I think we are going to hear such commentary from many chemicals companies, supplying their product to other final product manufacturers…when final product manufacturer is under stress, they put more stress /squeezes their suppliers!!

I think downward journey started in such industries and expecting de-rating in PE of such companies

Global slow down indicator:

Globally world leader BASF is not happy and forecasting H2 profit slowdown worst than 2008 crisis…

https://www.icis.com/explore/resources/news/2019/07/10/10389609/insight-basf-profit-warning-signals-major-chemicals-slowdown-in-second-half

https://www.bloomberg.com/news/articles/2019-07-08/basf-cuts-2019-outlook-citing-trade-conflict-industrial-output

1 Like

I had attended Balaji Amines concall yesterday. Some of the points I noted during the concall:

• Q1FY19 was an exceptional quarter as prices of many products had surged during the period.

• EBITDA was impacted by volatility in prices of raw materials and slow down in end user industry

• End user pharma – 55%, agrochemicals – 20%, other segments like dyes etc contributed 5% each.

• First and only company to manufacture amines through our own proprietary technology.

• Strength of Balaji also lies in the diversified product basket.

• No major dependence on China for RM. Our specialty is to develop the technology and raw material in India.

• In Q1Fy20, got long awaited clearance for morpholine expansion. Only 3 major p

• Acetonitrile – 18,000 capacity with installed capacity of 9000 MT. Started manufacturing from July onward and target to do 4000 – 5000 MT this year

• 6 month acetonitrile and THF for 6 months manufacturing. Margins on both the products are on higher side.

• Balaji Speciality chemicals – consent to operate received in June, 2019. Production of ethylene diamine and other niche products. 250 crore – subsidiary company infused. Margins will be similar to Balaji Amines. Ethyele Diamine goes into UPL, Coromondal and Indofil for manufacturing of mancozeb. Balaji Amines will break monopoly of MNCs like Dow etc in India.

• 90 acre plant – received mega status. Applied for NOC. Land digging will start in next quarter. Will take 15 months to commence – total capex is 200 crore. 120 will be bank funding and rest will be internal accrual funded.

• Hotel business is doing well and started contributing to bottom line. 60.6% occupancy. Cash profits – 1.35 crore during Q1FY20.

• RM – methanol has been taken care as per last call? What led to decline in gross margin? Inventory losses during the quarter. Inventory was at higher prices. Pharma and agro industry also not doing well in the quarter. Competitive pressure? Its not because of peers – everyone is in same boat. End user industry is not doing well. We were having purchases at higher prices in last quarter which led to inventory losses.

• This year – acetonitrile and morpoholine growth will be there from enhanced capacity.

• Second half in subsidiary, Balaji Speciality, will contribute to 90 crore sales and see pick up in H2.

• Break up of domestic and export sales for Q1FY20? 20% exports and rest domestic

• Some RM purchased from Balaji Amines into subsidiary.

• Guidance – depreciation and interest expenses for Balaji Speciality? Entire thing is capitalized and we will see entire figure from Q2FY20 only.

• Demand side? Current quarter (Q2) will be better but not much growth. H2 will see some recovery. It’s a cycle followed by pharma and agrochemical. H2 will definitely be better. Guidance for standalone? 1050 crore of revenue but will decline if RM prices decline.

• Volume growth last quarter? No growth during the quarter. 3 – 4% decline in the quarter.

• Volume growth target for FY20? 10% growth.

• Current volume from agrochemicals and pharma – 70 – 75% sales from the two segment.

• Methanol sourcing from overseas – taking at spot only. Procurement from outside only. 35% is directly sourced while remaining is sourced through traders. Not facing any issues on sourcing of methanol.

• Morpholine – we will utilize full capacity while acetonitrile we see sales of 3000 – 4000 MT. Dimethyl Amine also expecting some growth.

• Inventory loss this quarter? No pricing policy. Depends on markets. Fix prices every month.

• API and Pharma – 55% and agrochemicals – 20% of sales.

• Amines revenue – 23.5% sales, amines derivatives – 23.5% and result comes from speciality chemicals.

• Inventory loss during the quarter? Opening quarter inventory at higher prices while prices declined in the quarter. Methanol and one more RM prices have declined.

• Margins – guidance of 18 – 20% EBITDA margins? Morpholine, acetonitrile

• Capex guidance – 200 crore in FY20. Nothing in subsidiary – everything is in standalone balance sheet. Next year capex – we will first stabilize the existing capacity and then go for expansion.

• What is giving you guidance for volume growth in H2? In past 5 – 6 years, we have seen Q1 and Q2 haven’t been better but H2 was much better. Since July is completed, we get a sense that Q2 will not be good. In our segment, we supply to metmorfin and we feel that growth will be there after slowdown in first few quarters.

• 1050 crore guidance includes acetonitrile and morpholine sales for FY20.

• Greenfield capex? We will start land digging from next quarter.

• Volume for Q4FY19? Total volume 21, 543 MT.

• DMA HCL sales volume in Q1FY20 – main slowdown in DMA HCL only. H2 should pick up.

• Mega project – 200 crore capex? Rationale of going into ethyl amines where Alkyl is present in a big way? Looking for future not just this quarter. That is the reason we have taken that.

• Government clarification on methanol sourcing policy? Nothing from Government. Majority of methanol is coming from outside country only. Alternate arrangement? Qatar, Petronas and other countries we can import. Also, Deepak Fertilizers we can source methanol. Matter of 2 – 3 weeks only for passing on the prices of raw material.

• Agrochemical markets? More into exports or domestic? We have more into domestic market sales. Export sales doing different in different markets.

• Capacity utilisation at standalone level – 80 – 85%. DMA – 30% capacity

• Debt levels – standalone – no debt. Consolidated level – subsidiary taken 120 crore for which we have paid 20 crore. Total debt of 100 – 110 crore.

• Incremental revenue from expanded capacities of morpholine and acetonitrile? 100 – 120 crore.

• Improvement in specialty chemical volume but realization gone down? Some products going into API and Pharma which were not doing well.

• Other income during the quarter has gone up? This is one time. Some FDs for LC and some advances including sales tax refund have come as one time income. All because of interest income only.

• FY21 – standalone revenue – 1100 – 1200 crore. Coming year FY22 revenue – 100 – 150 crore of additional revenue from green field will come.

• DMF – 46,000 MT annual consumption. 35,000 MT is being imported from India. Sometimes the prices are less than our raw material prices.

• Subsidiary we had infused some capital in subsidiary.

• Green field capex – no other expansion plans at present? No. As of now no plans but have many products in pipeline. After stabilization of the subsidiary and green field capex we will look for expansion as we have many products in pipeline.

• Expect better H2 performance.

• Acetonitrile prices have increased from 100 to 250 – 300 per liter. We don’t have detailed data since we will start production this quarter.

• We are not sure if UPL will manufacture ethline diamine.

8 Likes

Results_Jun2019.pdf (334.4 KB)

Excellent numbers from Alkyl Amines. Acetonitrile prices must have played a part but overall these numbers deserve a closer look and signify reshaping of Indian Amines industry in terms of market share.

Rgds.

Hello all!

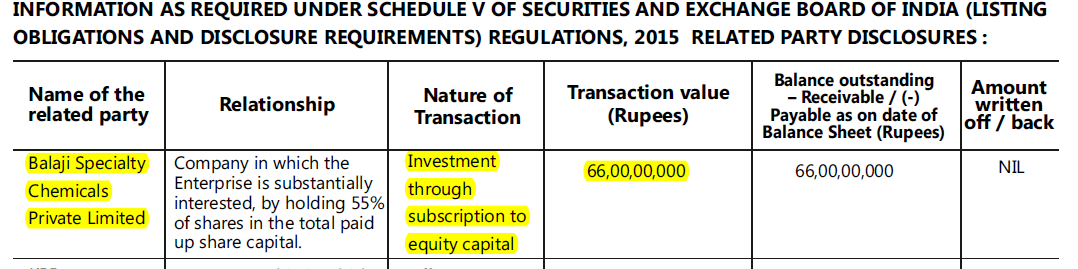

I am writing just to confirm my understanding of the investment in Balaji Speciality clearly.

From what I read, Balaji Amines paid Rs. 66 cr for 55% stake in Balaji Speciality in FY18.

Source: FY18 Annual Report of Balaji Amines

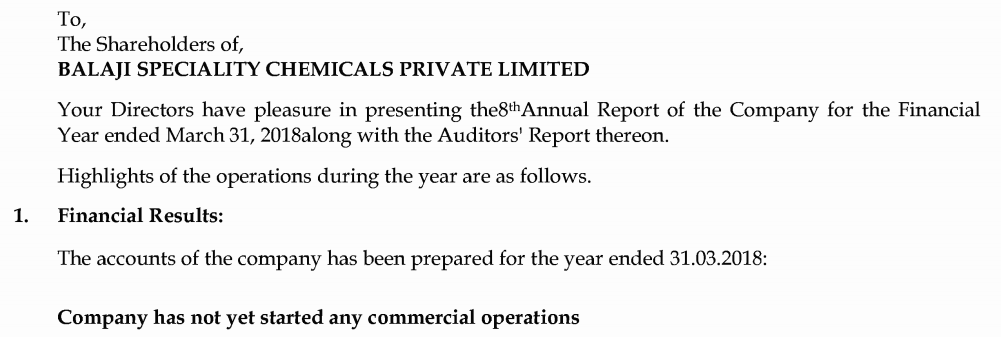

Also in the year FY18, the company had ZERO revenue.

Source: FY18 Annual Report of Balaji Speciality

So basically, the other promoters of Balaji Specialty got Rs. 66 Cr just like that.

Am I missing something here?

I am ambivalent on this particular point. However this is how I see the above transaction:

The promoters through the purchase of 55% stake @ 66 crores value the company at 120 crores

From the above reported numbers BSCL net worth comes to 84 crores.

Management had given guidance for FY20 revenues from BSCL would be 80 to 90 crores (against 100 to 150 crores earlier)

So triangulating from the above figures we have the following:

Price to Book = 120/84 = 1.42

Price to Sales = 120/80 = 1.5 (on the higher end)

IMHO the valuation does not seem too egregious considering they have at least 2 big customers in Indofil and Coramandel who are ready to buy their products (assuming they get the product approvals)

I am no accounting expert. Happy to be corrected on the above logic and calculations.

5 Likes

1 Like

https://www.investing-notes.com/balaji-amines-ltd-bse-530999-nse-balamines/

An analyst’s note on Balaji Amines.

Conference call recording is not yet uploaded on researchbytes. Does someone know another place?

Anyways, did anyone join the conf call? Did u get to know any growth and margin projections in next quarter?

http://www.balajiamines.com/pdf/1580730592Investor%20Presentation%20-%20FEB%202020.pdf

One of the earliest company covered in VP since 2010. Created huge wealth. How is it at CMP specially in view of Covid crisis and lockout impacting indias manufacturing sector and end users of cos products ?

Would it be a good buy on expected bad qtr nos of Q1 or Q2 or even at CMP? Views invited.

Main issue seems to be the difficulty in ramping up Balaji specialty chemicals. That would’ve been the primary driver of growth. Apart from that they only have some spare capacity of Acetonitrile and Morpholine to drive growth. Mega project as the presentation states will not start till end of next year.

1 Like

77% of the company’s revenues come from Pharma and Agri sectors. Even if there are short term disruptions in supply chain, the end demand is relatively better in these sectors, versus others.

1 Like

for any major growth in the top and bottomline, we will have to wait for the new volumes to come into play. Company had halted capex for the past few years to bring down the debt. In hindsight, it looks like a very good decision.

disclosure: holding

1 Like

Hi Guys,

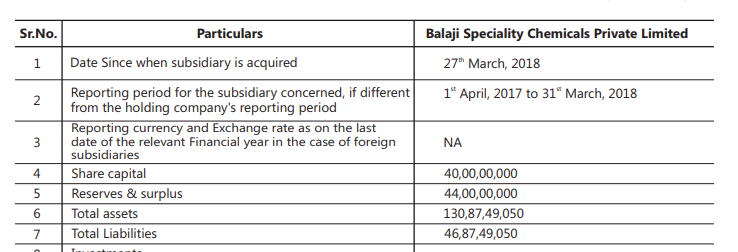

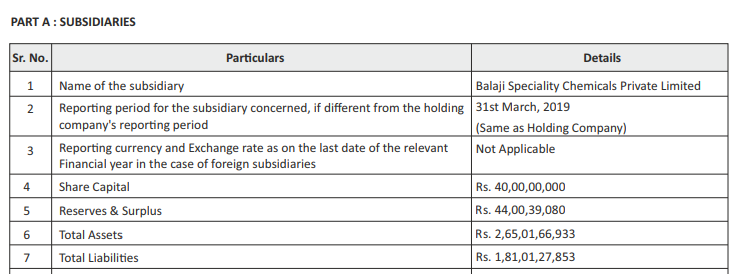

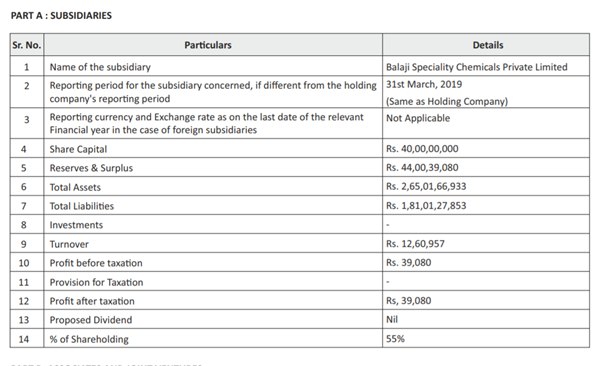

i’m struggling a bit to understand the mismatch between the magnitude of reserves/share capital/assets of Balaji’s subsidiary (Balaji speciality chemicals) viz a viz the total turnover and profit which are a fraction of the assets. Can anyone make sense of this data. Source - Annual report 2018-19

Cheers

Uzi

Any specific reasons?

They diversify into unrelated areas like hotels instead of doing simple things like paying dividends. Alkyl amines much better. They just focus on their core areas.

1 Like

Went through the Annual report of Balaji and had a question for keen company observers

- How do you view the 175 cr corporate guarantees from Balaji Amines to its subsidiaries. This definitely inflates the balance sheet. I’m not sure how to evaluate this?

- Does anyone know whats the current sales figures from balaji speciality chemicals. in the snapshot that i posted before it seems unrealistically low considering they have a target of 350-400 crores in FY21 or FY22 (not sure which FY)

Cheers

1 Like

Balaji Speciality Chemicals has recently set up new facilities. These will take time to stabilize and production is expected a few quarters down the line. A lot of this has been discussed in earlier posts on this thread.

disclosure:holding.

1 Like

Before Covid the plant were running at - 70% capacity utilization

Gap Break between Shutdown and reopen was on April & May

Current Capacity Utilization at 85-90%

YoY Growth : 19%

2 Likes

Balaji amine

Takeaways from the earnings conference call:

Balaji Specialty Chemicals (BSCPL): The company commenced the commercial

production of Ethylene Diamine (EDA) and Piperazine in Q2FY20. 4QFY20

revenue/EBITDA from BSCPL stood at INR 210/9mn representing 2.2/0.5% of

consol Sales/EBITDA. The plant’s utilisation is expected to rise to 30-40% by Mar-

22. At full utilization, the subsidiary should contribute INR 2.5bn to the BAL’s

consolidated topline, i.e. 27% of BAL’s sales in FY20.

Gross debt: Compared to INR 1bn in short term debt taken by the standalone

entity, consol debt stands at INR 2.4bn. This is largely owing long term

borrowings of INR 1.3bn taken by BSCPL.

The Greenfield project: The commercial production has been pushed back to

Mar-21 (earlier, Dec-20).

Capex: BAL has spent INR 720mn on the Greenfield project and plans to incur an

additional INR 700-750mn in FY21.

1QFY21: Plant utilisation stood at 70-75% in April, 80-85% in May and at pre-

Covid-19 levels in June. BAL’s hotel continues to remain inoperative in the

current environment. Fixed cost from this business stand at INR 2.2mn/month.

Acetonitrile: BAL is currently producing ~5-6ktpa of Acetonitrile, whose prices

are expected to remain elevated in the near term as the alternate process to

produce acetonitrile is currently economically unviable.

7 Likes