Yes, they look likely to close 2019 with an operating margin of ~9%. They have added one more store taking the count to 161 I think in belgavi, belgaum. The next logical cluster would be goa as they have some stores in kolhapur and now 2 in belgaum. Goa has a good per capita income so maybe we should see some store openings there in future. Just speculating though. There is already a Vishal Mega Mart there which is doing well

Not pun intended, but I never visit D-Mart for buying anything. I always do my shopping from Big Bazaar. The reason is D-Mart is very overcrowded everytime. Long queues for taking trolleys and high rush in all alleys. Big Bazaar has less rush and I pretty much get everything there that I can get in D-Mart maybe few things more which aren’t available in D-Mart. This is just an observation and nothing to say against D-Mart. Actually this is good news for D-Mart. But there is a very small trend that a bit more affluent people or who do not care too much about discounts and low prices prefer comfort. Some friends of mine who do not care about very low prices also do the same thing (visit Big Bazaar vs D-Mart)

Now D-Mart has ensured that there were no long queues at billing counter. They have ensured enough billing counters and it looks good sign for customer satisfaction.

@bheeshma - Just my thought; need your feedback on this.

I am from Ahmedabad, and after our marriage was a regular user of Dmart stores in Ahmedabad -> shifted to Bengaluru and again same trend; for our monthly needs we look at Dmart. However since couple of months we are getting the low/comparable prices from “Grofers” and some times “Amazon Pantry”, so hardly go to Dmart [because no value addition and on top too much crowded and long billing lines].

So my question - Shouldn’t Dmart concentrate on the pockets from where it started, i.e Tier 1 & Tier 2 Cities with a cluster based approach and focus to middle + lower middle class plus nearby stores???

From whatever i know about retail, its control over the supply chain that differentiates successful retailers from the rest of the pack.

If SKUs not available at the right time, right place, the right quantity and at the right price everything just unravels over time. Control over the the first 3 determines the 4th i.e the right price. And the price determines the customer group you want to target.

After Grofers moved from the inventory model to the hyper local , the control over its supply chain has diminished and that poses a threat to its business model as you cant offer low prices on a consistent basis if you have limited control over the supply chain.

Big Basket on the other hand, follows the inventory model and has been able to scale up rapidly however it cant offer low prices and that has informed its customer targeting.

Till such time India follows the MRP ( Maximum Retail Price) system over the MSRP ( Maximum suggested Retail Price) system, everybody intending to sell grocery will have to compete within the pricing boundaries

Online grocers are trying out various ways however till they establish some predictability in their sourcing and distribution , its going to be tough for them to offer low prices in perpetuity in a low margin business like Retail.

Over time i think, Retail will become more fragmented as a lot of business models will emerge in response to unique customer groups.

Just wanted to say that on certain dates and on certain cards, Big Basket is very cheap, you can get flat 20% off and home delivery, of course.

I am sure they make losses on those orders, so may not be sustainable though.

Very True! in fact one of a very new shop in our locality has an offer to match D’mart prices on every product along with home delivery. It has been more than a year I have visited any D’mart store. Bad traffic, rising fuel prices, increased actions on wrong parking etc doesn’t make lot of sense to step out for groceries. I use Big Basket for 90% of grocery purchases.

I was talking to a senior marketing guy in an FMCG company who said that all other retail chains complain and demand similar margins as it is being offered to Dmart. Pulls and pressure continue as D’mart refuses to accept unproven product on its shelves but BigBazar is ok. Any new FMCG comapny which wants to enter new categories is more receptive to Big Bazaar’s demands but older ones simply love working with D’mart since volumes are quite high. He was quite clear that D’mart passes most of these discounts to its customers and makes more money from bulk commodities i.e. suger, rice pulses etc which they sell under store brand.

The sales growth which we are witnessing due to increase in store timings along with decrease in product price. Reduction in price can’t be the only reason for this 39% revenue growth . Because Revenue is basically Volume * Price . So if we assume product price decreased 5-10% then volume should also need to increase excessively to match this 39% revenue growth , which is less probable .

If above point no. 1 is true then it need to be watched out How Revenue growth will take place from next year on wards. In my view then new stores which are coming up in past and current years will start contributing the next phase of growth. Management’s smart move is also require to hold up this growth rate.

Old stores already reached in peak utilization rate . We cannot expect more than 6-7% SSG from those stores. DMART ready can be utilized to boost up the revenue growth from those saturated stores.

Last but not the least , decreasing revenue growth was a matter of worry in past year, But returning to 30% + Rev growth from that 22% plus Rev growth is definitely a relief for the long term shareholder of Dmart . We need to be watchful that this continuity of sales growth rate should come without decreasing margin in future. .

In future, whenever you use your valuation model to justify any valuations…do quote its success ratio(as a disclaimer)…how many times it has worked fore you and how many times it hasn’t worked for you… Getting comments removed of someone asking for it doesn’t help any stakeholder… Don’t worry from being shot down - its only the people who challenge you would force you to improve and create a better model - and ultimately that should be your goal - that would be ultimate win.

Don’t be thankful to them who removed those posts and angry about who argued with you. Who argued they tried to do good to you .

We all are in stock market to mint money and keep the profit with us,not to win the argument ,not to increase the twitter followers, not to increase the likes in our post . Making money is more important than wining Argument and those nursery things.

For queries regarding valuation models my request would be to post in the authors thread for the same unless it is in the context of Dmart.

Different investors have different approaches to valuation.

However, the basic funda is that the true value of a co is equal to the discounted value of all the cash that can be taken out from the company.

In the context of retail which is well known globally to have bad economics whether its online or offline and is a cash guzzler in general one must be wary of high multiples. However, in the event we have a retail operation so well run that it generates cash instead of guzzling it over time, the case may be different. Its unlikely but not impossible and where Dmart fits is anyone’s guess.

Cash guzzling businesses in my view have two important commonalities- customer satisfaction is critical and customers have many options to switch over without incurring switching costs. Telecom, hotels , airlines , retail , restaurants etc are all examples of sectors where customer satisfaction plays a central role and dissatisfied customers just switch easily.

May be not. We will leapfrog to e-commerce very rapidly. Remember land line phones, before if took off in India mobiles exploded. Before, people could access internet on PC and laptop, mobile broadband became all pervasive.

Avenue Supermart is trading at PE of 100. The only reason I see why market is paying such a high multiple is the sales growth which is around 25%. Other companies have much better number for ROE, OPM and management quality, but are trading at less than half the PE.

Now its ROE is fairly average at around 18%, this will not be enough to fund the 25% growth in sales. So either the sales growth reduces or they go for the second option, i.e. borrow from public or institutions. Either way the PE of 100 will not sustain.

Therefore, I believe the stock is bound to see a correction in its PE multiple.

At PE 40 and three year forward EPS of around 20, the fair price comes to around Rs.800 a pop, which only a bear market can bring.

WB exited Walmart due to growth concerns, competive pressure of amazon. But he also didnot invest in amazon, as its run up too much too soon. So one lesson, exit underperformer and avoid over expensive.

Now coming to India, we have dmart but we don’t have flipkart listed. So we investors don’t have much choices of high quality business.As a result Excess investable household savings, is gushing into few quality stocks via MF.

No doubt dmart is a great business, but valuations are seldom rationale due to many factors…

One of the key challenges for Dmart is customers opting online options, but as per the report although sales are growing at rapid pace but it has major contribution from devices / gadgets which are non-core for our company.

I beg to differ that Flipkart is a quality business. And D-Mart can not be compared wit Walmart since 80% of D-Mart business is coming from consumer staples , to some extend you can compare this with Costco except the fact that it is a wholesaler. Costco and D-Mart is having a lot of similarity. And don’t forget the industry in US is already saturated on the contrary in India this industry is yet to mature so it is quite obvious that D-Mart will command this kind of valuation as of now unless there are some drastic events.

One clue to your q/s can be found in the additional working capital requirements that are required to fund its growth.

Dmart has an unusually low operating cycle of ~20 days. This means that working capital requirements are 5.48% of the topline ( 20/365)

If Dmart wants achieves a sales growth of 25%, then the additional working capital requirement is 25%*5.48% i.e 1.37% of the previous years topline. Stated differently, it requires an additional working caoital @1.37% of topline to grow by 25%. This is a very advantageous situation to be in esp in retail where working capital is an important factor.

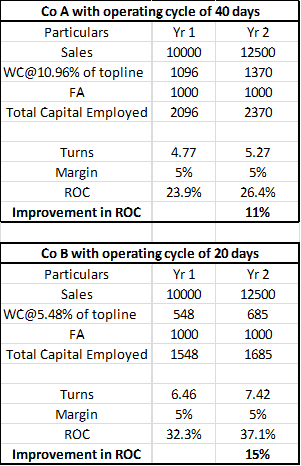

Consider the hypothetical example of 2 cos, one like Dmart with a operating cycle of 20 days and another one with an operating cycle of 40 days with same amount of investments in fixed assets, the same margin profile and the same sales growth.

A 25% sales growth will have a disproportionate impact on the the ROC. Co A (the one with the higher operating cycle ) - will improve its ROC by 11% over last year, while Co B (the one with the 20 day cycle ) will improve its ROC by 15%.

Both the cos have exactly the same growth prospects but because they have different operating cycles one gets valued higher than the other.