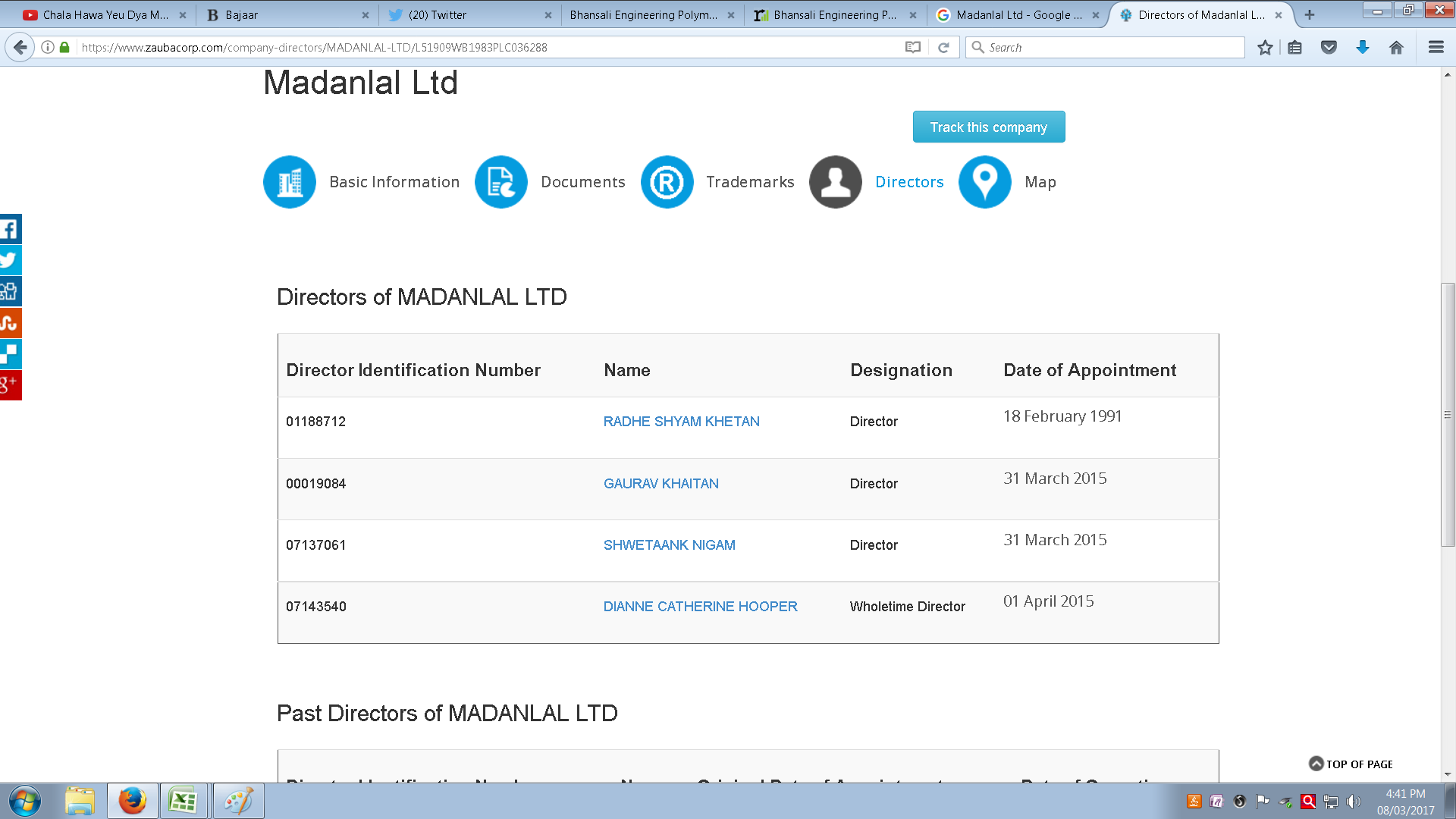

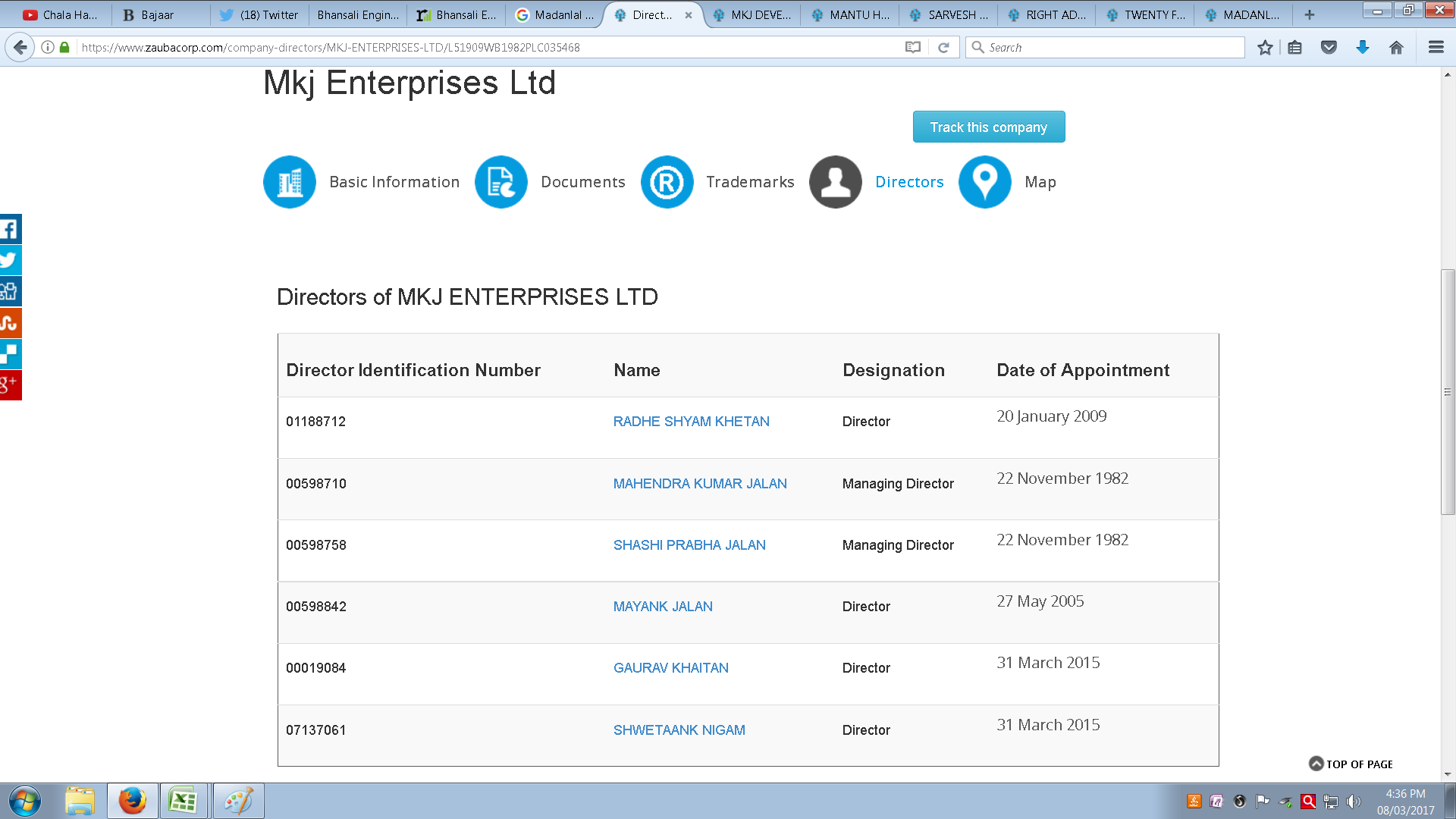

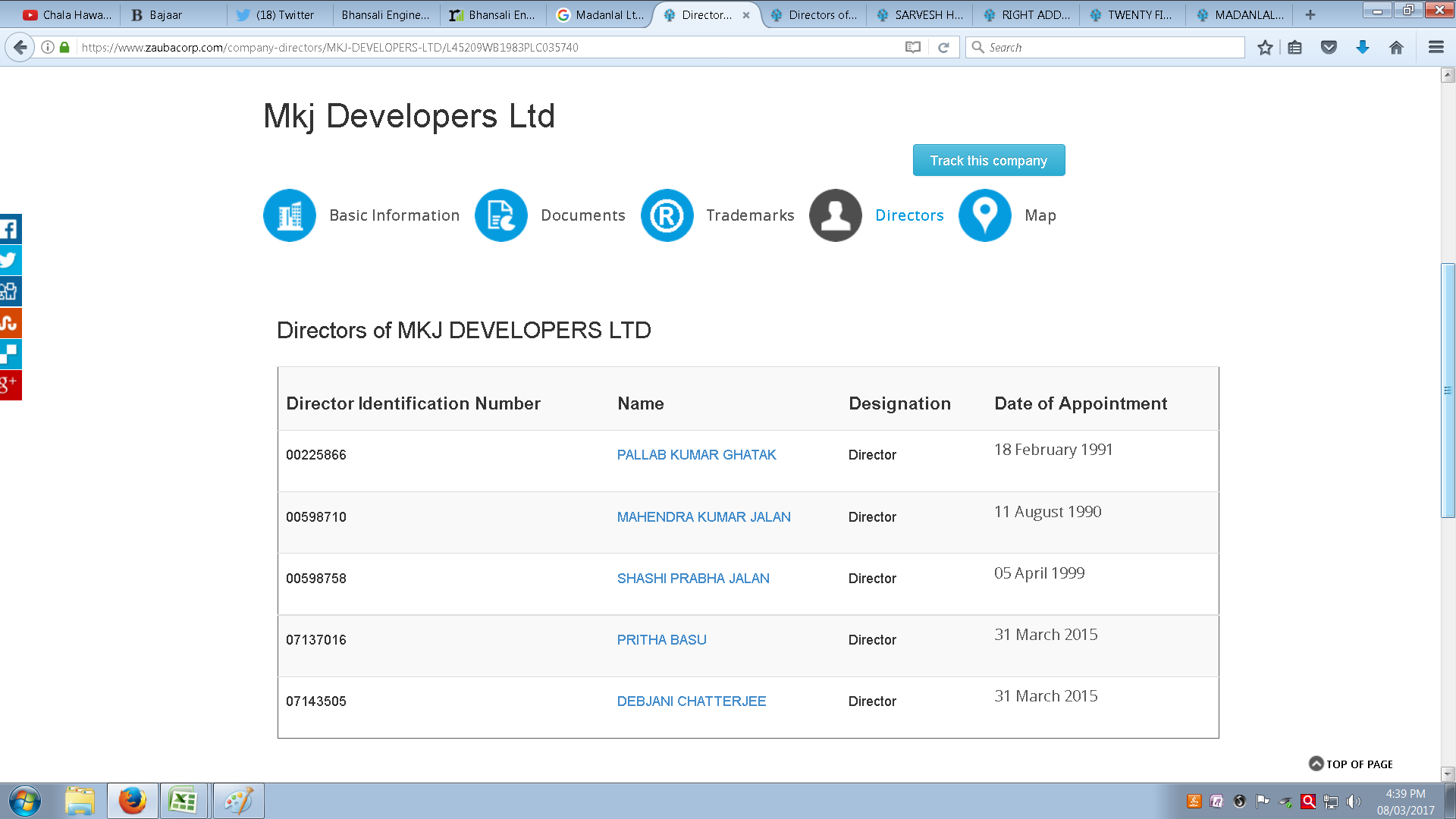

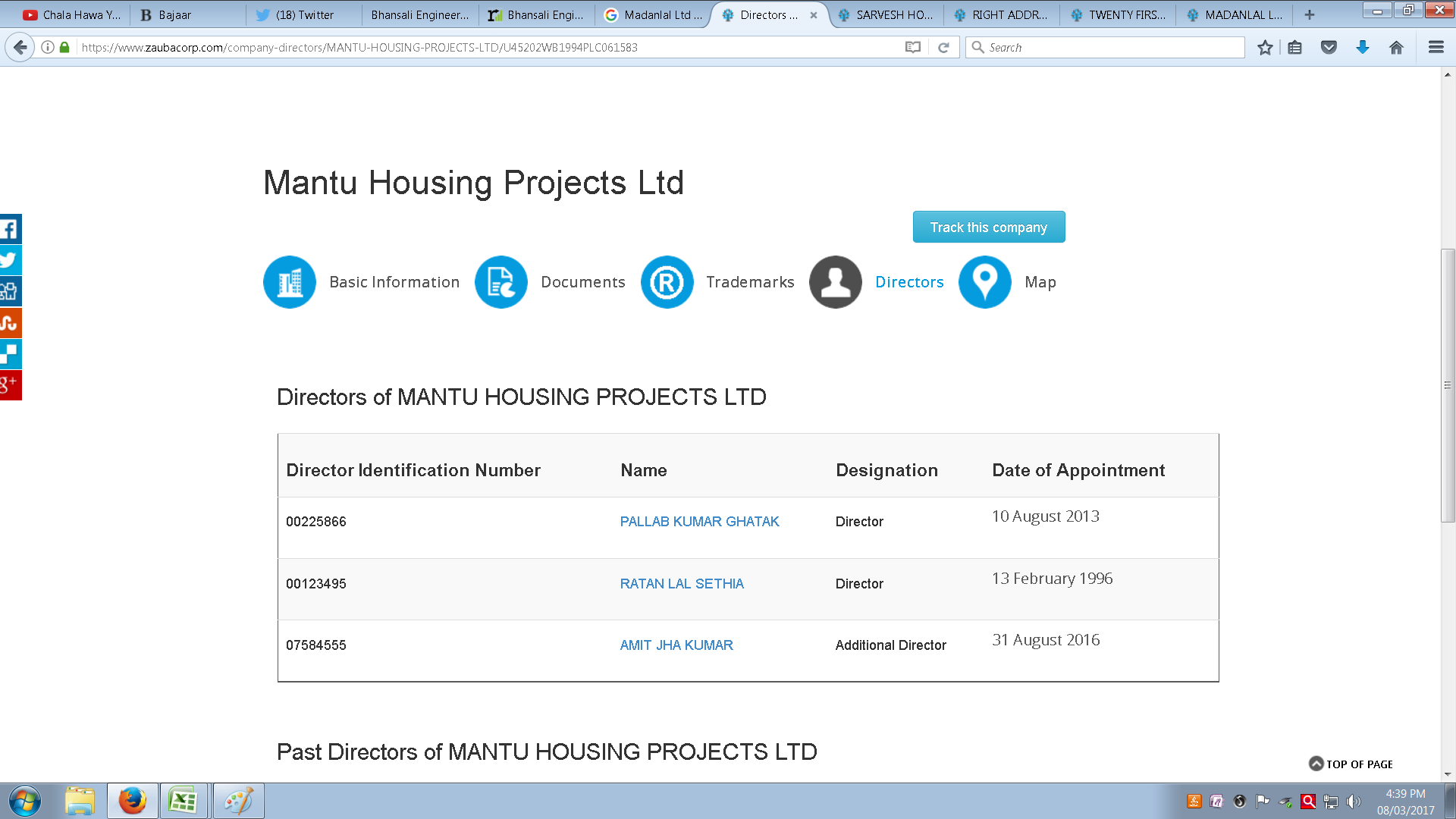

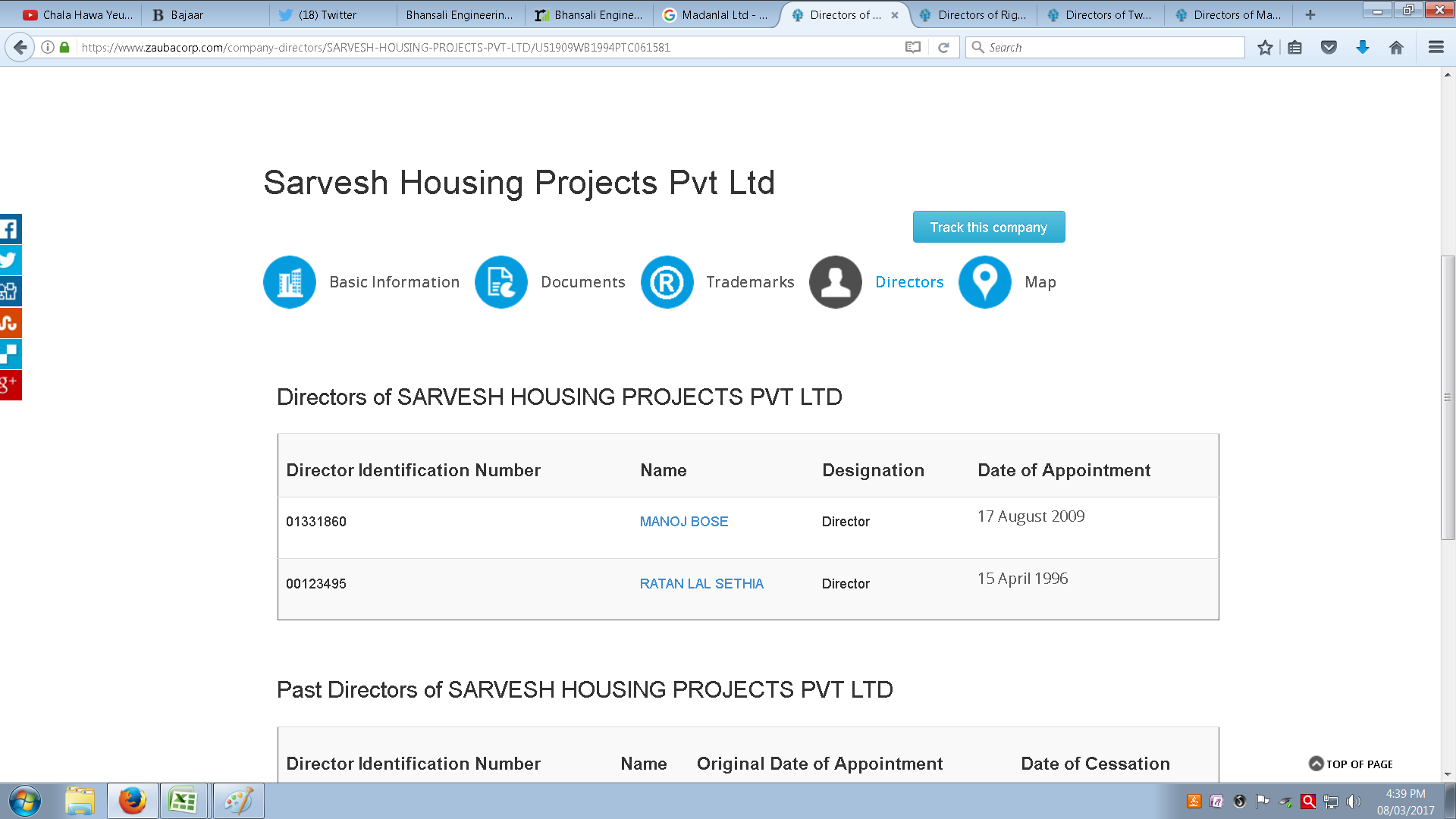

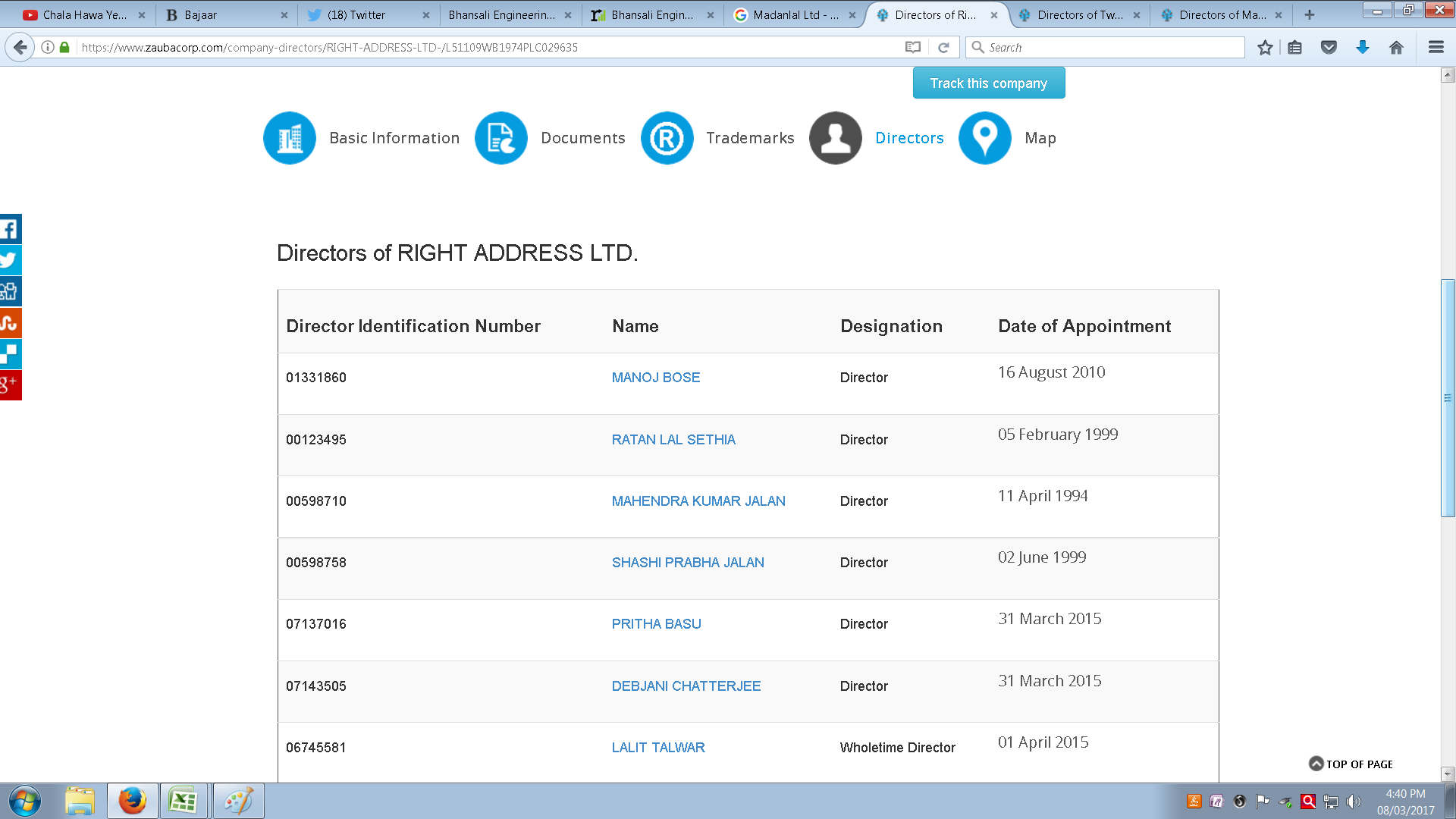

While calculating Promoter’s HOLDING I used to calculated Promoter"s holding along with related Party’s.

So we can understand is there any insider buying selling at expense of common shareholders

1)

2)

3)

4)

5)

6)

7)

While calculating Promoter’s HOLDING I used to calculated Promoter"s holding along with related Party’s.

So we can understand is there any insider buying selling at expense of common shareholders

1)

The shareholder of company viz. MKJ group of companies of Kolkata led by Mr Mahendra Kumar Jalan, had filed a case against the Company and its Directors in Company Law Board (CLB), Mumbai Bench, Mumbai in the month of September-2011, alleging oppression and mismanagement in the affairs of the company under section 397 and 398 of Companies Act, 1956, but were badly defeated pursuant to Order of the Company Law Board dated 24.09.2013 (Copy attached) and thereafter they filed an appeal in High Court, Mumbai under section 10F of Companies Act, 1956 against the aforesaid Order of CLB which was withdrawn by them suo moto. The Hon’ble High Court passed an Order (Copy attached) imposing a cost of Rs. 2.00 lakh on them finding that the case was devoid of merit and was frivolous, unsubstantiated and they abused the process of law for their vested interest and ulterior motives as also clearly stated in the said CLB Order(the detailed covering letter is attached).

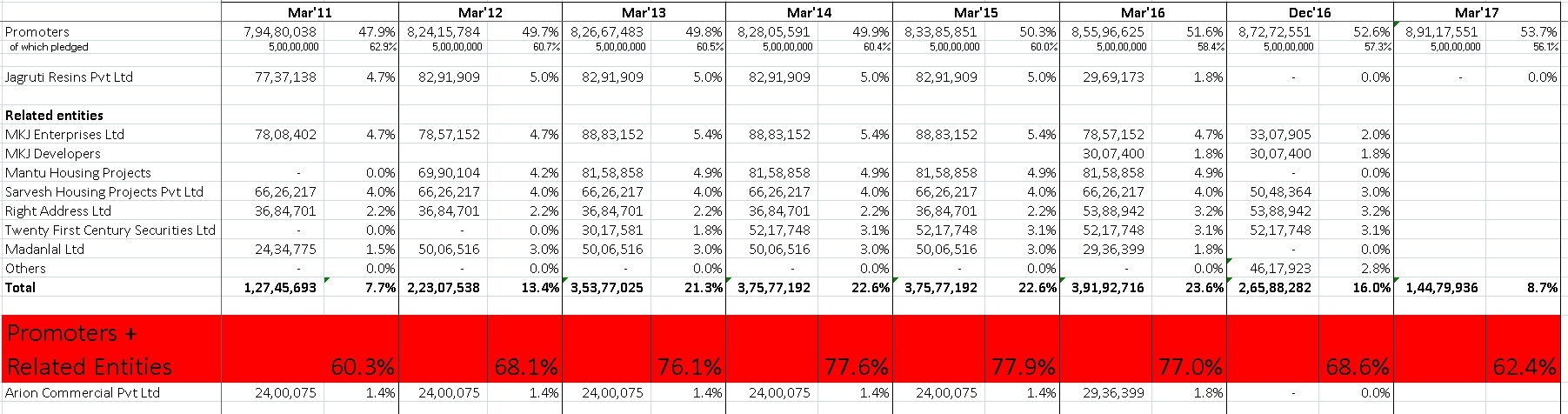

Here is the updated shareholding pattern till 21st March. All the “Non promoter” related entities have substantially sold off their holding. My guess is they will sell off entire holding in next few days. Promoter has bought a part of its, about 2.5% in Mar’17 quarter and promoter holding is now at 55%.

The historical analysis clearly brings out these “Non promoter” related entities bought shares, filed a frivolous case, brought share price down and increased shareholding. The High court has proved them guilty and now they are moving out.

Hopefully, the company will now be cleaned of mischievous shareholders and relentless selling may stop. The share price will now react more on fundamentals. BEPL - Shareholding.xlsx (14.1 KB)

Disclosure: Invested but insignificant portion of portfolio

Dear @RajeevJ

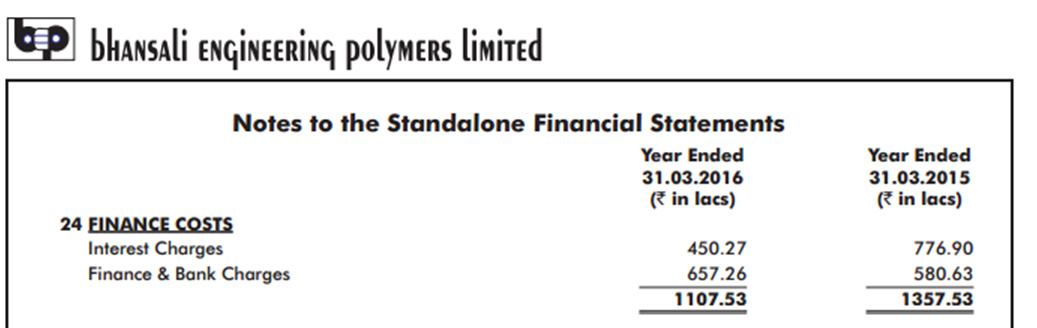

Not that it matters in the broader scheme of things, but i think there is an error in your computation of Interest charges for 2015. In your sheet it is 8.97cr but in the AR it is

Hi All,

BEPL looks interesting and I have taken up a tracking position in the co.

Just have a few questions, will be grateful if I can get answers.

How much is the CAPEX for proposed 120K MTPA capacity expansion?

By when is the capacity of 80K MTPA expected to be utilised fully? What will be the operating margins at the peak utilisation?

How does ABS from Bhansali compare on pricing w.r.t. imported ABS on CIF basis? The co. mentions need to match lower cost structures of international manufacturers due to higher efficiency and economies of scale.

How is competition in India? Any Indian competitor planning to expand capacity? This move could delay utilisation of expanded capacities.

ABS is a commodity as a product. The saving grace is that there are only a few manufacturers (Styro, DSM, Bhansali) in India plus not many exporters (Samsung, LG, Toray, Chi Mei and a few more) who fulfil short-supply. The industry structure helps maintain the prices. (Please correct me if I’m wrong.)

What stops new players in India to put up capacities? Do engineering polymers involve complex chemistry? Is there a minimum threshold to the level of capacity one has to put up to achieve competing cost structures? One reason could be that the end user of the processed product has to authorise the supplier of ABS resin, for e.g. Bajaj Auto has to approve ABS resin for its auto-part supplier. What could be the other reasons?

Thanks.

What a triangle breakout! explosive stuff enjoyed the move. If the prices form a flag or a pennant, we can expect more fireworks from this stock. The promoter concerns have been laid to rest finally and the stock has reacted like a rocket in a hurry to beat the escape velocity ![]() Investors could have gotten in at the throwback [ area in the green triangle ] - after the breakout. Also there were a lot of nano inverted h & s patterns forming spontaneously in the body of the triangle. These were all bullish signals and serious money to be made. For a serious value investor, besides the obvious valuation exercise , some basic knowledge of price patterns can give a wonderful edge and can make your performance look really good. I am slowly learning the value of this much derided art form.

Investors could have gotten in at the throwback [ area in the green triangle ] - after the breakout. Also there were a lot of nano inverted h & s patterns forming spontaneously in the body of the triangle. These were all bullish signals and serious money to be made. For a serious value investor, besides the obvious valuation exercise , some basic knowledge of price patterns can give a wonderful edge and can make your performance look really good. I am slowly learning the value of this much derided art form.

hi everyone …ineos styrosolution from the same sector also looks good…bepl has run up fast…ineos may be a turn around bet …with improved fundamentals for the sector as a whole

Has anyone been able to lay their hands on the consolidated results? The Co. has posted their stand alone results twice instead of their consolidated results.

The Co. came out with a great set of numbers for the March qtr. The markets probably had an inkling given that the stock doubled in the run up to the results. However, for some reason, it wants to keep its consolidated numbers under wraps which is strange. Hope there are no rude shocks in store! Though it approved the consolidated results, it has not put them out. Even the results published in various news papers are the stand alone results. We will have to wait for some more time to know how the joint venture with Nippon is playing out, but at least for now its share holders can feel happy that the story seems to be playing out well!

Hi, Can any one following this stock give long term expectation for 1-2 years? is price going to double in one year as profit also going to double?

Hey jagdish

No one knows whats going to happen to prices. However, if you have any views on the earnings & future prospects of the company it would be a good idea to post it here.

Hi,

the result is outstanding…yearly profit doubled and Qtrly profit 5 times…

also there promoter share increased from 52.60 to 55.69%

Missing part is expansion plan will continue or not.

senior people comment will be helpfull

As per the previous annual report,

They have already acquired the land in a port location ( location not disclosed ) for capacity expansion to reduce transportation cost and the movement of dangerous chemicals.

They implemented SAP for manufacturing operations and accounting which is a good sign .

Promoter is consistently buying in the open market which is also a good sign.

However , promoter pledged shares is not giving long term confidence.

From the annual report, management sounded very confident that clearly reflected in the recent quarterly results where the company posted excellent numbers.

Disclosure:: invested.

"Recently the company was given a non cooperating category by India ratings. "

India Ratings Affirms Bhansali Engineering Polymers at ‘IND BB+’ & Migrates Ratings to Non-Cooperating Category

Home · Press Releases · India Ratings Affirms Bhansali Engineering Polymers at ‘IND BB+’ & Migrates Ratings to Non-Cooperating Category

08

MAY 2017

By Neermoy Shah

India Ratings and Research (Ind-Ra) has affirmed Bhansali Engineering Polymers Limited’s (BEPL) Long-Term Issuer Rating at ‘IND BB+’. The Outlook is Stable. The rating action reflects the company’s financial performance during FY16 and FY17.

The ratings have also been migrated to the non-cooperating category. The issuer did not participate in the surveillance exercise despite continuous requests and follow ups by the agency. Thus, the rating is on the basis of best available information. The rating will now appear as ‘IND BB+(ISSUER NOT COOPERATING)’ on the agency’s website. The instrument-wise rating action is given below:

INR1,500

IND A4+(ISSUER NOT COOPERATING)

Affirmed and Migrated to Non-Cooperating Category

Note: ISSUER NOT COOPERATING: Issuer did not cooperate; Based on best available information

KEY RATING DRIVERS

The affirmation reflects an improvement in BEPL’s credit metrics. As per provisional financials for FY17, EBITDA/interest cover improved to 6.4x (FY16: 3.3x), driven by an increase in EBITDA margins to 8.9% (7%). The improved EBITDA/interest cover is above Ind-Ra’s earlier positive rating guideline of 2.5x. However, Ind-Ra is unable to determine the sustainability of the same in absence of any discussion with management regarding the company’s capex and other future plans.

BEPL did not participate in the surveillance exercise and provide information on working capital utilisation, sanction letters, future projections and management representation certifying timely debt service.

RATING SENSITIVITIES

Positive: A sustained improvement in the EBITDA margins leading to the interest coverage being sustained above 2.5x will result in a positive rating action.

Negative: Deterioration in the EBITDA margins leading to the interest coverage below 1.75x on a sustained basis will result in a negative rating action.

COMPANY PROFILE

Incorporated in 1986 in Mumbai, BEPL manufactures acrylonitrile butadiene styrene used for manufacturing plastic products such as drain-waste-vent pipe systems, musical instruments (recorders, plastic clarinets and piano movements), automotive trim components, automotive bumper bar, among others. The company’s overall operations are managed by Mr. B.M. Bhansali and Mr. Jay Bhansali.

RATING HISTORY

IND BB+(ISSUER NOT COOPERATING)/Stable

IND BB+/Stable

IND BB/Stable

IND BB(suspended)

Fund-based working capital limits

Long-term

INR600

IND BB+(ISSUER NOT COOPERATING)/Stable

IND BB+/Stable

IND BB

IND BB(suspended)

Non-fund-based limits

Short-term

INR1,500

IND A4+(ISSUER NOT COOPERATING)

IND A4+

IND A4+

IND A4+(suspended)

COMPLEXITY LEVEL OF INSTRUMENTS

After a hectic promoter buying in Feb-Mar 2017, the promoter once again bought from open market on 20th June.

If promoter has cash , why is he buying more shares and not reducing the pledge.

I received a mailer this week recommending BEPL which had completely plagiarised Anand Srinivasan’s post here from Jan 11. It was a complete copy/paste job. And a spam sms as well with a reco. I have noticed this sort of thing doesn’t usually end well and comes at the fag end of a bull run, before distribution starts.

Positives:-

Risk

Attaching the link to the latest AR for those unable to access it.

http://bhansaliabs.com/download/Bhansali-AR-2017-Full-for-mail.pdf

BEPL09-06-2017-Bhansali Engineer-Prabhudas.pdf (587.3 KB)

As PL is saying ‘Currently the company is debt free. Going forward the management has maintained that it will not borrow for capex or for working capital requirements. They have also indicated that they do not plan to dilute equity’ …

all these fine, then why Pledged Shares are not getting removed