It was mentioned in this same thread long ago that the promoters would very much like to remove the pledge but there is some legacy issue. It is not clear what exactly is the issue. Please see this:

1 Like

yeah that is what I do not understand. What exactly one means by “legacy issue”. Sorry I am kinda new to investment field so I might not be aware.

what is stopping other big players in specialty chemical to set up an ABS manufacturing plant?..

there is a clear demand, market expected to grow approx. 15% but there are only 2 players in India,…

can anyone help me to understand.

thank you.

BEPL in thier annual report has stated that there are significatnt entry barriers in this business. they have cited an example that LG india buys ABS from India or import it, even though LG chemicals is one of the biggest manufacturer of ABS in world

Expecting BEPL to end topline between 990-1000 crs and OP between 160-165 crs. this year, 2017-18. Need to see. Anything better than this, good bonus.

If LG-Chem is the biggest manufacturer in the world, there is no barrier to entry for LG-Chem to enter ABS manufacturing in India.

As per the information available online, BEPL is investing 1000 Crores for 200,000MTPA. until last year BEPL has a capacity of about 51000MTPA. so rough calculation comes to 200Cr for 50MTPA. This is not a huge capital for chemical companies in India.

in online i see SABIC and other Japnese and Korean companies offering to license their manufacturing process. so I don’t see there is again a barrier to entry…

something does not add up to the current ABS market in India.

2 Likes

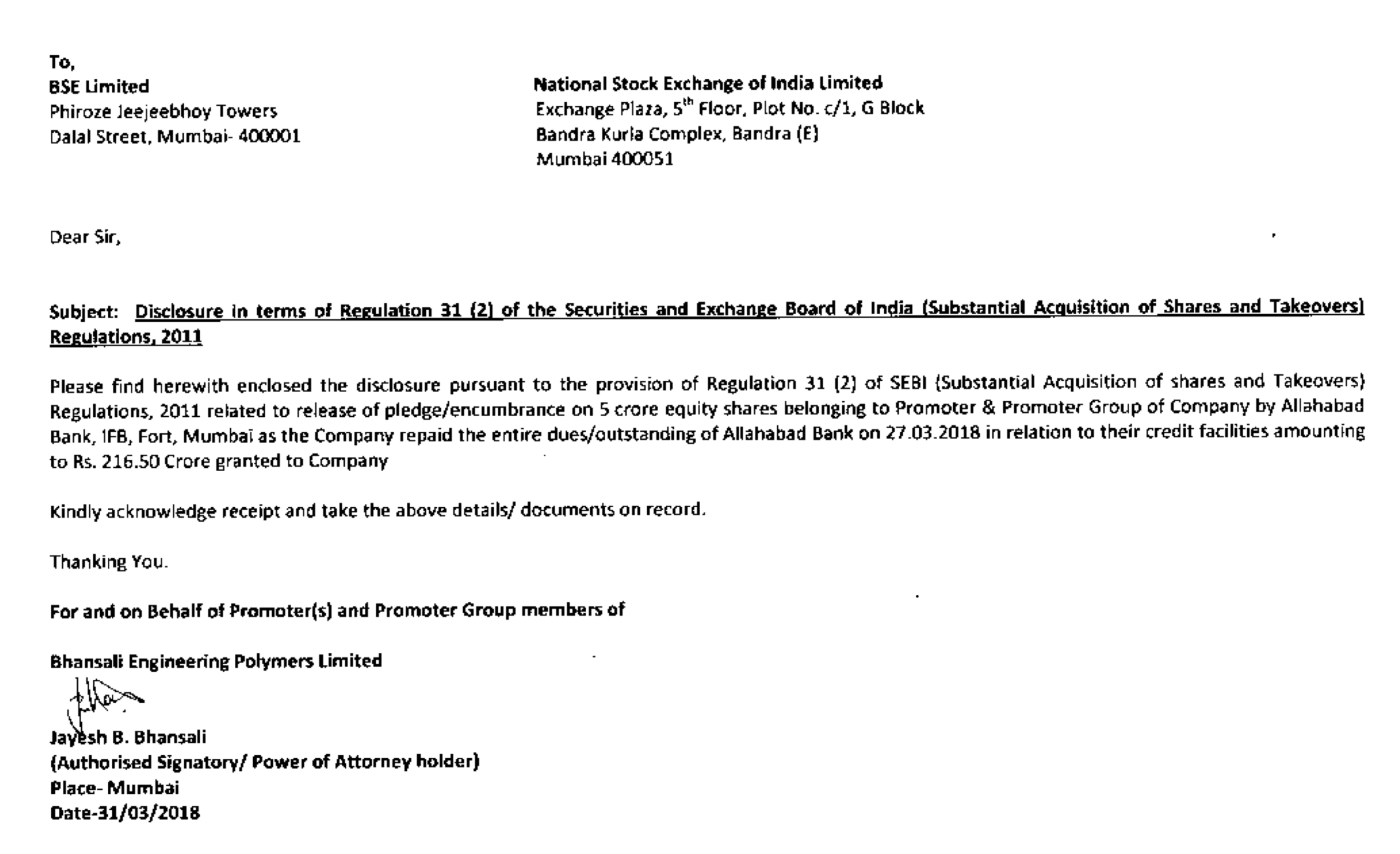

Pledge has been released fully. Check BSE site for the letter from Allahabad bank. Good news.

3 Likes

Very good news for not only release of 5 crores of pledged shares which were almost 30% of equity but also personal guaranty, land and plant machinery hypothecated to Bank released.

Communication in respect of implementation of ABS capacity expansion plan of the company from 80 KTPA to 100 KTPA at its Abu Road Unit:

Also, the company has informed that the Q4 results will be announced on 13-Apr

1 Like

Hem Securities is bullish on Bhansali Engineering Polymers and has recommended buy rating on the stock with a target price of Rs 255 in its research report dated April 10, 2018:

1 Like

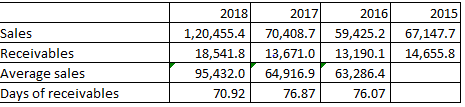

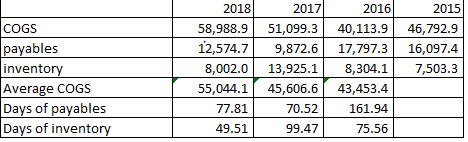

Standalone & Consolidated results for Q4 and the full year are out. Net profit of 99.80 crores on revenue of 1204.55 crores, zero short-term debt appear good, however increase in trade receivables from 136 to 185 crores is of concern

Current P/E is close to 35 which is fair for a 30% growing company, but upside seems limited in my view. Operating efficiency of the expanded Abu Road plant will be of interest for immediate margin expansion.

Disclosure: Hold, 8% of portfolio.

don’t just look at the absolute amount of receivables…the days sales outstanding have gone down 10% from 70 to 63…which means the company is collecting it’s receivables much faster than before…

otherwise also, the result is outstanding!

FY18 revenue growth 51%

pat growth 185%

ebitda margin@ 15% (compared to 9% in fy17 and 6% in fy16)

pat margin@ 9% (compared to 5% in fy17 and 3% in fy16)

debt to equity down to almost zero after repayment of 217cr of debt

disclosure: invested

Debtors write-off of 8 odd cr has sullied what could have been a phenomenal quarter.

![]()

Assumption: All sales are considered credit sales for calculating receivables days

The performance has improved on every front be it margins, cash conversion, solvency … The only problem is the run-up in the share price and hence definitely not a fresh investment opportunity for a long-term investor. However there still seems some upside especially with Abu expansion advanced by one year. Q1 FY19 results would give a better picture on the future prospects.

Also if we ignore the one time 8 cr write off from Q4 FY 18 results, the EPS cmes to 6.43 valuing it at 32 P/E( fairly priced currently - although I would be comfortable with a 35 P/E for this firm especially with the auto sector booming and industry duopoly and considering Bhansali being the better of two)

Disclosure: invested from 50 levels

BEPL - this 8 crs writeoff is puzzling still. In case you supply to Tier-1 Vendors and with Auto industry booming , why there is writeoff ? Is there something behind the smock ?

BEPL- going forward margin will be 12-14 % as it has to import RM and process it …

You may not get the explosive growth as base effect also kicks in…

All these are my analysis…

Disc Invested . PF% less than 1 now from earlier 7 %

1 Like

Purchase of stock-in-trade, almost absent till last year, is Rs.102 crores. This has produced 15-20 % of the revenue (material cost of in-house production is Rs.590 crores). This points strong demand, which the company is unable to meet from its own capacity. So it has sourced finished products from outside. While this is a positive, it also means that when the new capacity comes up, in-house production will replace these purchases. To that extent, new capacity will not contribute to topline growth. Part of the future topline growth has already come in this year. Margins should still improve though.

This is an item that should be watched.

10 Likes

As I mentioned earlier, there is a decelerating trend in BEPL top and bottom line. BEPL saved the day on topline through import , and also suffered exchange loss

As @chandragupta mentioned, I fulled agree, you may not see, substantial top line growth in coming days, till that 37KTPA expansion happens.

I agree with you that write off Rs. 8 Crore debtors is a huge amount (around 8% of profit) & matter of concern and also debtors has increased in absolute amount. Just writing a line that all the actions has been taken against defaulter is not enough. I think something more is there, keep a watch.

Just like those with BEPL in their portfolio have a vested interest, those planning to invest also have an interest in writing negative and bringing the price down to find a good entry point. Credit goes to the mgmt for being transparent about the write-off and exchange loss otherwise they could’ve just gotten away without anyone knowing why other expenses have gone up. IMO, although the stock had priced in a good result already, today’s selloff was more a knee jerk reaction and it has entered oversold territory.

Disclosure: invested

1 Like