Lot of research and work goes on maintaining and improving quality.

We had small capacities in start, but we kept increasing capacity at great quality.

Along with TUF, we are working in new products with reducing fish meal and better FCR.

It cannot happen suddenly, as lot of work is needed and quality is more important than anything

We have been able to reduce the fish meal intake but still working.

March 2018: The 1.75 lac capacity will go commercialisation

Processing plant is complete and in operation and should do commercial production by end of this month.

Requires a lot of permissions as it is food product. HACCP and all permission have been received.

Reasons for growth and increasing market share of Indian shrimp:

Vietnam and Thailand effected by EMS and still recovering

China net importer. This has contributed the most.

Indian quality is better than Ecudor or Indonesian shrimp. Eucoder is just near and gets transport benefits.

India is growing well, new farms are coming up, new areas are coming up. Have huge costal line (only 14-15% used), reached 5lac tonnes. Easier 20-25% growth on 2lac than on 5lac. Cultivation area may grow at 5 or 8%.

Indian companies are focusing on quality. Avanti - Devi and others, we sell directly to customers and this requires lots of certifications and best standards. To supply to wall mart and retail customers.

In India, the companies are taking it seriously. We are working on sustainable model, we want to be reliable partners and top 10 companies are working on it. We as India want to be preferred suppliers.

Things should be good except for unknown external circumstances.

When industry is growing, there are many who run after profits.

We want sustainable model.

We are educating farmers to not use antibiotics. Someone comes and explains them, and they believe it. We meet farmers. AP government has banned use of antibiotics in aquaculture. They should ban the manufacturers of antibiotics.

We did extensive propaganda to not use antibiotics. We showed the dangers of using antibiotics and that they would get good price by not using it. But sometime they cut corners and use them.

We are making representations to CM of AP and other departments. They are conducting village seminars

This is a trade barrier. Europeans want their products to be imported at lower duties in India. This is also a trade negotiation.

Industry has to survive and thus we are working on it. We are part of the team. We are really working.

Farmer is very sensitive to quality of feed.

He puts lac of rupees in farms, he closely monitors daily growths and FCRs. They need quality product.

They put feed in pond water and closely monitor the quality. They too want profits. Avanti’s feed is a pull.

We want our shareholders, our farmers and our employees to be happy.

We diversified into power plants in 2006-07. Not now. That time power sector was cream.

There are half a dozen global feed companies in India.

We are competing against them and able to sustain

Logistics is a problem in export and so is import duties

We are working on small quantities for export.

Fish industry is very large globally. Saloman and all are high value items and they are not here.

We are working on it. So we are focussing on India.

We are also selling to importers as well as retailers. Retailers is 85%.

Sustainability of margins:

Current EBITDA margins are exceptional due to weak RM prices but given the kind of volumes AFL is doing, 15% EBITDA margins in feed may be sustainable ( vs 10-12% in previous years)

If RM price increases, we won’t increase. We can’t change price everyday.

If soya bean goes back to 50, we would have to take the burden.

Others:

Fell short on feed capacity by ~15000 MT in the last quarter. Lost ~Rs 1000mn of sales in the quarter.

Current market share is ~43% and the company is aiming for 50-55% share in next 2 years.

Soloman is a cold water specie. That kind of water and weather is not in India. Similarly, shrimp grows well in warm water. That is the benefit of India.

Red Lobster is a 49% subsidiary of TUF. Chickes of Sea is also 100% subsidiary of TUF. Thus TUF has a huge retail network. We should get good realisations in processing.

For real value addition, the skilled labor is very hard to get. They are not regular and not very passionate. For example, it took 3 years to just get the labor to wear the masks.

Unskilled labor is generally available.

In talk with Finance Head:

There is a very different culture in Avanti. The MD talks to every head multiple times a day. He is aware of all the employees. He would ask us to cautiously develop good team and provide suggestions. He would ask us to let employees go early at-least 2-3 days a week. He sees everything and has developed an amazing culture here.

Both the sons of MD have been developed form bottom. One has got 2 years training in TUF. He is very good in doing international deals and customers. The elder one looks after the operations very closely.

At the AGM we met a head from another major Shrimp processor who was investor in Avanti in personal capacity. It was interesting to talk to him. Notes attached below.

Thank you very much @Donald and @pratyushmittal for the much awaited notes. You folks have been awesome.

It appears TUF - the 55% owner (by virtue of 40% in AFFPL, and 25% in Avanti)

0.4 + (0.25 * 0.4) = 50% right?

Fish industry is very large globally. Saloman and all are high value items and they are not here.

Soloman is a cold water specie. That kind of water and weather is not in India.

Were these points on Salmon made in reference to Avanti’s fishing foray? Have they decided on the breed of fish that they intend to focus on?

Indian companies are focusing on quality. Avanti - Devi and others, we sell directly to customers and this requires lots of certifications and best standards. To supply to wall mart and retail customers.

Devi has been mentioned as the only Indian company to have zero anti-dumping duties, what could it be that stops Avanti from successfully lobbying for the same?

The comment was more about TUF Ownership in AFFPL - 40% direct plus 25% of Avanti’s 60% = 55%

Nope. It was a general comment how lucrative processed Salmon was - and that unfortunately Salmon and Trouts grow in Cold Sea water, not in Tropical Sea water (warm waters - good for Shrimp) like in India. It was in the context of a question being asked on Avanti exploring other growth avenues. Fish Feed foray was not specifically commented upon. As they maintained in Concall - too early.

Zero Anti-dumping duty is a special status conferred on only 3 companies worldwide by US in Seafood Industry. Devi is one of them. But that status has to be earned over decades of established track record of not selling below cost. Avanti as it ramps up volumes, can certainly aspire for that - but perhas will take equally long time to establish such a pristine track record.

For those who would like to know more, there is this book called “SHRIMP—The Endless Quest for Pink Gold” which you may want to go through for understanding the industry in some detail. It seems to be a landmark book by many accounts.

This post is for those invested in Avanti - and wondering like me - how to take the Valuation Call?

Now that we have a decent measure of updates on the Industry and Avanti’s business, lets assume for a moment, that for the next 3-5 years Industry is stable and growing, and Avanti’s Competitive position remains intact - so it is free to continue to execute !! (big assumptions, but humour me for now)

If Avanti business continues to execute freely, can we try and answer a few back-to-basics questions?

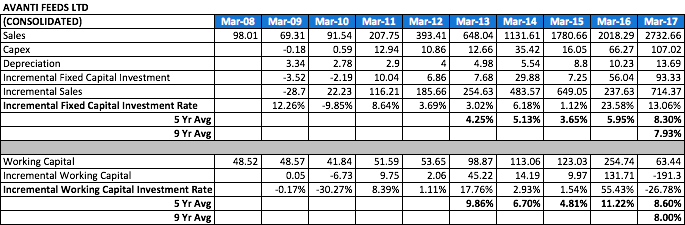

What is the typical (historical) fixed capital re-investment rate for Avanti business? For every rupee of sales, how much of incremental capital does it need to invest in fixed assets?

What is the typical (historical) working capital re-investment rate? For every rupee of sales, how much of incremental capita does it need to invest in working capital?

Has the Product Mix changed? in what proportion? If yes, by how much is it likely to alter the fixed capital and working capital re-investment needs? By how much is the Operating/EBIT margin likely to change with this altered product mix?

Not withstanding the super uptick in operating margins currently, what can we assume as a sustainable Operating/EBIT Margin for next 3-5 years? Also, what can we assume as a sustainable sales growth rate for the next 3-5 years?

in the last 6 months, I have learnt to focus on something very basic. That, if i am able to answer just these above very basic questions about a business with proper diligence, it is pretty straight-forward to factor in - What is implied by the Current Market Price - in terms of Valuations - a la Mike Mauboussin - What is implied in the Stock Price?? What is the Market factoring in today?? Remember Price is dynamic, keeps changing !!

And therein, I believe lies the real clue - about the Valuation Call !!

I find it very useful to join Howard Marks and Mike Mauboussin dictums together, at the hip. A proper assessment of Risk lies in the proper assessment of Stability of “Value” (HM). Stability of Value depends on “stability of future cash flows” (MM). Stability of future cash flows in turn, depends on Industry Stability and Competitive Strategy/Position of the business in the Industry (MM).

Let’s try and explore this further together, tomorrow_

Here’s some of the data points from a historical perspective, for the above queries.(Data Source ; Screener.in, Capex data is calculated, and is approximately correct, please check though)

In the light of what we know currently of product mix changes, Industry stability and Avanti Competitive strategy/position, what kind of assumptions can we conservatively make? Let’s say Product mix in 5 years will look like 50:50 Feed:Processing

Incremental Fixed Capital Investment Rate - Processing segment in general has about 2x the Fixed Capital Intensity of Feed segment. So in next 5 years, we should expect Incremental Fixed Capital intensity to settle at say 1.5x current averages??

Incremental Working Capital Investment Rate - Over the years, Avanti has shown remarkable advancement in Working Capital requirements in Feed Segment. However we should remember that was in a Oligopoly situation and tremendous customer pull for Avanti feeds. In the Processing segment, there is unlikely to be any such advantage, and they will have to compete like anyone else with the large buyers. In fact, depending on the long term nature of contracts,Inventory requirements can go up to even 3-4 months Sales during Peak summer. Which means we need to factor in much higher Working capital requirements. Till we have some good utilisation on the processing side (mgmt guidance for 40-45% utilisation in FY18), we will have to wait for more tangible numbers. But suffice to say, we can err on the higher side by taking 2x current levels??

EBIT margins - have shot up, While some may be attributed to economies of scale and operating leverage of late, much is attributable to the lower RM. Management has said, they cannot/ will not raise prices with every RM rise, rather will look to absorb. So clearly we should factor in much lower sustainable EBIT levels. Perhaps 4-5% points lower than current, as sustainable EBIT levels??

Growth rates - Given the recent enhancements to Feed Capacity, and the huge enhancement 175,000T expected to be in place by Mar 2018 (before next peak season), Mgmt is clearly indicating confidence in the growing market and taking an even greater share of the Feed market. Similarly if 45% capacity utilisation is achieved in FY18 for Processing segment, we are probably seeing the next expansion coming in FY19. Given this backdrop and past track record, can we take a growth rate of 25% for the next few years as conservative??

These points above require some back-n-forth discussion/debate perhaps, to zero down on realistically achievable, and conservative levels. Views invited from folks like @ayushmit@pratyushmittal@hitesh2710 and other bulls and bears

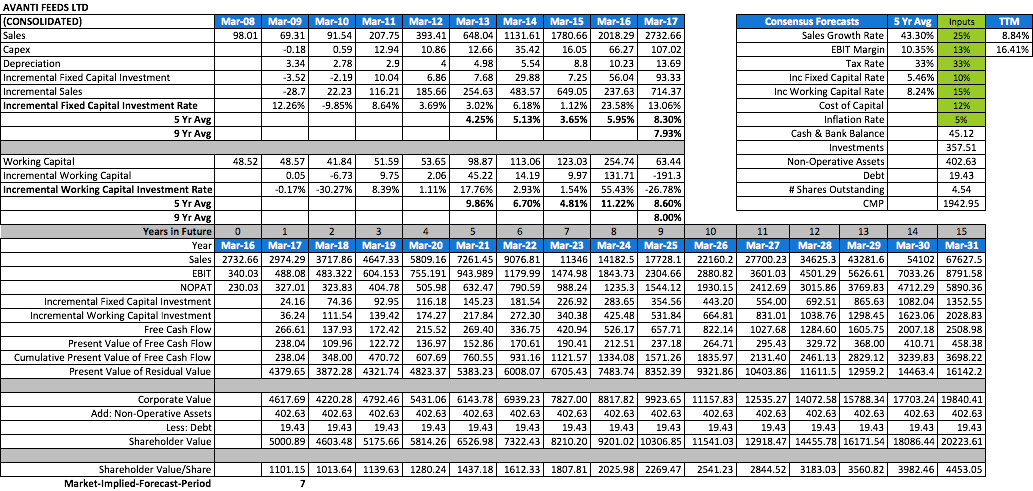

While we discuss and debate - realistic, conservative levels for above data points for Avanti Feeds, here’s something I modeled in using Mike Mauboussin’s Expectations Investing pointers. Excel enclosed. Since there is lucid concise explanation in the website, I am not bothering to explain more and bore you

For illustration, have taken a 25% growth rate, 13% EBIT margin, Incremental Fixed Capital investment rate of 10%, Incremental Working Capital Investment rate of 15%. The model throws up that at CMP of 1942, Market is factoring in Free Cash flows of next 7 years. Should growth rate be closer to 30% and EBIT margins higher at 14%, we may see that only 5 years of future cash flows are factored in todays price.

It’s important to remember that if we get the operating characteristics of the business roughly right and continuously adjust in light of newly emerging data-points, we may have different (more advantageous) price-points down the line to recalibrate your buy/hold/accumulate/sell decisions!!

This is early days for me with the model. I find in it very useful tool to think about a business’s future more tangibly, quiz Mgmt on the operating characteristics of its business, and use for my buy/hold/accumulate/sell decisions - especially for businesses that we know quite well, and have 4-5 years of familiarity with. Needless to say thanks to Screener.in one can upload this excel, and use the Excel export button to use this for any business one is familiar with, in under a minute!

Views invited! Disc: I am NOT a finance/excel expert. Domain Experts may like to check back with the Mauboussin paper/model espoused, and what I came up with. There may well be inadvertent errors. Will be glad if folks can help refine this effort

Hi @Donald - Thanks for your detailed notes above. They are very well written and useful

In the above modelling sheet - I think you are quite right with most of the assumptions. Working capital requirements will increase with the scaling up of processing business, though the good part is that the feed business is throwing out large amounts of free cash flows and this should give them an advantage over other processors (many of them are under lot of debt). Couple of observations on modelling:

In the are where we are putting future numbers, shouldn’t year 1 be 2018?

I think it will be better to consider 20-25% growth for next 3-5 years but after that the rate should be much lower? Can we try another model with this as the input?

I think its just a typo in row 18 on sheet ‘Price Implied Expectations’. Meaning that B18 cell should be Mar - 17 and the cell Q18 should be Mar - 32. The cell K3 (Mar-17 sales of 2732.66) and B19 is the same.

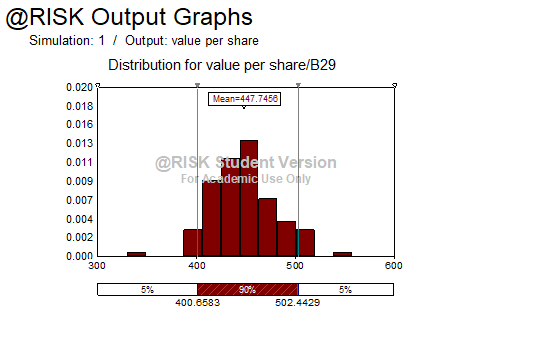

One thing we used to do rigorously while doing DCF was to run simulations to get a distribution for the value per share. Why, because the output (intrinsic value per share) is extremely sensitive to the inputs. Here in this sheet we have 25% of sales growth. Reduce that by 1% and the impact in 2032 is a fall of 10%. That’s why I think simulation would be important. Something like the pic below.

Also finding the weighted average cost of capital is tricky, this too is a very sensitive input. For instance if we reduce 50bps then the change in value per share in 2032 is 13%. In both cases as we move out of time sensitivity impacts more.

I like a novice don’t do such detailed DCFs anymore. I look at ROIC & growth, dcf is too complicated for me

@sajijohn - I think we went from a breakdown to a breakout with a gap-up. I personally feel the previous trendline resistance will now be the support and we have broken out of that. Results have changed things considerably and the chart should be seen keeping that in mind. I feel 1900 levels should be the new base.

@deevee/ others who might be seeing only a DCF here

While what was presented by me may easily seem like a reverse DCF, Expectations Investing (Concept/Book) is much more than that. This is actually not about forecasting using DCF. It is with a twist. I too DO NOT use DCF One must have the patience to go into the book a bit deeper. For those interested to learn more about the proper usage of this important concept …here’s a teaser.

In the preface to the book this is what Peter Bernstein writes, "As Rappaport and Mauboussin remind us repeatedly, stock prices are a gift from the market, a gift of information about how other investors with money on the line are estimating the value of future cash flows. Rappaport and Mauboussin walk their way around this question of uncertainty of future cash flows -by telling their readers not to answer it. Here Rappaport and Mauboussin are at their best. They set forth a systematic testing process to guide the investor toward a reasoned judgment about both the company involved and the market’s expectations, ultimately to determine whether to buy, sell, or hold.

Key to successful investing is to estimate the level of expected performance embedded in the current stock price and then to assess the likelihood of a revision in expectations - anticipating how and when Operating leverage strikes, and much more like other important business value driver triggers. Investors who properly read market expectations and anticipate revisions increase their odds of achieving superior investment returns.

When you go deeper into this, you may also find like me - that this cant be applied to every business. But a business that you know well and have been following for a number of years - to truly understand that business value driver triggers - i find it most suited to Oligopoly situations.

yes thats a typo - Year 1 is actually 2018; just like Year 0 is data for 2017 (not 2016)

Yes, we can do that for sure - first attempt was to introduce the concept of using a business (we know well) operating characteristics and check how much is implied in the price. As we have discussed, many times we find excellent businesses where the Market is factoring in just 2-3 years of future cash flows, where we know important developments are actually shifting the business to a higher trajectory - better mix, higher profitability, better cash flows - that’s where I find this concept becomes very tangible/very effective - anticipating revisions in market expectations - before they happen - thats the promise i see in its judicious use - not just some reverse DCF

If we keep illustrating the use of this with different business examples at different valuation stages - the importance and centrality of the concept might start getting widely understood/adopted.

Donald - thank you for sharing EI “concept”. I read EI book couple of weeks back and planning to re-read it again. I agree with you that it is very useful especially when you know the business in-and-out. But personally - I felt Accounting for Value book to be more practical conceptually, where one can check the implied growth rate in residual earnings (without going deeper into the line items) and determine if it is feasible for the company to achieve it or not.

Wanted to check what you meant by market factoring certain businesses in just 2-3 years of future CFs vs Avanti getting Market Implied Forecasting period of 7 years. How is a business that is being factored in just 2-3 years different than 7+ years?

Thanks in advance.

Disc - holding Avanti since Dec. 2014. Currently 26% of my portfolio.

Will check the Accounting for Value book. Thanks. Actually I find that when you know a business pretty well and have followed it for a number of years - it makes great sense to get into the line items - because then you can catch the IMPACT of changes in business mix like Operating leverage starting to kick in at certain times (and also fading out) in the business - if one followed Ajanta Pharma well and had absorbed EI (which I hadn’t then in 2013/2014) one could have harnessed the dramatic uptick in the business to ones advantage knowingly - out of skill, not luck :), and also be on top of the current fade out. Every rupee of increase in Sales was resulting in 2-3 rupees of EBIT increase then - I don’t find too many of my friends focused on/talking about catching this small, but important aspect!

The same operating leverage (as different from economies of scale) is playing out dramatically in Avanti now. Past experience should tell us, that happy situation is hardly the time to exit the business. So I have found, it pays to go down to the line items.

Simply that lower the number of years of future cash flows factored in in todays price the better. 2-3 years factored in todays price would mean a much higher margin of safety, and therefore I can accumulate more. Price is a dynamic thing - Mr Market keeps giving you opportunities - when it prices inefficiently. With this, we can have a better handle on expecting revisions in future expectations. For e.g. with Avanti quoting at 800-1200 not so long back, one could have used 20% growth rate (and knowledge about Avanti’s FA and WC incremental rates) and seen that market was factoring in under 2-3 years of future cash flows, then …and perhaps used that to one’s advantage.

Not an easy task - but for someone focused on this aspect - could be done!! I intend to apply this to my prospecting/existing universe systematically, from now on.