@jamit05 - Look for Working Capital Days. (I think you were asking for this, going by my very limited hindi skills)

![]()

@jamit05 - Look for Working Capital Days. (I think you were asking for this, going by my very limited hindi skills)

![]()

Mucho Thanks…

Does it mean that any company with working capital days of 20 has a fair chance of trading at a 100-multiple.

And how’s that Havells has

100 is justified or not, many things I dont understand. But I know one thing that the company with increasing ROE always quote at high valuation than static ROE.

Suppose company has 10%ROE.so it earns 10 on Rs 100 and can grow at 10% only without taking money from market. Now capital is 110. Next year ROE is 11% i.e. the profit Rs 12.1. The profit growth is 20.1%, enough to drag PE component down in valuation.

Dmart has to see its steep hikie in ROE as per many parameters. So this high PE may be Illusive.

I am invested here because it is new, growing, efficient and great business irrespective of valuations. It will fullfill my low expetations of return safely.

The idea is to try an understand why some businesses naturally are valued higher because they operate differently. Operating cycle is one reason from amongst a host of other reasons. A negative cycle means that the business doesn’t need to invest in working capital to grow. If there are no growth prospects or the business is not growing for some reason or the other - a good operating cycle will not come to the rescue. For queries regarding havell, request is to post in the appropriate thread if it exists.

Aap ne Hindi likhne ka kasht kiya, uske liye dhanyavaad. Ab aap thoda google kijiye - waha aap ke sawalo ke jawaab mil jayenge. P/e ki duniya se bahar aa jaiye aur dhande ki duniya me aaiye

Best

Bheeshma

I too dont know if the current PE is justified. But we can look at it this way. It has a consistent track record and it at least has a PE < 100. In retail, most of the listed/unlisted players are loss making and dont even have a PE. Even Trent and shoppers stop with not so good track record and return ratios ( Thought the business is not comparable) have a high PE. Amazon didn’t have a PE for a long time, and when it had one it was meaningless. ( oever 500 or something) . I dont think people use PE for valuing retail companies. ( Even in M&A deals, I doubt PE is used)

Having said that, I wonder why damani sold it at 40 PE during the IPO. And he is one of the smartest investors. This is kind of confusing.

You can refer to Prof Bakshi’s blog post on what determines the PE of a stock. The key variables being Growth, its Predictability and Longevity and Free cash generation.

More than guaging the valuation of a share from its PE, it is far better to arrive at value by estimating future profits of a business and then estimating the present value as available and applicable to the shareholder.

There can be businesses available at a high PE but which offer far more value than a business languishing at low PEs due to some serious problems.

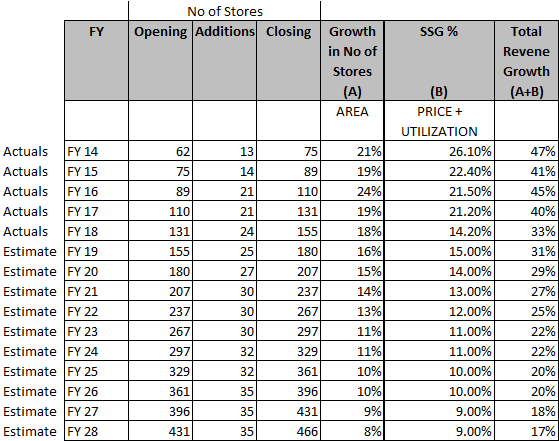

I believe Dmart has a very good probability of growing Revenue at 20-25% CAGR for the next decade. Sharing my calculations below:

Usually I like to break down revenue growth into volume growth + price growth. However for a Retailer like Dmart, it becomes relevant to further break down volume growth into Store Area growth and Store Utilization Growth.

1) Store additions - can grow in line with management guidance but pace of additions will certainly fall. What is interesting to note that even if Dmart reaches 450-500 stores in FY28 which is 10 years from now, its store count would still be lower that 2018 store count of many other competitors like Reliance Fresh, More.

2) Price - Safe to assume price would grow in line with inflation

3) Utilization - This is the most interesting variable. In fact there are so many smaller variables in this for eg,

a) When per capita income increases,

b) What is the capacity constraint in a Retail store ? - Is it the space? no if billing counters? working hours ? As the density of population in cities increases, what is the increase in no of people buying from a an average retail store ?

c) What if the product mix increases from the low margin Food groceries to the higher margin discretionary spend items like apparels, footwear, home furnishings?

Dmart till now has been extremely successful in driving growth of stores through higher utilization. The SSG is a combination of the price growth and the utiIization growth. I would not bet for the SSG rate dropping to inflation rate immediately due to the many tailwinds in favour of utilization growth such as increasing per capita income, increasing urbanization, younger population etc.

Now if you observe, in the above calculation, the Revenue growth can grow at a CAGR of 23% for the next 10 years. Safe to assume that Cash Profits can grow at a rate of 200 bps higher than Revenue CAGR due to economies of scale, deleveraging etc. which would make it ~25% CAGR.

Coming to requirement of funds to source this capex, in FY 18 when it added 24 stores, the capex was ~ 850 crores, whereas the cash profit was ~ 940 crores. As the pace of additions of new stores reduces, it seems that the cash profits of Dmart shall be sufficient to meet the capex of store additions as well as provide for incremental working capital. In fact post debt repayment, Dmart would start generating free cash which it can distribute to its shareholders.

How many businesses can grow its profits at a CAGR of ~25% for the next decade with the same probability as a Dmart? To my mind there isnt any Non-Financial Stock in the Indian Listed Universe which can do that (If you find any, please let me know ![]() )

)

Ofcourse its easy to make 10 year projections in a spreadsheet when no one knows what the reality would be. It could turn out that my estimates are completely wrong and foolish.

Then again, I believe Investing is about taking a leap of faith and with every style of investing and every stock, there will be some degree of risk and uncertainty.

Stock markets work like a discounting machine and once the good things are known, it usually gets discounted in the price.

If one can provide data and logic that can challenge the above, at least some of us on this website would be able to learn from it and augment our investment logic, knowledge and wisdom.

One would be naive if he tried to arrive at the valuation number with this ratio of PE.

One would fail as an investor in the long term, if be bought too high or bought a bad company.

Some financial ratios (cash flow, fcf, roe, RoCE debt etc) give us a glimpse into whether the company bad.

The good ones are often expensive, especially when Nifty is bullish. Comes in PE ratio.

Inverse the PE ratio, and u get the earning power. It is an important number as it tells you exactly what to expect from your investment. For ex. If I bought HUL, i would have to wait 20+ years to get returns just as good as ONGC is giving now! Am I prepared for it?

Simple analysis raises such important questions.

Coming to DMart. I do not understand the business dynamics. The brand and numbers are good, but the cost is high. A healthy correction in it’s prices will not be ignored.

What makes an investment successful is buying good companies at a reasonable rate, preferably cheap. But, if you are paying a high price then you have already lost half the battle at the word go. Post which, the company’s fundamentals could deteriorate or normalize due to it’s growing size or the market could correct in general.

We have all seen this rigamarole unfold several times in the past.

There is no doubt about the company and the promoter running the business. The main debate is all about the Valuations. Below is a piece of writings by one esteemed boarder @basumallick in Page Industries forum which i believe is relevant for here too. I have edited a little part in his posts.

The entire thesis and point of discussion seem to be that if institutions/individuals are paying a very high PE, therefore the company deserves it and it will sustain. This is grossly incorrect. Overvaluation persists for a time period, sometimes years, because of many years. And when the overvaluation bubble bursts, it takes years for the stock price to get back to previous levels.

Take a look at the stock of Microsoft, a great company, which took 16 years to get back to levels seen in 2000 during the dotcom boom. P&G US, arguably the biggest FMCG company in the world, took 5 years to recoup its 2000 highs, then another 5 years to get back to its 2008 highs. Similarly, it took Colgate-Palmolive 7 years to break out of its 2000 highs. Look at Infosys and other tech companies which uses to trade at extremely high PE during dot com boom. Look at those Real State Players which were trading at very high valuations during 2007-08 . All have cooled down sooner or Later.

The simple point is paying too high a price is a recipe for disaster. Stocks, over 100 years of traded history, have NOT sustained at an extremely high PE for very long. Mean reversion inevitably happens and moderates the price. It can happen today, tomorrow or it may not happen in the next 1 year. The timing is not predictable. But what is sure is it will happen. The higher the price paid, the more the pain in store.

The rational thing to do is to side-step such extremely expensive companies or if one is compelled for some reason to buy it, to have a low allocation. There are 5000 odd companies traded in India. We don’t need more than 20 good stocks in our portfolios.

If one is absolutely not able to find 10-20 good stocks which one understands and is available at reasonable valuations, then it is better to stay in cash / debt funds, and start expanding one’s circle of competence. Unless the market is at a peak, there is usually always some good opportunities lurking behind in the shadows. You just need to keep doing the hard work of going over many many companies to find the right one. Buying the defensives at ultra high valuations is taking the easy (read, lazy ) way of investing.

@basumallick ignored that Growth is an important part along with quality .Quality gives capital protection and Growth gives the return . Valuation is matter of debate . Who have more than 3+ years of investment horizon ,he will consider dmart,page gruh etc type of company else he need to look out for cheap ,non quality stuff where he might get return for some time but there is also full possibility of capital erosion of 60% from 52 week high(ex. Edelweiss.) etc

Page Ind gave 25% CAGR Return in past 3 years despite staying in 90 PE 3 years ago. Genomal’s assurance with 20% growth with 20% Margin for next 20 years is more comfortable to me than XYZ value investor and so called Analysts. Over Analyzing for some companies are injurious to wealth .

Investment return depends on exit multiple which Mr. market will give over time. If we see current quality consumer/retail stock they are quoting at 50-60 PE and if we assume Dmart will get similar kind of valuation 15-20 years later then it’s very good investment. People give analogy of Infosys ,How much return infosys has given in last 18 years and so ?. Infosys was quoting at 300 P/E not 100 P/E . Current Infosys P/E is 16.5. What if infosys were a consumer company like (Britannia, Nestle, Asian paint etc). It would be easily getting PE of 50-60 by mr. market in 2018 .Imagine, someone had invested in Infosys in 2000 at 100 P/E not in 300 PE and exit P/E of 50-60 .Investment return would have been very different.

I would be more concerned about how much opportunity size is there for dmart to grow for next 20 years. Can it grow at 20-22% for next 20 years ?. If it can do that it will turn out to be multibegger from here also. There are handful of quality stocks available in the indian market and Dmart is one of them.

Sanjay Bakshi has written very good article about this in 2013.

Technological evolution which requires changes at organisational level are more disruptive. Machine learning is that kind of change, it enables one program to do the task which was performed manually by people earlier, now the challenge has shifted to developing such programs than managing low skilled people.

E-commerce, as per my belief, will not require a retail chain to change it’s existing organisation. It will require developing parallel infrastructure, which is not disruptive in the same manner as machine learning is to IT.

Large Mature dividend paying Consumer cos like Coca Cola and P&G should generally trade at p/e of 20 or thereabouts. In times of irrational exuberance they may well exceed this which is a case of extreme overvaluation that doesn’t end well for investors.

I had a look at the P&G 2000 AR after the post to check its financials,p/e and commentary.

What i found is they had a tough year as highlighted in the AR below, its Return on Capital employed was 17.7% and they paid out 50% of earnings as dividend. They also has a D/E of 1:1. The p/e at this point was 42.

http://www.pginvestor.com/Cache/1001181137.PDF?O=PDF&T=&Y=&D=&FID=1001181137&iid=4004124

Similarly, Coca Cola p/e fluctuated between 50 - 100 pe in 2000

Its financials were also similar. A ROC of 16%/ROE of 23% and 3/4th of income paid out as dividends.

http://people.stern.nyu.edu/jbilders/Pdf/2001Cocacola.pdf

As Dmart becomes mature over time most certainly it too will trade at moderate multiples of 20 or thereabouts.

However, during its rapid growth phase one really cannot expect those multiples , in which case the rational thing would be to avoid it and look at other cos of similar quality which are exhibiting the same growth numbers and available at less concerning multiples.

Point is, presenting P&G/Coca Cola fall post high PE’s without the supporting financials is just one side of the story.

In one of warren buffets letters, he discusses the violent impact of a revision of growth rates on the valuation w.r.t to network television station. A network station that can grow earnings at 6% in perpetuity when it stops doing that and earnings just bob around a mean, experiences a severe contraction in valuation. That is what will probably happen to d-mart , but in the near-mid term it looks unlikely at this point

Best

Bheeshma

Amazon is going too aggressive… Brick and mortar retail needs to have omni channel strategy to survive the amazon juggernaut!

It appears as though the market quotes really far ahead prices of growth stocks.

If there is a fund buying DMART at 100PE, then at 20% cagr EPS growth it is factoring in next 13 years of growth. In other words, if bought at CMP only after 13 years it’s (projected) EPS will give 10% returns. (Either that, or the Fund house is speculating that the growth will increase further)

This is just amazing.

Therefore, if I intend to be a long term investor, then I should invest at a PE level from where I have visibility of earnings, or just accept it as plain speculation.

On similar lines, Infy has zero growth. I am being conservative. Then with 40Eps, I would buy the stock at only 400, to get 10% earning power.

However for TCS, there is 8% growth, With 73 EPS if I buy at 1200, it will take 6 years to give 10% returns. But at 1900, it will take almost two decades. In that respect DMart and TCS are equally expensive.

That is how intend to sort good managements/companies in order of price-value.

Hi @jamit05

You can refer to Security Analysis where Ben Graham explains investing in growth cos and the pitfalls, pros and cons. In general, it is the recommended advice that one pays little or nothing for the growth component from an investing point of view.

No point agonizing over valuations. One can revisit it later when one is comfortable.

Best

Bheeshma

Dmart has started issuing Commercial Papers frequently to obtain funds to meet short-term debt obligations. Board had approved raising the limit from 200 Cr to 500 Cr on 29th Oct’18 & last 2 months have seen company utilizing it for 100 Cr each, where maturity dates are approx 3 months. Does it mean that company is in dire needs of funds for aggressive expansion / run its day to day operations? Despite having good PAT in each quarter, they are opting for frequent commercial papers.

Do they disclose the utilization of such funds in annual reports? Just being cautious on hearing a different company utilizing huge amount (approx 2200 Cr) for advance / loan to its employees

Is “Exclusive DMart Ready Deals” section new on the Dmart Ready website : https://www.dmart.in/

?

Also something to mention is the pickup points.

Can’t resist saying the website is very likeable now as compared to before.

Big Bazaar is aggressively pushing prices against Dmart now a days. Our local dmart employees were saying they can feel a reduction in the number of shoppers visiting Dmart. KB is taking Dmart head to head but I don’t see it benefiting him as he don’t have the cost advantage of Dmart but I am sure that he will not let Dmart grow at aggressive pace like before by pushing the prices. Big Bazaar is also going aggressive with their cards and future pay based offers in the store. Smart shoppers are moving towards Big Bazaar Profit Club Cards and planning how to shop in advance now a days. I had written a post a month back how Big Bazaar Profit Club Cards is a better deal compared to Dmart. https://www.desidime.com/forums/hot-deals-online/topics/10-cb-on-big-bazaar-gift-vouchers-hurry?page=2#post_5412406

They are also giving free shopping every year. This is the second time they have added free shopping benefit in a few months. I have got rs. 400 x 6 cards = rs 2400 worth of free shopping improving the ROI further. https://www.desidime.com/forums/hot-deals-online/topics/big-bazaar-profit-club-will-add-free-shopping-worth-rs-200-to-your-card-tomorrow

I am sure Fretail is making losses by going aggressive but this will surely stop Dmart from growing at the high rate. I think we are looking at a significant de-rating of the dmart stock just like Shankara in the coming times.

@bhisham @anon35913099 @jamit05 @mrai74 @basumallick After Amazon’s intent to enter into offline model - What are the odds of Dmart doing a strategic partnership with ABC Player who is eyeing Indian market? With this partnership the now and then requirement of funds for expansion would also be taken care of + with this Dmart and ABC player would be ready with full ammo to take on Amazon + BB.

Disc. These are just personal hypothesis - but thinking on these lines can provide different paradigm to dmart shares.