The way the company recognizes revenues (only after apartment is handed over) rather than based on % of project completion implies revenue growth will not be smooth QoQ or even YoY. On top of this, the real estate industry is cyclical.

Better to evaluate the biz on a rolling 5 year basis.

I have been dishearted by my investment in Ashiana though I bought it at a lower price; but it has not moved much.

Considering the fact the branded low income/mid income builders with good reputation would be differentiated survive in the long run, what do you think are the conservative estimates for the company sales to be 5 years down the line.

Would it be 2x, 3x, 4x ?

You must have your yardstick to measure if it is a lower price. Personally, I dont think a revival in real estate would be totally visible in next 2 years. So, it is up to one who buys on value and ready to wait till dust settles. Regarding valuations, you can use their current set of projects and get a sense of valuation ranges possible. There are few interesting techniques mentioned on prof. bakshi’s page and on poddar housing thread on VP. As per my analysis, I see it as good value buy provided I can wait for 5 years when sector revives. For me, this is kind of buy and forget story for few years until something dramatically changes any of qualitative and quantitative assumptions

Disc: Invested. Views are personal and not for any recommendation. Please use your own discretion.

I would avoid forecasting rev, profit & cash flow growth. Value the company conservatively based on current or avg of past 3-5 cash flows, and assume any growth is a bonanza. Going by this, Ashiana would begin to look attractive when price falls below 100.

With the real estate sector severely mauled by the demonetization…we need to remember a few points…

in these times of jobless growth, the real estate sector provides lot of employment to unskilled as well as skilled labour

sooner or later, this sector is again bound to pick up…given the trend towards urbanization, demographic compulsion due to rising population and rising prosperity…

we can expect the govt to give support and incentives to the affordable housing sector…vis a vis the premium / luxury sector.

Do all the above points make Ashiana a good long term contrarian bet?

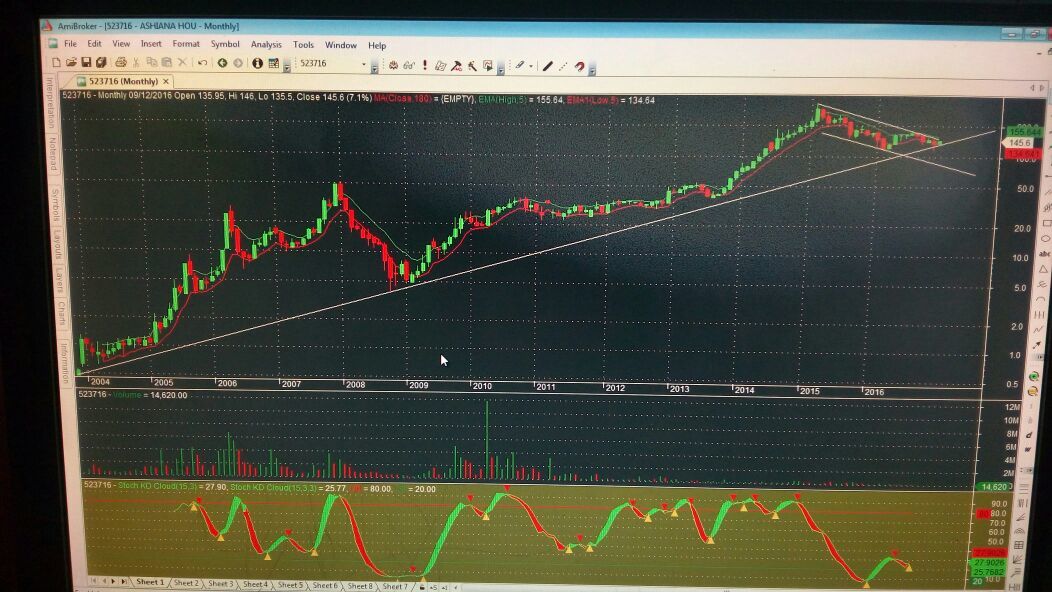

Atleast the long term charts seem to suggest…

Do have a look at the charts of Ashiana…

We already know that it was a favourite of Prof Sanjay Bakshi…now it appears to be a good long term investment for practitioners of slow and focussed investing…

It has been pointed to me by another investor, that Ashiana is taking support from its looong term trend line…and that can serve as a stoploss point…investors may hold the stock as long as it is above this line…

This thread is dead despite 20% surge in price today. its a sign of how pessimistic investors have become about the real estate sector in general…the movement today was sentiments based in my opinion yet I am bullish on the prospects of this company. Its a rare business in the real estate sector run by ethical and transparent promoters. They have a good brand recall in their markets both in terms of development time and after sales service. For the patient investors, Ashiana seems like a very decent buy.

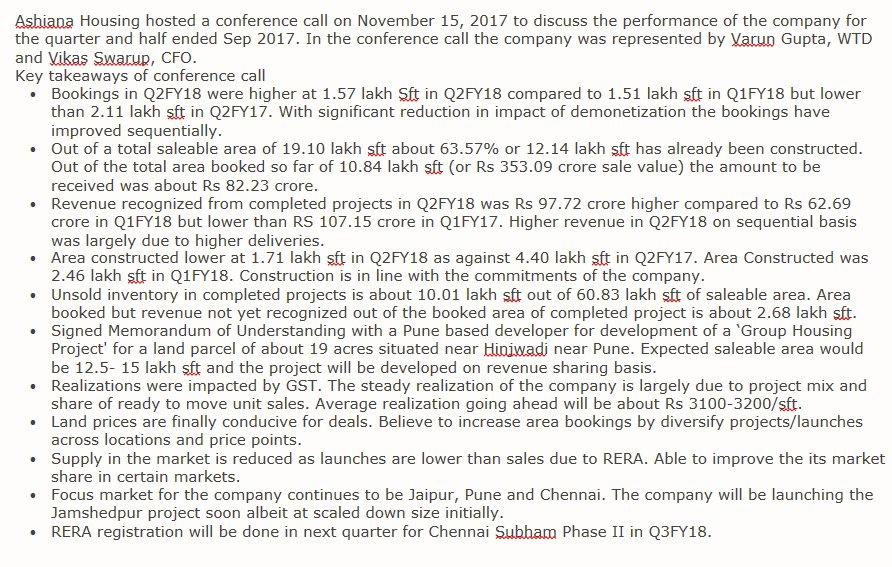

I don’t get this. They are currently not present in the affordable segment (carpet < 645 sq ft), still their stock is running. Have they said anything on this? Any intention of entry in this segment?

If not, then is the stock’s run justified purely on the basis of this credit linked subsidy? Sure it changes the dynamics to some extent. But does it justify a 50%+ increase in valuation (post the announcement) despite the fact that the bookings continue to remain poor?

Yes presently they arent in affordable housing. MD had indicated that they will have to do some adjustments going forward to come in same area category. I dont know if the run is justified. However, when Ashiana did report good nos. in the last few quarters market didnt react then. What has changed then? Perhaps the sentiment, as the MD says, and the only way we will see it is increased area booking nos. in the coming quarters. Even after the run, valaution-wise it isnt streched in my opionion with PE 15x where bigger ones command PE 30-40x.

Thank you for your reply. I believe there’s a reason for the difference in valuation between Ashiana and the biggies. Some of those big players are able to float even in the current troubled waters. Look at Godrej - They are able to sell anything that they launch within a span of a few weeks even today, probably because of strong branding and past track record. While on the other hand, Ashiana’s bookings remain poor, and they haven’t made good progress in majority of their under construction apartments. Please also bear in mind that Ashiana still has about 6.2 lakhs sq ft of unsold area in those projects that have already been delivered (total area in those projects: 42.9 lakh sq ft).

I’m positive about the long-term prospects of the company due to its unique positioning within the sector (senior living, no speculation on land etc), & ethical management, and that’s why I’m holding on. It’s just that I couldn’t understand the current run. But, I agree with you - improvement in bookings can be on the cards in upcoming quarters.

Ashiana follows a direct sales model vs godrej or most of other players and hence 25%+ PAT margins. However, as per 2016 AR, current slump waa one biggest challenge and looks like they r learning how to adopt in terms of sales, however , they have decided not to change sales model. So, may be given some time based on their historical track record, they should do better

In one of interviews,ceo said better signs r visible. From last 1 year, there were no multiple visita but now customers r visiting multiple times n along with family members which they consider a qualitative indicator for buyer seriousness. Let’s see how it pans out .

Also , I believe though they may not get direct benefit of affordable housing ,considering 30-35 lakh ticket size , they will get benefits of govt multiple push to housing plus for companies like ashiana , RERA should be a boon. India has 21000 plus builders. RERA has already led to start of consolidation

How to estimate the future revenues for a company like Ashaina? Considering the state of demand in the RE sector and the management’s view on future sales it appears that revenue for FY18 & FY19 for Ashiana are going to be lesser than that of FY16.