It seems its a positive development for industry (rather than as suggested by headlines) as duty has been placed at 1.35% vs 2.34% proposed few months back?

16 Likes

Soyabean prices rising, Shrimp Feed prices staying constant, anti-dumping duty increased. All points to what will be a not so good quarter and year for Avanti Feeds. Will be exiting if stock falls below 400 and rebuy when it has a proper upwards trajectory.

Transcript of Conference call is out

Highlights:

Feed Section

- The feed sales is projected to increase by 10-15% in FY19 over the sales of 430000MT is FY18

- The company is aiming to increase its market share from 43% to 47% in the coming year

- The company will not be increasing the price of Shrimp feed as they dont want to burden the farmers.

- The prices of the Raw materials for the feed i.e Fish meal and soya beans currently is comparable to the prices in FY16-17

- The price of the Fish meal depends on the Fish catches from the sea and it is very dynamic in nature

Shrimp Processing and Export section

- In the Shrimp processing and export section, PBT of 12 to 15% is expected.

- The company is focusing on Value added Products and achieve a minimum of at least 70% of the exports

- The Value added products include “Ready to Cook” and “Ready to Eat”

- The “Ready to Cook” will have lower margins compared to “Ready to Eat” .The range of the Margins will be in between (7% to 15%).

- The company has already started selling “Ready to Cook” . “Ready to Eat” is also being done and it seems some orders are coming.

- The company has started focussing on European countries apart from US

- The orders will be either "On Spot " or Contracts(duration of contracts depends on the market demands and supplies)

The management appeared confident and overall ,the upcoming year will be an average year with PAT in the range of 10 to 15%

Disc:Invested at high levels at 18X PE.Planning to average now

2 Likes

I genuinely believe that most market participants are taking a myopic view towards the company and the industry and these sensationalized headlines dont help much. One needs to assess if the recent slowdown is structural or temporary in nature. Below are my thoughts -

- Current slowdown in demand is temporary and its already witnessing signs of recovery as orders from India have picked up as per channel checks. Decline in shrimp prices has made it a cheaper source of protein and hence the volumes are seeing an uptick in US. Whats very interesting to note is that despite lower demand, India has still managed to show growth in volumes and increase its market share.

- ADD needs to be looked at in context of duties on other countries. In Vietnam its as high as 25% and 10% on China. This gives a clear advantage to India for long term growth. Also lets not ignore the new markets opening up for India like Korea where the duty was reduced from 22% to 0 (https://economictimes.indiatimes.com/news/economy/foreign-trade/yoga-for-taekwondo-shrimp-for-coffee-india-and-korea-expand-trade-pact/articleshow/64941510.cms).

- Soybean production is expected to be 15% higher this year as more farmers have shifted production due to high prices in the second half of last year. This will lead to lower raw material prices in the second half of this year when the season starts.

- Out of total exports, India’s share in value add is just 6-7% while for Vietnam and Thailand its more than 40%. Both Vietnam and Thailand have been struggling lately as can be seen from the export data. This is large market for Indian companies to cater to which leaves enough room for growth.

- SIMP regulations require traceability of shrimps to the pond level. This is a big positive for large 9-10 shrimp processors in India as smaller processors dont have systems in place to implement the requirement.

- Given TUF’s backing, Avanti can easily penetrate into newer markets. For example, China market is opening up for India as mentioned by Indrakumar too in his latest interview. TUF set up its own subsidiary for distribution in China in 2017 to cater to the requirements there.

- Competition in feeds is not new. The supply is 2x the demand in the industry yet Avanti has been able to increase its market share over the last few years. Why should this change now with new players coming in?

- Farmers are not making money issue - This is NOT true. Farmers are not making AS MUCH money as they made last year. They are still making money at current farm gate prices. Only new farmers who bought expensive land are struggling to make money. This is good in a way as it will restrict oversupply.

While I do expect the first half to remain muted especially due to higher base last year, I do not believe there is a structural risk to the industry. One needs to cut through the noise. The company is trading below 14x FY 20 EPS as per my estimates

37 Likes

Isn’t avanti trading below 14x PE FY 2017-18 itself

Not the right base as it was an abnormally good year.

great points @sagararya

can u give a more clearer picture on how u arrived at the FY 20 EPS, in terms of revenue/volume assumed from feed & processing , margins assumed for each segment.

If u have assumed some qty of value added vs normal shrimp please throw light on that also.

Thanks

Management has clarified that there would b volume growth but bottom-line ll b muted. Nonetheless it is probable that Avanti maybe able to meet FY 2018 s bottom-line with increased volume growth

There will surely be a decline in FY 19 profits as compared to FY 18. Have no doubt about it. Expecting anything else will be wishful thinking.

FY 20 will witness growth as capacity ramps up

Broad based assumptions

- Total processing capacity 22000 MTPA. 90% utilization in 20 ; 655 rupees per kg realization in fy 20 which lower than 680 in FY 18 ; ebitda margins at approx 12%

- Total feed capacity of 6lakh, 100% utilization in 20 at 66 per kg (no price change assumed), approx ebitda margins at 13.5%

This should give approx same ebitda as fy18 translating into higher eps due to tax incentives from the new processing plant. The company can do brownfield expansion if the demand rises.

Please do you own diligence. These are just my estimates which could be way off.

2 Likes

Whereas I am not able to mention source immediately ( One is Undercurrent), where I have seen slight price improvement in last 2 weeks of June and USA inventories are getting cleared,but yes- it is early on.

I am sure more news will flow in coming days.

I was also checking one 24 BUSD USA Food distribution giant’s Qtrly Q1 report and they were also mentioning that business got hit last qtr because of Weather issues in USA

I was just wondering what made promoters to buy 5 shares, 25 shares , 35 shares etc…from open market. Are they too worried about share price and just trying to give a moral boost by just showing promoter purchase irrespective of the quantity. Last few months it’s a continuous disposal and recently Thai union also sold off few shares. As i am quite new I always see insider trade also as a parameter to see the movement of stock.

.

PS: Invested before split and now confused whether to sell now and buy later or just hold.

Ya it’s worrisome that for last few months so many announcements, very small buying, Thai union clarification… Looks like management complete focus has shift to share price? Isn’t Management showing sign of nervousness? Any expert opinio

If at all the intention of the promoters was to give a ‘moral boost’ as you said, for sure they would be spending far more than Rs. 2000, Rs. 10000 and Rs. 14000. Buying or selling of insignificant number of shares (in the case of Avanti, looks like 0.16% of shares have been sold by promoter group members in a period over 6 quarters.) shouldn’t be a concern IMO. For all we know, they might have liked to see a nice round number and hence these purchases! ![]()

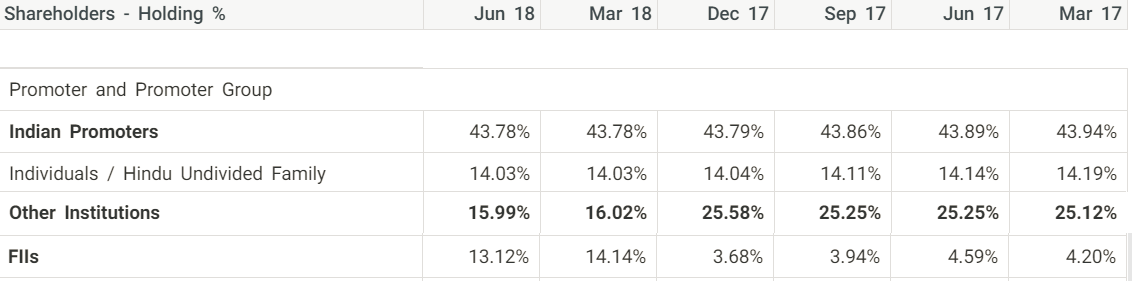

Thai Union reducing its stake significantly should be a concern though. It reduced its stake in Avanti Feeds from 25% to 15%. However, all those shares sold by Thai Union were bought by Thai Union Asia Investment Holdings.

Chart below with data for above comments (Reduction of 9.13% in “Other Institutions” and increase of 8.92% in “FII”):

Thai Union stated that it is committed to consistently maintain its shareholding in the company in a range of 20-25% consistently.

Thai Union’s shareholding in the company has reduced marginally from 24.85% as on March 31, 2018, to 24.75% as on June 30, 2018.

In this thread itself we can see that well-informed members too do seem to get panicky about “stake sale” by Thai Union. So the clarification doesn’t seem to be too out of place now, isn’t it? ![]()

3 Likes

Avanti Feeds still remains a multi bagger. It’s market share is going to increase to more than 55% in feeds sector and to 50% in frozen shrimps exports sector in coming years. Further Avanti is also going for value added products. This precarious situation in shrimp business is a boon for Avanti because this crisis will eliminate the weaker guys from the market and only the fittest will survive. Avanti is the fittest player in this business so there are high chances that Avanti will get more turf to play because of reduced number of players in the shrimp business. This is my first post on this forum. You are welcome for your feedback.

7 Likes

very common sensical first post !!!

Avanti is still a 3 bagger for people who are holding it for last 15 months…

Met one man who used to lease his hatchery for Avanti earlier, says that there is overproduction in AP and other areas and almost 60% of the small farmers have stopped production. Because of the AP govt policy of subsidized electricity and other sops, many farmers were able to make a lot of money last year and they anticipated better times this year and now they are in trouble. The winding up process will take many months as they take loan and buy vannamei species in advance. According to him, if domestic consumption improves it will become lucrative again. He says Avanti has good reputation and it has grown recently because of the support of Thai Union. According to him Avanti is probably bigger than Devi foods. This over production is not going to go away in a haste. It may take an year or so more to stabilize

16 Likes

I am quite amazed by the short nearsightedness of many of the folks in the investment industry. Most of us are trying to interpret each and every news headline and bring some conclusion out of it. As Munger has said - to a man with a hammer everything looks like a nail. If one has a negative opinion on stock, he or she will try to derive negative conclusion from the news and vice-versa.

Rather than focusing on parameters that are beyond one’s control I would try and answer few simple questions that we can answer with certain confidence -

1. To start with, will Avanti survive for next 10 years?

With a certain probability I would say yes. This business has not been built over night. Management has built sustainable competitive advantages around its business by working very closely with the farmers, establishing teams on ground, building capacities and developing strong R&D. This sustainable advantage is getting reflected in its 45%+ RoE, strong balance sheet (huge cash poistion built over years), healthy working capital and a market share of 43% in domestic feeds business. When a player like Godrej Agrovet agrees to Avanti’s strengths it speaks volumes about the business.

How do you see competition from other companies like CP and Avanti?

It is difficult. If you look at Avanti Feeds, it was much smaller some time ago. Today, it is much bigger than [the Thailand headquartered] CP group. This is despite a fall in stock prices for Avanti. Its market capitalisation which was over Rs 12,000 crore is more of an order of Rs 6,000 crore now. The last two years were very good for the Indian shrimp industry as there was problem in Thailand and Vietnam.

Once you are sure about business sustainability with certain confidence, next question is -

2. Do we see sustainability of earnings for next few years with certain probability?

My answer would be yes unless a. people stop eating shrimps globally b. management does something really stupid c. some other country comes up in big way as a shrimp exporter to US and European countries or d. big player in feeds business emerges out of nowhere.

For me I don’t foresee either of a,b,c or d to be happening. People will continue to eat shrimps if not more at least at same pace in worst case scenario. Shrimp processors will need feed. Looking at the past history I don’t see management doing anything stupid. If they have survived through rough patch of pre-2009 era I think they will do reasonably well going forward as well. Vietnam or Thailand might re-emerge as an alternative to India but again its not going to be easy. Plus shrimps from Vietnam has far higher duty than the Indian ones so as to export to US. New competition coming in I find it very tough as elaborated in point 1.

3. It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price. - Warren Buffett

I have no clue how the earnings will shape up this year or next year. I doubt if the promoter can also say this with certainty. I am open to buy a business any day which can grow its earnings at sustained rate of 15% with RoE of 45%. Indian market history shows companies which can grow at sustained pace with reasonably high RoE than cost of capital will always command premium. You can check any of the consumer companies.

I believe if we can answer the above three questions clearly, we can cut through the noise confidently.

Cheers.

27 Likes

During times like these, we tend to see a negative development in a company/industry in a much zoomed out way thanks to our frenzy media and our own instincts prodding us to look out for most plausible cause/effect relationship. Reminds me of Howard Marks quote- pendulum swing won’t stay for too long at the extremes. While, the current fall in price may continue further (due to any correlated/non-correlated events), it definitely may not go on eternally. My two cents about recent developments and way forward-

a) Industry headwinds- fall in demand due to adverse weather conditions in US, oversupply in India (due to small and first time farmers entering the business after looking at lucrative returns over last 1-2 years) led to fall in shrimp prices. Way out- demand uptick in US (which we are slowly witnessing) and other key markets, rise in shrimp prices (again, I verified through some shrimp traders and prices started moving up now). Again, in times like these, I believe, small & marginal feed players will see the major impact, as big farmers tend to stick with larger players like Avanti (due to their sustainable competitive advantage of lower FCR, technical support to farmers etc) .

b) quarterly performance- am not expecting Avanti to repeat Q1, Q2 18 (which were key quarters and Avanti had shown great profits due to benign raw material prices). But, I feel, its better for me to see the bigger picture here (2022 target set by Avanti management to attain USD 1 Bn turnover) rather than mull over immediate quarterly numbers. Do I believe the management to execute their plans and attain their target in next 3-4 years? Yes, based on their track record till date, I trust the management to explore new opportunities to efficiently allocate the capital and generate good returns.

c) media articles vs on the ground situation- I realized, some of the media articles grossly exaggerate on the ground situation and may not truly reflect the accurate picture. Its always better to cross verify by directly talking to industry people, farmers rather than relying on media articles. When, I spoke to traders and farmers, I realized situation is not so gloomy as painted in news articles and well established farmers/intermediaries are well prepared for such adverse operating conditions.

Times like these are extra ordinary, which test our patience and self belief. Very difficult to sit tight and cut all the noise around. Especially, when few large cap stocks are hitting all time high! I realized, no point in pondering over things (like next market move, next quarterly result expectation etc) which are beyond my imagination and control. Personally, I am not adept in identifying the exact bottom of the stock in the current fall and hence have been averaging down, keeping bigger picture in mind. Finally, two things are bound to happen- either I make money or gain experience and hence a win-win situation either ways !!

Disc- Avanti feeds form the largest position in my portfolio and my views are extremely biased. This is not a buy/sell recommendation. Pls do your own due diligence.

15 Likes

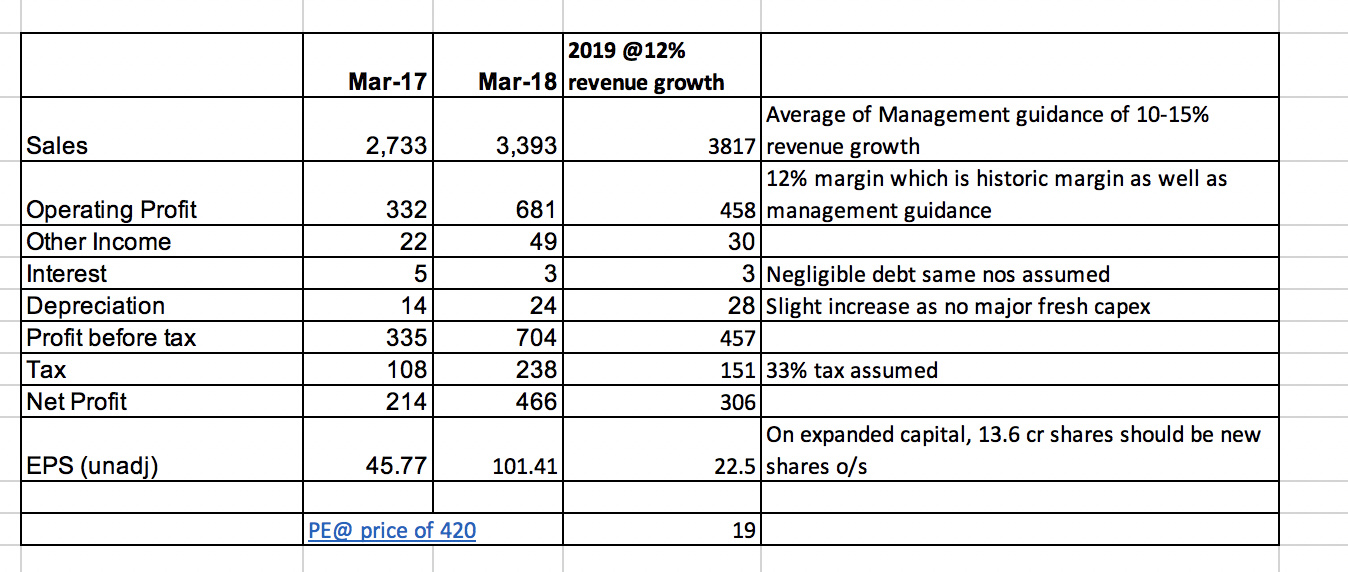

totally agree with the points made by @sagararya@sarmams, broadly we have been spoilt by the exceptional 2018 performance which in no way is the new normal but was an aberration. Have done some back of envelope numbers for 2019.

Even if you look at the projected 2019 profit, which is much lower than 2018 you are looking at 20% CAGR over 2017 which is actually very healthy. It is a fact that stock price had run much ahead of fundamentals, which has now corrected - even today a 2019 PE of 19 is reasonable but not exactly cheap - but that does not take away from the intrinsic advantages of the company or the long term attractiveness of the sector. I think this is a good time to build positions with a 2020 outlook.

Disc - hold a tracking position, looking to add

3 Likes

When I was doing calculation , I also reached to similar expected EPS of 23 for FY 19. However , what I am more bothered is about the PE of 19(@EPS 23). For a commodity industry , is it on higher side , if we assume bear market is coming soon ? Can the market do PE de rating from here ? Last year in optimistic scenario , it crossed 30 PE also. Few years back it was trading around 10-12 PE approx. So can we get those levels also , provided their are various macro and micro factor like interest rates are increasing , anti dumping duty , increased supply , decreased prices and increasing raw material prices etc. ? I am more worried about PE de-rating than earnings concern. Request others to share your views on it,

Disc : Invested

1 Like