Yes, it may be a one off qtr for waterbase as far as margins are concerned. But still good performance

2 Likes

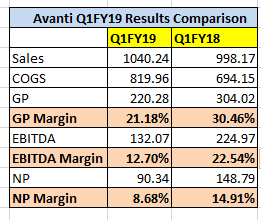

Quarterly results:

Considering industry headwinds since early this year, glad to see flattish overall Q1 revenue. Good chance that there has been increase in volume with lower realization for Shrimp Processing segment because of lower shrimp prices. Not surprised by lower margins and we should consider this as new normal margins.

Disc: invested

19 Likes

Except High Raw material costs the results are satisfactory. I would not compare the results yoy as 2017 period was exceptional year. EBIDTA margin has dipped marginally from last quarter which suggest competition on margins to keep the market share for the end product. I will compare yoy on revenue growth due to seasonality and here avanti showed 4% growth which again suggest competition from other countries. This is a new normal for Avanti and Stock price should follow the new normal.

Disc: One of the top holdings in pf. Continue to hold post this result in near term.

2 Likes

2017 was exceptional , but if we consider the results with June 2016 quarter , how do they look like. Is their a improvement ?

1 Like

US imports reduced 2 months in a row n India’s first yoy decline in 2 years

Indian government increased import duty on Artemia, live feed used in hatcheries.

Avanti acquired 5% stake in a Indonesian venture owned by its Thai partner.

3 Likes

AGM happened on 7th August. Can someone please share the AGM minutes .

AGM Notes

Attaching the Chairman’s address below followed by some of the key points highlighted during the discussions with the management. Note that I may have missed to jot down some other intricacies or details. As a disclosure, Avanti Feeds forms a large chunk of my portfolio and this was my first ever AGM of any company (seek your pardon if the writeup appears novice).

-

Last year was an abnormal year due to reduced prices of inputs, and that lead to inflated margins for the company. As a result, many farmers extrapolated this and jumped into the euphoria of shrimp cultivation, leading to oversupply in the market. This was aggravated due to a prolonged winter in the US, with snow storms on the east coast that lasted till March. This had a natural impact on consumption (if you can’t go out to eat in a snow storm, the demand would be impacted).

-

Mr. Alluri stressed many times that from his 25 years of experience in the industry, margins of 10-12% for feed and 7-10% for processing should be considered normal and sustainable. Any deviation is an anomaly. He did state this many times during earlier interactions with investors as well.

-

In a tough market environment which hasn’t grown in the last few months, Avanti’s market share has gone up to 46-47%. Mr Alluri made it very clear that they are not going to go for market share by selling on credit. Financial discipline is of prime importance.

-

Avanti’s FCR is 1:1.2 while for competitors it is 1:1.5 on average.

-

Out of the total capacity of 22k tons for processing, around 50-60% is being utilized currently.

-

Consumption in the US has resumed after the extended winter and is nearing the usual levels.

-

The company has made a small investment with Thai Union in the Indonesian shrimp feed market. The company is also looking to expand in the neighbouring markets of Bangladesh and Sri Lanka. The conditions etc are similar to India and this can be seen as a natural extension of the Indian market. The market size would be roughly 1.5lac tons, of which Avanti is aiming for 50k tons.

-

China market is opening up. The import duties have been reduced from 18% to 6%. Earlier, China used to a net exporter of shrimp, now it’s becoming a net importer. Thai Union has a presence in China and Avanti would be leveraging that.

-

Globally, most shrimp feed companies have margins in the range of 4-5%, but Indian companies have a cost advantage due to which you see better margins. This, along with other cost efficiencies are the reason India should continue to be significant in this market going forward.

-

Competition: competitors have been always there in the market, nothing new. Cargill has been around for 15 years and they focus mainly on fish feed (same with Nutreco). The main competitor in India remains CP. From a global point of view, overseas competition for Indian exports is there, but it was interesting to know that in Thailand, though their export numbers are not very high, there total production numbers are not low and it’s going for their domestic consumption.

-

Management is exploring options in producing fish feed. Mr Alluri mentioned that in India, cheaper fish (Rs 60-70/kg) is the one that has max demand, the others are priced higher (Rs 400/kg) and would not see that much demand. So if the company does enter fish feed, it’ll not be for domestic consumption. Also, getting into fish feed is not a big technical challenge for a shrimp feed producer. The existing technology can be used with a few minor modifications.

-

Entry barrier in shrimp processing is not that high now, but getting the quality checks, having the traceability and USFDA approvals are the critical bits.

-

Mr Alluri mentioned that what used to be called value added products earlier (in shrimp processing, like, ready to cook) are slowly getting commoditized (I guess it happens in most industries sooner or later), but it was good to see the honest admission. There are still a few areas where there is serious value addition and the company seems to be aligned in that direction.

-

It was encouraging to see Mr Alluri’s sons present there and they seem to be picking up the nuances of running the business. I talked to one of his sons, he mentioned about how the company’s relationship with the farmer is getting stronger. Overall, it was encouraging.

-

Thai Union’s investment arm has recently sold a minor stake in Avanti (as was disclosed on the stock exchange). Their mandate (from the Thai company) is to maintain the net holding between 20-25%. So they may sell more, may not. No one knows.

Overall, a good experience attending the AGM. Worth taking an early morning flight to Vizag and back.

56 Likes

Hi All,

Avanti’s corporate film.

Regards,

Yogansh Jeswani

14 Likes

Very good notes from Arpit. I think he has covered all the major points.

It’s always good to go to this AGM and interact with the management. They seem grounded and talk sense. The presence of people from Thai Union is also very strong (almost 3-4 people sit on the stage with management).

On the negative - the company earlier kept guiding for 4.9 or 5 lac tonne volume however it seems they may be able to do volumes something similar to last year or may be about 4.5 lac tonne. As per discussions, it seems that things were ok till may be May end or June end but as the low prices continued for 4-5 months, it was not very remunerative for farmers and a lot of them didn’t go for farming in the months of July and August. The second crop has started on a weak note and the culture may be down 15-20%+. The positive is that due to this, the shrimp prices have now started going up in India and they expect farmers to come back to farming (but from Nov it would be winters so one needs to see how many can come back quickly).

Mr. Indra shared that there was lot of greed in the industry over last 2-3 years due to very high growth and profits being made and hence the farmers who took expensive leases may not come back soon. However all this is positive for the long term and sustainability of the industry.

Processing cos have made very good margins in Q1 but now prices have increased more than international prices in India so the margins should normalise going forward.

32 Likes

Indian shrimp prices rising fast as packers fight for raw material

By Tom Seaman Aug. 15, 2018 09:26 BST

India shrimp processing

A

A

Comment

The prices for vannamei shrimp raw material in India are moving up fast.

Processors are fighting for reduced levels of raw material to fulfill orders, after farmers reduced stocking due to disease issues and the weak market, sources told Undercurrent News.

Prices for Indian raw material in week 32 (Aug. 6-12) are up 17-24% since week 28, when they seemed to have bottomed out, according to the Undercurrent prices portal. Meanwhile, prices for raw material in Vietnam – which have just been added to the portal – Thailand, and China are all fairly stable, as can be seen on the portal.

Prices for 50 count per kilogram of raw material have risen the fastest, increasing 24% from week 28 to INR 273 ($3.88)/kg. Prices for 30 and 80 count sizes were the slowest risers, increasing 17% from week 28 to INR 393 ($5.59) and INR 223 ($3.17), respectively.

“Big processors are struggling to complete orders and delays, maybe major, are now anticipated. New offers from processors are now scarce,” said Jim Gulkin, managing director of Siam Canadian Group, a Bangkok, Thailand-based, pan-Asian frozen seafood supplier with an office in India.

“Raw material shortages will continue through at least October and perhaps through year-end,” he told Undercurrent.

According to Gulkin, big processors in Andhra Pradesh, the main state for Indian shrimp farming, as well as packers in other areas, “are racing to complete major year-end sales orders against rapidly-declining raw material availability”.

READ ALSO

EU suspends free trade talks with Thailand

Shrimp price analysis: Some India sizes almost $2/kg cheaper than Thailand

The big processors in Andhra Pradesh, “most of whom have major orders still on the books, are buying raw material from Odisha and Gujarat to make up for the current shortfall” in their home state, he told Undercurrent.

Andhra Pradesh’s first major crop “is pretty much exhausted”, he said.

“Many packers still have pending orders for August and September ETDs [estimated time of departure],” said an Indian shrimp sector executive (source A), who preferred not to be named.

Durai Murugan Balasubramanian, secretary of the Pattukottai Shrimp Farmers Association in Tamil Nadu, also said there is “strong competition” among exporters to secure the last available raw material.

“My sources are telling [me] prices likely to bounce [to] strong levels in coming weeks,” he told Undercurrent. “The raw material availability in Andhra [Pradesh] has gone very low.”

The stocking suffered from severe “vibriosis and white spot” issues, he said.

Also, most farmers suffered from high feed conversion ratios due to white feces, another disease. This has meant many have switched to farming fish, claimed Balasubramanian.

“Going back to April/May, farmers began reducing pond re-seeding in terms of area, the number of ponds re-seeded as well as stocking density. This was widely anticipated due to stubbornly low prices and tepid demand. Hatchery sales dropped drastically and hatcheries tried to move product by offering farmers substantially reduced pricing. Many hatcheries temporarily closed down at that time,” Gulkin told Undercurrent.

“There has been a drastic drop in raw material arrivals as farmers recently stayed away stocking for the new crop, due to the low prices and high disease risks. There have also been reports of white spot disease in many shrimp farming regions that caused high mortalities,” said source A.

13 Likes

Yes, as per my discussions with some industry people, in recent weeks there has been a substantial price increase in Indian markets (the global prices are still weak). The same reflects two things 1. The farming in 2nd crop has been very low and hence a demand supply mis-match. The current good prices should lure the farmers to come back 2. The long terms prospects of industry remain good if these prices sustain

13 Likes

q1 fy19 IR

the company says the shrimp feed industry good see a degrowth of 10-15 % in FY 19 ; however the company is confident of maintaining a flattish year in terms of volume of feed( confident of increasing market share from 43 % to 47 % overall)

shrimp hatchery commercial production estimated by early 2019

even though the shrimp prices fell by 15-20 % in q1 , exportd from india have increased in vol terms

company still maintaing its vision to become 1 billion USD company till 2022, that would be roughly 17-18 % topline CAGR.

Keep watching the soybean prices. Already 7 - 8 % off their highs this year. And we just heard that the domestic shrimp prices are going up due to less supply. Keep watching the input and output prices and input and output demand and supply.

https://www.outlookindia.com/newsscroll/soybean-futures-move-down-on-global-cues/1365834

1 Like

Avanti sources Soya meal from India only Today in ET saw, with good rain happening in MP, Soya production expected to be good, that will cool down the domestic price. Because of Trade war, International prices already down.

The global shrimp raw material price crash seen in the first half of 2018 is indicative of a “new reality” when it comes to levels going forward, an analyst with Rabobank has said.

The first signs of a price crash were visible in 2017, as supply began to exceed demand and China’s formerly unsatiable appetite eased somewhat, wrote the bank’s associate director for animal proteins and seafood, Gorjan Nikolik, sent to Undercurrent News.

The report – “Keeping up with the Crustaceans” – notes the price crash occurred during the first harvest of 2018, as a result of strong double-digit supply growth from India and Ecuador, though growth was also reported in Indonesia, Vietnam and others.

“Currently, many farmers are harvesting their shrimp at a loss – or at least with a far lower profit margin in the last five years – mainly because the key elements of the cost part of the equation, such as feed, energy, and labor, have not contracted (and for some, have increased).”

He predicted that, in addition to farmers’ protests, the industry’s shrinking profit pool will be redistributed throughout the value chain, with “considerable consequences”.

Nikolik echoed what sources have been telling Undercurrent for much of 2018; that many farmers will reduce stocking for the next shrimp crop, or reduce feeding rates and delay harvests, or simply not stock at all.

“Shrimp farming has a fairly short cycle, and farmers can respond quickly to changes in price, balancing the market within a few months,” he wrote. “However, predicting how farmers in each region will respond to a low-price environment across a number of crops in the next few years is much harder.”

India has just begun to see prices rapidly rising again, as packers compete for limited raw materials. However, Rabobank does not see this as the start of a full recovery.

“In our view, although a mild short-term price recovery is likely, the lower price level, in the absence of a major new disease outbreak, does represent a new reality. A reality in which price levels dictate supply trends even more than biological supply-side challenges; a shift from a supply-driven industry to a more demand-driven one.”

He predicted the main medium-term impact of this would be a decline in the overall profit pool, with farmers bearing the brunt of the contraction. This may discourage new land and new farmers from entering the sector, as well as hitting existing farms.

“Certainly those planning to invest in greenfield operations will reconsider the investments, especially if these investments are high and there are no government development subsidies available.”

He expects capital-intensive recirculating aquaculture system projects to find it even harder to find investors, and large industrial farms under construction to have to reduce profit expectations and even delay scale-up plans. “This is especially true for those projects targeting global export markets, while farms relying on more isolated markets, such as the Middle East or Australia, may be less affected.”

Shrimp raw material prices can be followed at Undercurrent’s prices portal, including recently-added Vietnamese vannemei updates.

Forced Indian consolidation?

While India is likely to see its high supply growth rate of recent years slow, growth should still continue, Rabobank expects. While Andhra Pradesh – which accounts for some 70% of production – is likely to reduce its supply growth to low single digits, new regions such as Gujarat, Odisha and West Bengal can continue the expansion, Nikolik wrote.

Management with firms Nutreco and West Coast Group have already told Undercurrent they anticipate their planned 100,000-metric-ton feed plant in Gujarat will stimulate growth there.

“The newcomers in these regions are not (yet) discouraged by the low shrimp prices, as the biological cost of production in these new regions is very favorable, especially in the first few years of operation, when the new farms are largely pathogen-free,” noted Nikolik.

A lower Indian growth rate will delay or discourage investment throughout the value chain there, he believes. He also predicts the planned feed production growth will mean an over-capacity, leading to new projects being delayed or canceled.

Listed Indian firms active in the shrimp sector have seen their share prices drop in 2018 so far, he added, with over 60% of market capitalization lost. The announced initial public offerings may be delayed, or even canceled. “Perhaps this will lead to the first round of consolidation in the Indian shrimp industry. This could also be an opportunity for foreign investors to increase their presence.”

Ecuador growing

Already one of the world’s key shrimp farming regions, Ecuador has room to grow its output via intensification, wrote Nikolik. The country’s government has pledged to connect 100,000 hectares of farming area (roughly 45% of the total) to the power grid, a move which should aid this development, he said.

This should allow for the use of productivity-increasing equipment, common elsewhere in the world. Industrial Pesquera Santa Priscila, Ecuador’s largest shrimp producer and processor, aims to grow in this manner, it has told Undercurrent.

However, Rabobank noted, more than half of Ecuador’s exports go to China – a high dependence on one market. Much of this goes via Vietnam’s “grey channel”, though China has been cracking down on this of late, and has cut import tariffs from 5% to 2%.

Chinese demand cooling

China – the largest shrimp market in the world – is expected to see a mild recovery in domestic production this year, said Nikolik. This may also continue for the next few years.

At the same time it is cracking down on illegal imports entering China via Vietnam; though tariffs have come down, a shift to legal trade is likely to increase the price of imported shrimp.

“This price may further increase if the Chinese renminbi depreciates against the US dollar, following the trade war with the US,” he said. This same issue could mean some previously-exported Chinese shrimp may need to be sold domestically; overall, net import demand may be set to ease.

“If Chinese import demand weakens we will see a continuation of the low-price period, as China has been the main demand driver in the last five years,” wrote the analyst.

“The lower profitability at farm level means Chinese investors, who are typically long-term-minded, could see the period ahead as an opportunity to acquire shrimp farming assets abroad for a more favorable price.”

Government predictions across Asia are bullish for increased supply, and Rabobank believes at least part of this growth will be realized, given the increasing professionalization in Vietnam and the rising numbers of semi-intensive farmers.

If predictions were all to materialize, the global industry would expand by over 1 million metric tons in the next three to four years. In Vietnam, and in Indonesia, Rabobank sees at least a part of the growth expectations coming to fruition.

Another good article that will encourage Industry level consolidation…push weak players out…in Feed and Shrimp also

3 Likes

Q1FY19 Earnings Conf Call Notes:

Key Takeaways: Shrimp prices have rebounded at farm gate level. Management expecting higher stocking of feed and increased culture for 2nd crop and overall trend moving towards normal levels.

Feed Business & General Business Trend:

• Fishmeal prices 76 to 96.44, Q1FY18 to Q1FY19. Currently at 101. (Mr. Rao was very fast. I may have recorded these numbers incorrectly, please confirm numbers in published transcript)

• Soya from 30 to 38, Q1FY18 to Q1FY19. Currently at 40.3. (Mr. Rao was very fast. I may have recorded these numbers incorrectly, please confirm numbers in published transcript) MSP announced by government is keeping prices firm.

• Feed sales volume for first 6 months for 2018 calendar year is similar to last two financial years’ first six months.

• Domestic farm gate prices are rebounding and more farmers are expected to do shrimp culture for 2nd crop for the year. International shrimp prices have also increased. Situation has changed now at ground level for farmers. Farm gate prices have significantly increased compared to last quarter.

• 4.3lacs MT feed volume was done in FY18. Expecting to do same volume in FY19.

• Current slump is temporary and expecting things to recover in coming year and company is still positive on making it $1bn by 2022 through below points:

o Increased contribution from value added shrimp processing

o 6lakhs MT feed capacity expecting to fully utilize in coming years

o Exploring Fish feed opportunity

• 10 years back similar situation occurred when prices slumped for shrimps and Mr. Rao was giving it as example as how industry rebounded and things normalized in few years.

• Avanti can increase feed price, if farmers are making good money (increase in farm gate prices). Sustainability of farmer is critical for the industry.

• Industry expecting 10-15% degrowth in shrimp exports. Avanti expecting flattish growth for FY19.

• Management expects that area under shrimp culture will continue to increase in future.

Processing & Exports:

• Avanti normally hedges currency exposure as soon as orders are confirmed.

• Other expenses have gone up to around 20% of sales because of mark to mark forex losses.

• Hatchery construction going on. Will take10-12 months to commence. Start with 200mn seeds. CAPEX 6cr and another 6cr for two phases.

• Management takes into the account future prices before quoting for export orders. Avanti confirms exports orders before purchasing shrimps.

• Increasing market share for processing business. Establishing brand in exports market is very difficult. Customers have loyalty to local established brands. Large clients are impressed with new processing facilities of Avanti.

18 Likes

Thank you for the detailed notes. While the long term target of USD 1 bn remains intact, the plan to achieve it is not clear. I personally do not see them achieving it with existing capacities. I believe foray into other segments (like fish feed or value added products into other geographies) may help them achieve the target. While, someone clearly asked the question today on the call, management could not provide a clear answer. Also, it is not clear, what % of their exports are to EU and other countries.I feel these additional markets may provide the company to increase their capacity utilization in processing segment (which they say, will do 11000MT in FY 19). With a capacity of 22000 MT in processing side, I somehow do not understand such low utilization levels. And, have been hearing evaluation of fish feed segment in the last few calls, but no concrete steps to kickstart the process yet. Somehow, I feel the call time of 1 hour is too less (while I registered myself to ask a question, I did not get an opportunity). Most of the time in the call is wasted asking about management guidance on next quarter and there after. Will send across these questions to investor relations team and ask for clarifications. Will keep the forum posted.

8 Likes