Not sure if my analysis is correct but promoters buying from market and not releasing pledged shares may be indication that they are seeing better future for the stock so they are buying more shares rather than using the same money to release the pledged shares. If price is not going to go down then they may not worry about pledged shares and may use that money to buy more and may release pledged shares later.

3 Likes

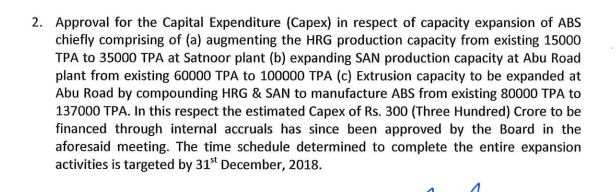

the company has virtually guided a volume growth of ~40%. Thats a very very ambitious guidance! Also, capacity will go up to 137 ktpa by Dec 2018.

I see two capacities mentioned in the AR - 80 to 200 with the new port based plant and 80 to 137 to 200. Which is the correct version?

The main customers for BEPS are auto and consumer durables. Which is the split for BEPS? Looking for sector dependence as well as customer dependence - is customer-wise revenue data available? Is there room to acquire newer auto customers, for example? Or are they already present at all major OEMs and need to increase share of business to grow?

Hi Rajeev, the JV numbers seem good. Thoughts?

What make you feel that numbers are good?

As per AOC-1, JV has total loss of around 35Lakhs

Notes from 2017 AR:

-

As on March 2017, the capacity stands at 80 KTPA. Exploitation in the year 2016-17 has been to the extent of 64.31% only. Company is confident that by end of the current fiscal 2018, it will produce and sell 72 KTPA (90% utilisation) i.e. optimal capacity utilization. This works out to approx. 40% volume growth.

-

Company is creating additional capacity at Abu Road to take total capacity from 80 KTPA to 137 KTPA by 31st December, 2018. Requisites steps have been initiated and the entire expansion programme will be financed through internal accruals.

-

Mega expansion is planned at a port based in Gujarat of minimum 200 KTPA. It would take 5 years to commence its operations (31st March, 2022). Work on land acquisition is progressing rapidly. Captive power plant is also planned which shall keep costs under control.

-

Mr. Jayesh Bhansali was paid a fixed remuneration of Rs.60 Lacs p.a. in FY 2017. From FY 2018 onwards, in addition to fixed, he will be paid Commission, both together shall not exceed 5% of Net Profit of the Company. Mr. B.M. Bhansali is already taking fixed remuneration of Rs. 60 Lacs and commission upto 5% of Net Profit. This means that remuneration from FY 2018 onwards will be maximum permissible.

-

The company has proposed a special resolution to approve borrowing of Rs.1,000 crores by the board from time to time as they may think fit and suitable. The company may be planning to take debt for their mega expansion in Gujarat.

-

The overall demand of ABS has substantially outstripped the present supply from the domestic manufacturers which are only two, BEPL and an MNC competitor (INEOS Styrolution India Ltd) whose respective capacities are identical and aggregates to around 160 KTPA against the current consumption level hovering around 275 KTPA in F.Y. 2016-17, this is likely to continue to grow at the rate of 15% CAGR for at least a decade ahead.

-

It is estimated that Internationally overall ABS Global capacity utilization is around 70% and therefore big capacity players find it attractive to supply in the deficit zone mainly India and China. However, despite the market opportunity, the global players find it difficult to meet demand of the Indian market as quantity wise it is not attractive to cater to each market segment on account of variety of colours and performance specification.

-

Global players establish and expand their capacity in China as China globally exports the products manufactured out of ABS resins. So China is exports driven whereas India is domestic market demand driven and therefore it may not make sense for global player to set up manufacturing here in India.

Principal Threat:

Basic raw materials of more than 85% viz. Styrene and Acrylonitrile monomers along with several Additives & Pigments are imported. Fluctuation of prices and availability in the International market could be principal threat. Price of monomers is volatile on account of availability and price of the petroleum and petrochemical building- block materials viz. crude oil, ethylene, naphtha, benzene, Propylene-oxide, etc. Import dependency also leads to risk of Foreign exchange fluctuation.

Project execution at Gujarat will remain a key factor. Looks like company is planning to take substantial debt for the same as they have proposed a special resolution to raise Rs.1,000 crores. This is way higher than the present Net worth of the company. Any untoward incident can lead to financial troubles should the company decide to take huge debt.

Hopefully there will be clarity on concern regarding pledged shares by management in AGM on 15th July, 2017.

6 Likes

I think the key takeaway here is that 40% revenue growth and possibility of margin expansion which is where the joint venture with Nippon will play out should give a bottom line growth of 50% for the next 2 -3 years.

Mkt will closely watch the commitment being given in the AR. If it happens, will reward them really well. Execution is key now.

Encouraging part is Remuneration is low and linked to performance

I will actively looking towards, AGM responses. Kindly share the details of responses, whoever is attending in Mumbai

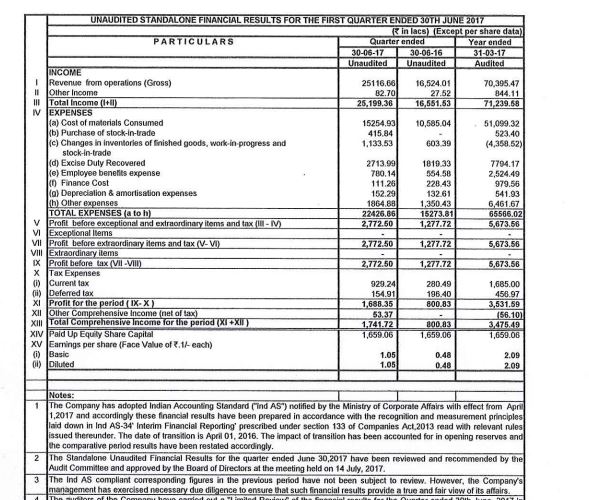

My bad, saw consolidated results on the next page and messed up the numbers

Management Meet Notes by a friend.

Outlook:

Out of total demand of 350000 ton, more than 60% of demand is met by Ineos (capacity ~140 KTPA) & Bhansali (capacity 80 KTPA-FY17, 137 KTPA FY18) imports are largely concentrated on basic ABS polymer (white grade) which are low margin and basic grade where BEPL is not focusing on. Colour grade cum resistance are higher margin and involves R&D, customer approval etc where BEPL is active. Infact LG Chem which is one of largest producer of ABS globally is locally sourcing from BEPL as local characteristic, approval, quality cannot be met by imports from parents.

Overall ABS market to grow at 15% over next decade but colour and specially variant will grow at higher rate as innovation to replace metal with ABS in various application like Automotive, White Good etc is on rise

Competition;

Imports are basic ABS grade and low margin where BEPL is not focused. INEOS as competitor has high cost structure, frequent management changes, lack of local ownership and decision making and not aggression is helping BEPLto expand faster that overall market growth.There is not much scope for more competition due to

- Since it is very hazardous chemical process getting license is very difficult.

- Most of market would be capture by both local players with coming capacity (BEPL FY18-137KTPA + FY22 200 KTPA).

- It is very sticky business where product approval might take months to years and BEPL operates on cost + model which is win win for both.

- It is complicated process and make various combinations of color variant combined with different level of resistance and technology is concentrated with few players world wide.

Niche play:

Bhansali + Nippon JV is are bringing new variety/class of product in Indian market to meet changing customer preference. Infact Bhansali has employed 3 Nippon employee with high pay (around 8 to 10 lac/Month) for innovation and quality . 90% of business is by ABS in which 60% + are speciality variant and intends to grow in this area. They do supply basic ABS polymer to existing customer on request.

Capacity :

80 KTPA to 137 KTPA work as begin and machinery has been ordered. It is Brownfield expansion and capex would be 30 to 35 Cr and to be funded internally. This capacity will come by end of FY18.

For 200 KTPA, Greenfield expansion near Kandla will help to save 8 to 10% freight cost and make them more competitive. BEPL is talking to various interested party as equity participation to fund this capacity.

Others:

Promoters had pledge its shares to Allahabad bank decade back and its under arbitration. Management is actively working with bank to release its pledge.

MKG group an overhang for past few years has now completely exited.

Management would look to up stake from open market (2 lac bought on 20 June 2017, 1.5 lac share on 22 June 2017) and would like up till highest permissible limit (75% permissible) over period time

Takeaways:

Promoters are pure focus on ABS from past few decade and intends to be formidable players and no 1 in Indian market. BEPL is very debt averse and would continue to do so ahead.

Main promoters at 62 age is an hands on/at shop floor shows passion for its company.

OPM margin from current about 11+% will further enhance due Brownfield expansion(fixed OPEX) and focus on high margin and speciality grades.

Duopoly play in high growth market linked to direct consumption theme (Automotive 50% and white good segment and others rest)

Its has long term contract with all major client like Maruti, Hero Honda, Samsung, LG etc where raw material volatility up or down is factored in the contract which is win win for both BEPL still not able to meet latent demand and has to let go some customers. BEPL intends to ramp and achieve 100% utilisation from FY18

Disc: Invested from 39 levels.

9 Likes

P/L Before Other Inc. , Int., Excpt. Items & Tax is 9.14% of sales for BEPL and it is 6.9% of sales for INEOS Styrolution India. These figures are for the last FY 17 (source moneycontrol). The rise is share price immediately before the results seems spectacular. I tried to dig out some news about increase in capacity related to INEOS Styrolution India, but I couldn’t get any such information. With little investment, if BEPL can increase capacity through brownfield expansion (from 80 to 137), and if raw material prices remain favorable—this can lead to huge increase in profits, even before the proposed port based expansion is undertaken. Much of it can be considered speculative at this stage though.

Disclosure: invested at 25 levels.

1 Like

Excellent result from BEPL

No wonder promoter was buying heavily from the market

3 Likes

What abt expansion plan? Approved

It will be great if we get more input from AGM. Hope people from Mumbai will be attending it.

Great results…

Profit Before Other Inc. , Int., Excpt. Items & Tax jumps to more than 11% of sales for Q ending June 17. Most important question is: in what stages will the capacity expansion be planned? If everything else (cost of production and market value of products) remains stable, after expansion the EPS will be in the range of 10-12 and annual sales above 20000 million. These figures are not impossible… look at INEOS Styrolution India.

The future seems to be unfolding for BEPL.

1 Like

It will be great if People in Mumbai or those attending it, can share notes from Today’s AGM being held in Mumbai

INEOS are in 3segments, ABS being one of them. Are you comparing with the total revenue or only this segment revenue?

Hi…

Perhaps, you are referring to my first post dated 13 July. I have mentioned the total revenues of the company (INEOS) and not any particular segment. For FY ending Mar 17, Net Sales/Income from operations: 1,482.35; and Profit Before Other Inc. , Int., Excpt. Items & Tax: 102.33 Crores (6.9 % of sales). The source is Moneycontrol website.

I also recall reading that in case of INEOS the specialty ABS business is lower in comparison to BEPL that may be the reason for lower margins. I will like to add that in case of INEOS the net profit for FY 17 is little less than 70 Crore that will perhaps be the net profit of BEPL for FY 18 on 1000 crore revenue. So the difference in profits (in comparison to sales) becomes glaring. In case of INEOS there is no profit (or revenue) increase visibility in the near future. This seems pretty obvious that during FY 18 BEPL will cross INEOS in every possible financial indicator, except perhaps net worth.

If there are no short term loans and long term loans then why the company is paying Finance cost? As I can see a Finance cost of Rs 1.11Cr in Jun 17 results.

Has anybody asked this question along with pledged shares in the AGM?

2 Likes