Some key points from the conference call. I listened to about 40 minutes of the call. Missing any key announcements made after the 40 min mark. Other members are encouraged to add more.

Planning to launch a comprehensive payment system (digital wallet + co-branded credit card). Announcements to come soon.

Tieups now with top 3 ecommerce players - Amazon, Snapdeal and Flipkart - for their EMI card financing.

Co. anticipates deterioration in credit quality for consumer durables. Based on their risk assessments they have tightened the screws this quarter (Sep-Dec 2016). However they did not mention whether this would lead to slower growth or de-growth of the consumer durables portfolio.

EMI cards and Retail EMI cards business doing very well. Especially the partnership with Future Group has generated tremendous response. 25% repeat transactions.

LAP now on 100% direct-to-consumer model. Although there was a de-growth of 38% (YoY basis), this portfolio is expected to grow going forward.

Indian NBFCs : Shadow banks may hit a bump on frothy valuations.

Every bull market needs a hot theme that can fuel fervor and frenzy among investors. Usually that crown is reserved for an emerging sector that is long on promises, but short on specifics. Internet boom in 2000 was one such classical case. But, this time, bucking the trend, market has latched on to one of the most unlikely sectors for its steroid. It is not a sexy emerging business. It is an age-old dull business that has been around since the time private businesses took roots. Lending is no fancy business, but, by taking NBFCs and other retail financing co’s to lofty levels of valuations, Indian market hasn’t disappointed its ardent followers by showing how insanely irrational it can stoop to.

Like every hot trend, it starts with certain fundamental triggers, but soon gets hijacked by hyper momentum. It is no different in this case. To begin with, the prospects for NBFCs and retail lending brightened with key fundamental triggers such as,

Increased credit demand on falling interest rates

Improved profit outlook for lending on lower cost of funding

Significant market share gains for NBFCs (including HFCs (Housing Fin Cos)) at the cost of large banks such as ICICI, Axis and SBI that are saddled with stressed assets.

Increased liquidity to NBFCs/HFCs from alternate source of funding (besides banks) to tap into this growing opportunity.

Increased demand outlook for HFCs from rural and semi-urban.

Surging demand for microfinance post stability in regulatory norms.

While these factors in isolation may look not very unusual, the combinations coming together conspired a deadly revival in the earnings momentum for this sector. That set the bull case for the sector. Once in control of bulls, soon, momentum morphed into mania leading to froth in valuation in much of the stocks in the sector. Stocks such as Bajaj Fin, Canfin homes, Gruh Finance , Equitas and Ujjivan have surged and are quoting at unsustainable price-to-book valuations. Valuation multiple for most of these companies are much higher than established and well run larger players like HDFC and HDFC Bank. Take for example, Bajaj Fin is at over 8 times the price to book (FY16) while the multiple for HDFC Bank is less than 4.5. Gruh Fin is at the fanciest level at over 14 times P/B multiple.

Such froth in this sector is scary for the simple reason that the business model of lending is murky at its core. It is a business where profits are front-loaded and losses are back-ended and thus making the business fundamentally risky. Loans are easy to give and so are profits in the beginning. But when loans sour later ( as in most cases), write-offs come back to hit in a back-loaded fashion. This is not to say that this business can’t be run conservatively. But the inherent risks in the lending business make it an average business at best or a fragile one at worse. Valuing such businesses at stupendous multiples like the ones in the current market is fraught with ruinous risks which the investor can ill afford. Froth in this space gives an excellent window for investors to exit positions clinically. While it could impact the returns in the short-term given the daily surge in stock prices in this space, it will prove to be a prudent one in the long-term with these stocks set for major regression in the eventual correction.

Hi Amit,

Do you think 2.7 and 2.78 p/b for ujjivan and equitas respectively is too much ? Would like to know why and what should be ideal range. Trying to learn more about BFSI space and thats he intent

Disc : Hold multiple stocks in BFSI as portfolio basket approach

This is what Basant Maheshwari thinks. Quite opposite.

''But there is one space on which I am super bullish. Before you ask me for three names, I can tell you indicatively – one is mortgage finance, second one is a small finance bank and the third is the micro finance sector. So there are several critics in the market but majority thinking does not make a bubble, majority buying does.I do not think the majority have actually gone and bought these stocks because their market caps do not tell you that the majority have bought them. ‘’

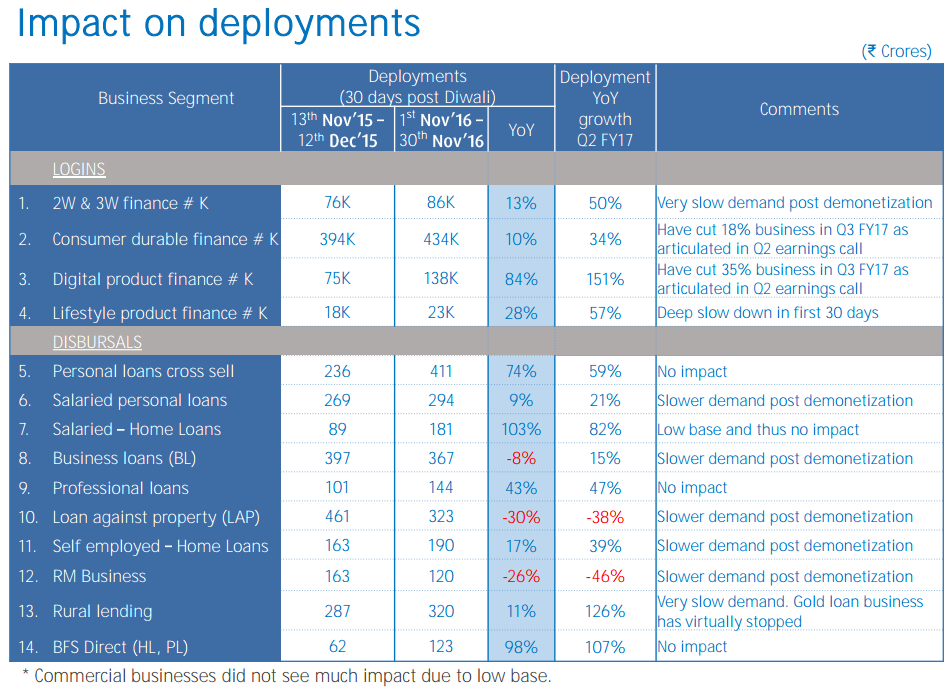

Of the many segments that the company operates in., the only segment that may have a short term negative impact is the 2-wheeler & 3-wheeler finance one.

This segment contributes to 9% of total disbursements., out of which 30% are cash collection models.

Rest of the segments seem to be marginally affected.

The management & its disclosures are simply one of the best.

That was a great presentation to understand these type of businesses.

Cash collection model is only:

30% of 9% of 2-wheeler & 3-wheeler

Some Gold loan portion of rural finance

Cash collection should be less than 6% of total loan collection and the stock fell over 35%! Net-net demonetization is actually positive for Bajaj Finance.

Not many would have thought that one day you could finance weddings thru formal channel

A great example of:

How credit will penetrate more into unorganised markets?

How a capable management with a history of innovations in an age-old business is more likely to continue with its good habits, in good times and the bad

This is the 3rd announcement after demonitization on tie-ups being done by BFL on buy now, pay later model. The other two were Lloyd and LG.

Correlation does not mean causation. Just because Bajaj Finance released a presentation today and its share price dropped close to 6%, does not mean that the market reaction was in response to the release of new information. Highly irresponsible journalism I must say. They could go a step ahead and say crude oil prices jump 5% post Bajaj Finance management updates on the impact of demonetisation.

BF conducted a conference call today (I’ll share notes in some time). In fact, the impact of demonetisation has not been that bad, and only certain parts of the business have been affected. Other parts are growing steadily. A key takeaway from the call was that the business is doing and is expected to do well.

LAP & business loans have been impacted, but mostly due to company’s own policy of bringing down high ticket luxury loans. Impact of demonetisation has been 5 to 6%, while impact due to company’s own policies has been ~25%. Overall impact 30%

CD financing has seen slower growth, not due to demonetisation, but due to company’s strategy to tighten screws on this portfolio till December. They had mentioned this in the last quarterly conference call. Please see my last post

Other parts of the loan book have seen good growth despite demonetisation. Overall the loan book is expected to grow, with more focus on retail loans.

They did a YoY comparison of deployments in a 30 day period post Diwali. Here is a screenshot from the presentation.

Loan book can be categorized into 2 broad categories depending on the profile of the customer - affluent loan book (92%) and mass loan book (8% of the portfolio)

Collections have only been affected in 8% of the total loan book. This is mostly 2W/3W loans and rural loans. Collection efficiency has dropped from pre-demonetization levels of 90% to ~68% and this is expected to improve as the pace of re-monetisation picks up.

No impact on 92% of the loan book.

Been investing in non-cash channels of collections. This process has been accelerated due to demonetisation.

Company has increased dongles on ground, from ~1200 to 7000, so that customers can repay via debit cards and online wallets.

Overall feeling that I got from the call that management was cautiously optimistic, acknowledging that impact has not been that bad but refusing to promise or commit to any drastic improvement in performance.

Long term investors should welcome and hope for further correction in Bajaj Finance share price. Market hasn’t given any entry point for a long time as business is simple and understandable and execution is flawless.

one school of thought is that now that banks are flush with cash, they will get into retail lending and thus may compete with companies like bajaj finance etc.any thoughts on this aspect.invested in bajaj fn

Bajaj Finance was never a play on lesser interest rate than banks. It was a play on its reach and in ease of sanctioning loans. .

Disc. After correction it forms 10% of my portfolio

We keep hearing these stories about the banks now and then. The basic thing is distribution network , feet on street, organization capability and reaction speed.Very few banks have these qualities.So I would not worry too much.

He said they consciously slowed down even before demonetization because there was stress in the economy. I take it as stress in their portfolio. If there was stress in the portfolio before Nov 8, it must have gotten worse after that. They are down to a reasonable growth number now. We will know what is that number when earnings come out. Hopefully it is still 2 digits.

The MD had mentioned about this on the conf call for Q2 earnings. He said that they “anticipate” stress in their CD portfolio and hence they will consciously remove the pedal from the accelerator for Q3. Since CD loans are short term loans(< 1 year), in the MD’s own words - “All the bad cholestorol gets drained in 1-2 quarters”. Remember that they had not actually experienced stress, they just anticipated it to happen.