase in automobile sales in Asia, owing to robust demand from China – the world’s largest automobile market. China currently accounts for around half of global demand for ABS, according to market participants.

China’s automobile demand is expected to rise 6% year on year from 2016, according to industry estimates.

China’s ABS imports rose 4.2% month on month for August at 167,068 mt. This also represents a 14% rise year on year, reflecting the strong demand for ABS and its downstream sectors in Q3.

According to the latest statistics released by the China Association of Automobile Manufacturers, automobile sales were up 10.9% month on month to 2,186,000 units in August. This is a third consecutive month of growth and also represents a 5.3% increase in sales compared to the same period last year.

Production figures were equally positive, up 1.6% month on month to reach 2,093,000 units in August. Year-on-year, this figure represents a 4.8% increase.

Another contributing factor is the pickup in seasonal plastics demand ahead of the week-long National Day holidays in China that started October 1. During this week, downstream users of ABS typically observe a large spike in both consumer electronics and automobile sales.

This increase in manufacturing activity ahead of the National Day holidays was evident in China’s latest Purchasing Managers’ Index for September, which was up 0.7 points from August to 52.4 – a year-to-date high.

PP BLOCK COPOLYMER HITS TWO-YEAR HIGH IN SEPTEMBER

The same trend could also be observed in the polypropylene market, especially block copolymers which are being used increasingly by Chinese manufacturers in automobile applications.

China’s PP block copolymer import prices surged to two-year highs early September, as downstream demand from the automobile sector rose, according to industry sources.

The Platts CFR Far East Asia PP block copolymer assessment had risen 5% since the beginning of the year to $1,180/mt on September 6, 2017 – a price level not seen since July 15, 2015 – with the industry expecting relatively firm demand in Q4. But since then the price has edged down to $1,150/mt on September 27, down $5/mt week on week ahead of the Chinese holidays.

PP copolymer imports into China are also on track to rise 15% to about 300,000 mt in Q3, compared with Q2, according to China customs statistics. Block copolymer, also known as impact copolymer, is used increasingly by the automobile industry to substitute metal components to build lighter cars and promote fuel efficiency – an industry trend known as “lightweighting.”

An average car used about 150 kg of plastics and polymer composites in 2014, according to the American Chemistry Council. This amount is expected to double by 2020, making it one of the most important growth sectors for PP producers, industry sources said.

Q4 ABS PRICES TO REMAIN SUPPORTED ON SUPPLY TIGHTNESS

Looking ahead to Q4, with no new ABS plants scheduled to begin production later this year, demand is expected to outstrip supply, sources said.

“Despite a fall in both feedstock butadiene and styrene monomers prices last week, the tightness in the Asian ABS market will likely continue to provide support to ABS prices in the short term,” an ABS producer said.

Feedstock butadiene was assessed at $1,450/mt CFR China on September 29, down $150/mt week on week, while SM fell $95.50/mt over the same period to $1,263.50 CFR China. This represents a $79.80/mt or 7.6% fall in feedstock costs week on week for non-integrated ABS producers, which will likely exert some pressure on producers to adjust offer prices lower when the market reopens after the National Day holidays, next week.

Meanwhile, European ABS prices in October are expected to be steady, tracking a stable outlook on costs, Platts reported earlier. The European ABS spot price was last assessed at Eur1,820/mt ($2,180/mt) FD NWE Wednesday, up Eur90/mt over the month.

With the CFR China ABS spot price falling below $2,000/mt last week, the import arbitrage from Asia into Europe may re-open in October, based on indicative freight costs of around $100/mt between the Far East Asia and Europe and additional inland freight costs of around Eur20-30/mt

6 Likes

Very relevant news article. Excellent eye for detail!!

Do you know the correlation between prices that BEPL (or any other indian market players) fetch and the prices of ABS in Europe / China… Do they track closely or are BEPL’s sales at contracted price with no mark-up for rise in spot?

Just trying to understand whether margins and bottom line of BEPL tracks closely to global prices or it follows its own course?

Your reply will be appreciated.

No idea. But what I gather from earlier notes that BEPL, 50% production long term contract and rest 50% Market Linked