Some more retail shrimp prices in US, this is Whole Foods in Boston.

And people are pretty serious about antibiotics in meat, so that will not work for sure.

Some more retail shrimp prices in US, this is Whole Foods in Boston.

And people are pretty serious about antibiotics in meat, so that will not work for sure.

Avanti Feeds free fall? anything new apart from plan for the import ban(EU/US) news?

I would say driven by the import ban news along with profit booking and overall weakness in mid-cap.

About Devi Sea Foods - one of the largest Shrimp Exporters -

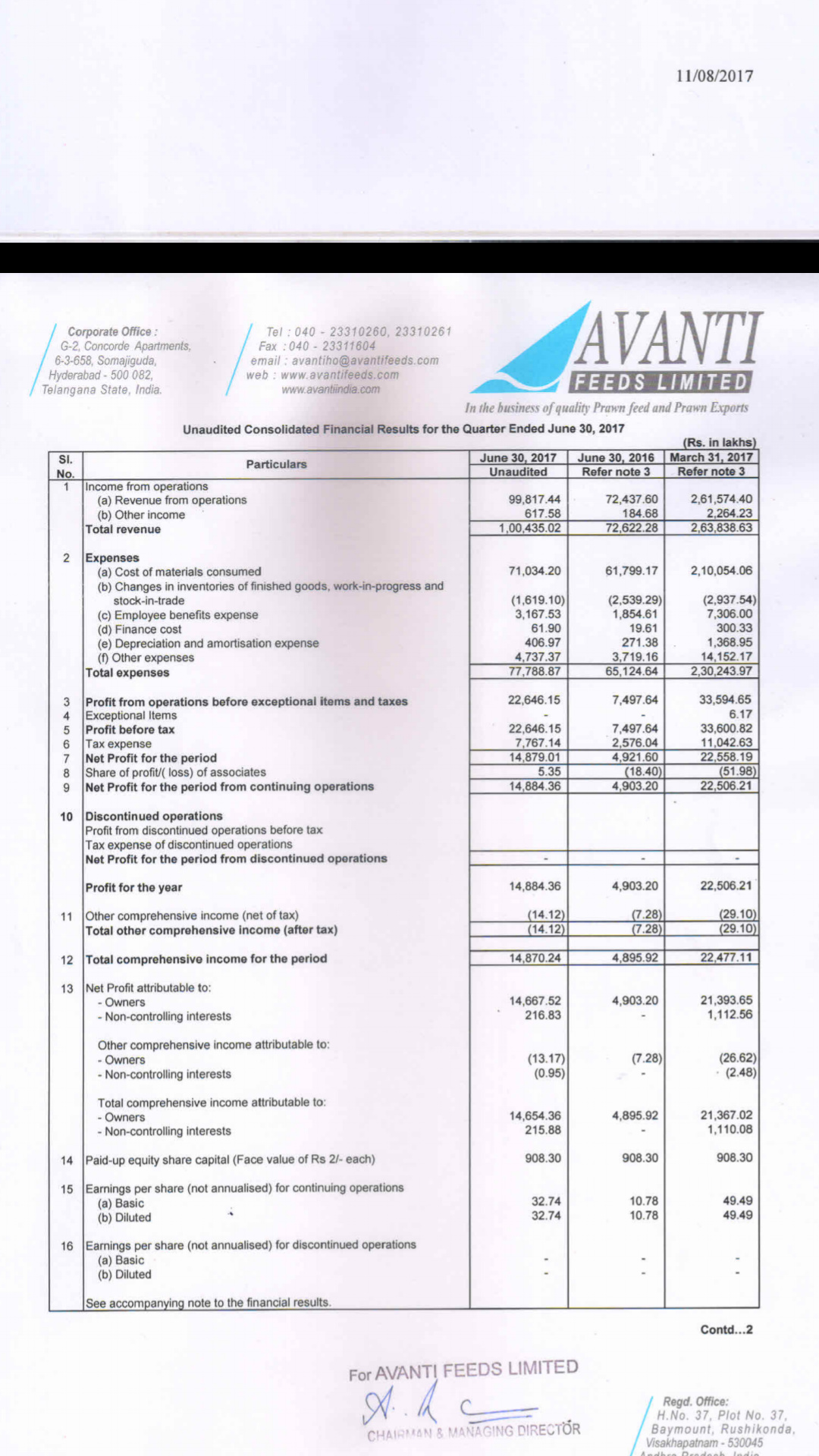

Q1 FY18 results… Could not have asked for more!! Better than expected…

Source: http://www.bseindia.com/xml-data/corpfiling/AttachLive/0e6471f3-6281-4380-abf7-15dd8a8eb935.pdf

23% EBITDA margin Vs 9% for Jun16 and 19.5% for Mar17

15% PAT margin Vs 6% for Jun16 and 12 for Mar17…

Indeed a bumper result…

WIll have to explore whether these margins are sustainable over the weekend. Expert inputs welcome!!

Indeed. Superb performance. Aided by lower raw material costs and higher volumes. Hope to get more detailed info from tomorrows AGM.

Disc- invested

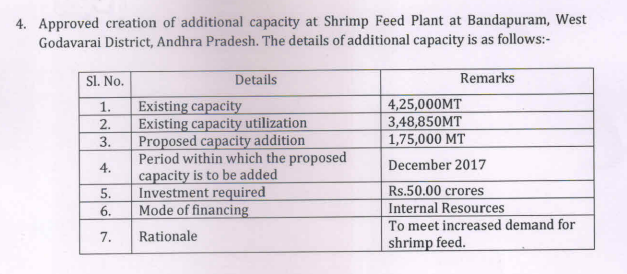

Upcoming capacity expansions

from: http://www.bseindia.com/xml-data/corpfiling/AttachLive/d83647cb-d7be-44f8-a9aa-ed3036f2eaa1.pdf

Very helpful stuff. Thanks these things help a lot

Key takeaways from Avanti feeds (AFL) AGM: Demand remains strong

Demand greater than AFL could supply:

Many thanks. Clearly low capacity utilisation of the industry at large explains the growing moat of Avanti feeds. With players losing market share and operating at half capacity, the question of being able to compete on price becomes increasingly difficult.

I think the key is to understand how strong Avantis customer loyalty is, why it is so and if/how can it be replicated. To me, this company seems to be a page industries in the making unless it already is one

We had 2 other very insightful meetings around the Avanti AGM in Vizag. First one with Senior Management of a featured processed Shrimp Exporter supplying majorly to the largest food distributor chain in US, also slowly ramping up interest in Feed business. The evening meeting was with another 1200 Cr plus processed Shrimp exporter - over 25 years in this business. Request @pratyushmittal to compile and share his detailed Notes, later. Please allow some time for that.

Meanwhile, let me share the most important takeaways (for me) - from the 3 meetings. These need to be examined critically to understand the RISKS - by everyone continuing to remain invested in Avanti at higher valuations. To properly evaluate RISKS, we realise ONLY 2 key questions need to be answered with integrity. 1. Is the Industry Stable and growing? 2. Is the Competitive Strategy/Position of this business getting stronger or weaker?

A. Is the Industry Stable and Growing?

Here are the inputs we got to chew on

Global demand-supply equation: Currently in India’s favour (refer to @spatel posts earlier in the thread), unlikely to change in a hurry. Indian Shrimp Industry is seen as a stable long-term source for quality shrimp. This is a big perception shift towards India and away from other competing producers. Key reasons are good track record at disease management, robust regulatory environment, excellent investments by Top 15 exporters in latest/modern technology, investments in all necessary quality accreditations like BAP, HACCP, and the latest more stringent ACS. US demand seen growing at 6-8% for a number of years as shrimp preference as healthy food is entrenched.

Competing countries ability to ramp up production: Indian production is likely to keep ramping up at 20-25%. Aquaculture has picked up tremendously all along the coastline. India has exploited only 15% of its aquaculture-available coastline so far - if i remember correctly 1.2 million hectares out of 7.5 million hectares. Surprisingly even inland culture (other side of the NH - groundwater salt +brackishness added) has proved feasible and is picking up steam. Unlike India most other competing countries at similar scale - like Indonesia, Equador, Mexico, Vietnam - have already penetrated more than 70% of available aquaculture land. Thailand is unlikely to come back to earlier levels of production

Farmers remaining happy - Key to Industry viability - $4 Pricing Viability line: Currently farmers are able to sell at double of their costing. Now while pricing will always be dynamic, given current supply-demand outlook, it’s seen as unlikely that pricing reverts to levels that threaten farmer viability in the foreseeable future

Very healthy demand for small-size shrimp: Demand for small-size shrimp in resteurant/hotel retail chains in US has seen heavy demand. Customers are happy to get healthy food like shrimp but at lower cost levels (premium prices for large shrimps), making retailers happy too. Key parameter that seems like keeping everyone in the food chain happy. Farmers are able to start harvesting within a month (typically 3 month harvesting)- reduces disease/other risks by half, breakeven achieved, faster turnover. Feed guys are happier with higher demand; Processors are happier because of faster turnaround and lower working capital requirement.

This last one was a surprising new insight gained in the last interview of the day. We need to corroborate this further with other industry experts - will revert. Meanwhile requested @spatel to be on the job to establish count/pricing/quantity value mix

Disc: Remain invested, but examining critically. Likely to trim positions on Portfolio Sizing constraints with increasing valuations

It will be interesting to see results post GST.

Continuing the next scrutiny on evaluating RISKS.

B. Is the Competitive Strategy/Position of this Business getting stronger/weaker?

Here are the key inputs for consideration

Feed Segment - Saturated or Room for growth?: Avanti has always backed itself (maintaining product quality/farmer pull) and taken risks ahead of peers at augmenting capacity aggressively. Even as 4.25 L tonne capacity gets utilised, plans already announced for the next 1.75 L Tonne at a 50 Cr fresh investment. The last 1.25 L expansion came at 70 Cr, so there might be something wrong with the 50 Cr figure - we will revert back after checking. The expansions are on the back of Avanti’s claim - we will continue to expand capacity till the time we are unable to meet demand. This year the feedback from operational levels is they could have easily sold at least 20-25 K Tons more, had supply been there.

Feed Industry Capacity 22 Lakh Tons; Feed Market Sales 10-11 L Tons: Given this backdrop, this is an astonishing performance by Avanti - increasing its distance with peers every year on the back of product quality, continuous data-points gathering from farmer fields of FCR data of Competitor and own, timely support to farmers. Management is very confident of increasing market share to 50-55% harnessing the projected 20-25% growth in annual shrimp production in India. Industry experts (including competition) do acknowledge that Avanti is probably likely to achieve these aims - given its financial strength, farmer pull and quality product, its very effective field-force MIS and support, and the like

Processing Segment - Competitive Position is weaker?: One can easily make the case that probably Avanti competitive position in this segment is comparatively much weaker - given that there are much bigger established players in teh processing segment with deep entrenched relationships with the large buyers for over 2 decades. Avanti has some relationships - but at a very low scale. So achieving scale will take time. There was a surprise here for me as well. It appears TUF - the 55% owner (by virtue of 40% in AFFPL, and 25% in Avanti) now owns minority stake in Red Lobster, it’s US importing arm Chicken of the Sea, and is keen on investing in many other large retail chains (like the terminated Bumblebee acquisition). Chicken of the Sea is the largest importers and supplier of frozen shrimp to all the big seafood establishments in US. Yes, it will keep its 1.5 - 2% margins. But rapid market access to large buyers is a given perhaps, in tandem with Avanti production scale-up. That probably explains the aggressive ambitions on the processing side.

These were my key learnings/insights into Avanti’s business at the moment. Invite everyone invested to chew on these and examine critically.

Disc: Remain invested, but examining critically. Likely to trim positions on Portfolio Sizing constraints with increasing valuations

Now let’s also examine the other Risks - widely thought of as being associated with Avanti Business:

Aggressive EU stance - testing 50% India Aquaculture Consignments for Antibiotics: Earlier only 10% of consignments were being tested. Indian exporters are seized of this and have been educating farmers and conducting tests of their own before acceptance (but again this is on a sampling basis, not 100% and not fool-proof). Multiple processors opined that rejection rates have actually come down despite the aggressive testing and that the EU stance is more a form of govt-to-govt trade barrier arm-twisting for ensuring favourable market access for their products. In any case the Shrimp Industry exports to EU is under 15% for the Industry as a whole. And many of them (who do not have major long-term EU contracts, one of the large processors we met had) have options of avoiding or minimising exports to EU. For them the US and Vietnam (for re:export to China) are the the much larger focus markets. Those with long-term EU contracts have chosen to insure consignments that help them achieve cost break-even in case of such an eventuality.

Disease cropping up any time: Unlike this widely prevalent belief if we speak with any of the stakeholders they tell us the summer months are completely immune to diseases - bacteria/virus does not survive in the harsh hot summers. Only in winters there are some reports every year - but that happens mostly on over-stocking by unscrupulous greedy farmers eschewing best-practices. With increasing awareness levels/education efforts every year this has reduced. unlike Thailand, Vietnam or Mexico with large coastal farms over 30-40 kms of contiguous coastline, Indian Farms are tiny a few acres. Some are 50 Acres. Largest is not more than 100 acres. Hence disease containment (preventing spreading) is far more effective - though such need has not arisen so far. In any case its one harvest washout for those effected, if any. Ponds are dried up and readied for the next harvest/season.

Stringent Anti-Dumping duties may again be levied any time - crippling largest US Market: Again another very prevalent belief, but probably misconceived. Last time duties over 10% had crippled the Indian Industry. Actually the Exporters opine that such stringent duties last imposed had actually strengthened the Industry. Leading Exporters know what is at stake and have adopted better practices, maintain accurate data (cost levels and export price levels). Anti-dumping duties are levied when there is evidence of dumping below cost by exporters across the country (weighted average taken). While there is no repeal of the anti-dumping duties at present, the record on much lower anti-dumping duties of 5% and 2.20% (for period under review Feb 2014-Jan 2015) would tell us that actually the evidence is very strong that dumping-below-cost has greatly reduced and only few instances are now observed. It is reported that final order due in Aug/Sep 2017 for period under review Feb 2015 to January 2016, the duties will be further reduced to 1.07%?? (will check with experts and revert on accurate data sources for the above)

Invite everyone invested to mull on these, and collect more points/counter-points.

Disc: Remain invested, but examining critically. Likely to trim positions on Portfolio Sizing constraints with increasing valuations

How prescient our VP was in predicting potential of this undiscovered gem Avanti in 2014. Thousands would have benefitted by regularly following this lovely thread on Avanti.

How Vannamei has started benefiting large no of por tribals from Odisha as well.?

“Andhra Pradesh is close to our area and thus it became our destination. Vannamei cultivation is a round-the-year affair. We are assured of work whenever we come in any season,” said several Savara tribal youth.

Absolutely correct as usual @Vivek_6954,what a thread…! hope more new and old threads like this becomes alive with new ideas, management talks and field research etc. some examples like premco (consolidating story),chamanlal,KRBL(food exports),tata metaliks,astral(pipes),insurance and AMC and other emerging themes waiting to be explored by our team of donald,avik,ayush,vivek6954 and our fantastic team. Thanks…