Vijay kedia holding a company stock is a craze… People think if he buys a stock, it must be the next Aegis logistics… But he only knows why he bought Aries agro and holding it in spite of a few years of indifferent performance…

1 Like

Do you feel Aries has as deep pockets as UPL or PI or MNCs to do serious r & d? As far as farmers shifting from urea/DAP to micro nutrients is concerned, that sounds like a dream! Micro nutrients can be supplements , nit the substitutes.

Your point of getting retailers shelf space is valid but please do the reality check, there are 150 small companies of the size of Aries in agri-industry who have their own small strongholds in different states. Only a MNC or a large Indian company has the ability to influence the trade across India.

2 Likes

You are right .People buy stocks by copying big investors and without doing self studies . Later on they try to justify themselves by giving not so convincing arguments.

1 Like

You are right initially i have also very bullish on AA.

When i have searched market there nothing with aries other than high credit cycle business. And when i have searched MDs personal profile i felt he has no guts ,enjoying holidays only:-)

Many things but i also surprised why vijay kedia holding it for 4 years.!

Aries is a 50 year old company. I don’t know about deep pockets but it has good vintage and geographical reach. It is fair to assume it is a first mover in a niche. Aries doesn’t just offer supplements, it offers water soluble fertilizers, pesticides and chelates

Kedia’s investment thesis could be below: Indian farm sizes are tiny. As farm incomes rise, the farmer will look to increase yield on his small tract of land - crop nutrients/fertilizers will take a bunch of that disposable income. Soil Health Card scheme is a trigger as someone mentioned, government also wants the farmer to move away from Urea based fertilizers (which is a huge subsidy burden). Aries currently caters to mid and large sized farmers. Real gains will come when it skims down the market into the small farmer - aided by government schemes.

2 Likes

Global & indian Market scenario

Rise in awareness about the benefits of using crop micronutrients among growers coupled with increase in farm expenditure, ease of application, effectiveness of micronutrients for crop yield & productivity, and surge in demand for biofuels are the key factors aiding the swift expansion of the global crop micronutrients industry. However, the market growth is hampered by factors such as cumbersome mining process of micronutrient reserves, availability of cheap alternatives, and presence of counterfeit products, and lack of awareness among farmers regarding dosage and proper application of micronutrients. On the other hand, investments initiatives by government and private manufacturers facilitate development activities, which are in turn expected to create opportunities for the market growth.

Agriculture in India was historically viewed as a traditional occupation mainly catered to the needs of self-consumption rather than a commercial activity to make wealth of it. The demand for food grains in the latter half of the 20th century led to the Green Revolution. Today farming is more commercialized and there is a growing awareness on the need for improved high yielding varieties, and efficient management of inputs such as water, nutrition and management of pests. It is estimated that 88% of the total available water is being currently used in agriculture. Due to the indiscriminate use of irrigation water and fertilizers, fertile soils have become water logged and saline. The use of micro irrigation techniques and fertigation is the only way to manage these resources efficiently.

Product:

- Micronutrient

- Value added secondary fertilizers

- Water soluble NPK fertilizers

- The Company is part of the growing specialty plant nutrition industry, a distinct section of crop nutrition

- Aquaculture and animal products like fish feed or milk booster

- Pesticides

- Chelates

- Researching hydroponics

More about hydroponics on https://micronutrients.akzonobel.com/applications/hydrophonics/

Business

- Widespread market all over the country especially in areas growing cereals, horticulture, plantations, oilseeds and spices.

- Perennially high working capital requirement due to need to provide credit to the customers and also maintain customized inventory in all areas of operations.

- High seasonality due to dependence on rainfall and changing cropping pattern.

- In AR FY16 The profitability from operations was adversely affected due to extremely erratic agricultural season, requiring additional promotions, excessive discounts to retain market share including higher cash discounts to recover market outstanding. By choosing to incur these costs, the Company managed to retain revenue at the cost of profitability. It was felt prudent to do so since in a highly competitive market, loss of market share would be difficult to recover.

- Flash sales in BSE were done in FY16 and got booking worth 200cr the Company has conducted similar flash sales on the state level and the average conversion of bookings to orders was approximately 75% to 80% , current digital fy18 flash sales has order book 350cr which shows good growth in business y0y

Management

- Management is candid with good disclosure & good promoter holding

- Have established a good distribution network from scratch

- Pay regular dividend

- Company has got lot of awards

- Develop a business in niche under penetrated segment

Risk

- Monsoon risk

- I just can not find barriers to entry and company can loose market share due to competition

- 20-22% raw material sourcing from outside india means rs depreciation risk though 8-10% of export mitigate this risk somewhat

- WC intensive business WCDAYS is very high

- High leverage 90% of it is short term may be due to high WC days

Investing rationale:

- I can see growth with order book in near future and better capacity utilization along with tailwinds like MSP in an election year and good monsoons this year.

- Company is available at Price/3year avg cash flow=3.8

- Long term runway also looks good

- Management has been candid, developing distribution, brands and farmer relation as well as niche products

- Management holding is good

- Cash flows superb and digital flash sales provide order book comfort and is growing

- Soil health scheme and other government initiate along with farmer awareness to provide further boost in long term

Disclosure: Tracking position (1%). This is my initial view of the business and is not a buy/sell recommendation and I may be completely wrong in analysis and I am not a SEBI registered analyst

1 Like

Better would be to bet on the companies which are export oriented and have a brand -image in Indian market. Believe me, I am in distribution business of agro-chemicals . There are 100 other companies selling micro-nutrients similar to Aries. Sales are all linked to longer credit period and higher margins and retialers/distributors like me shift our purchases every year. There is no brand pull from farmers level for the non-established brands like Aries. Customer is dependent on retail -channel for credit so trade decides which brand to push.

And as said earlier, trade tend to push the [products where they get longer credit and higher margins as there is no product differentiation.

9 Likes

If anyone studied AR for FY18 there are some long outstanding recovery from the dealers in gulf region…

If anyone can explains whats that?

Thanks

1 Like

Checking the thread exactly one year later. When I posted the above message last July , price was 119 . Now at 58 . Half with in a year. People may say that all mid/small cap have same story. But let’s separate wheat from chaff and this company is just chaff, nothing else.

1 Like

@ashishverma

You r absolutely right now laughing on my own thoughts on AA.

i have learned at very high cost by the way

1 Like

This is what they call tuition fee. We all have our own fair share of mistakes in this journey called life.

2 Likes

True, This is tuition fees. I got carried away when Shyam Sekhar and Vijay Kedia invested in Aries and everyone was bullish. With borrowed conviction so strong that even with 67% loss did not sell the stock.

1 Like

1 Like

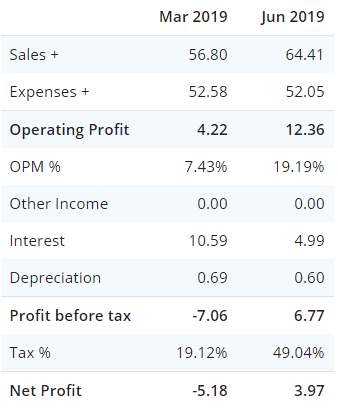

How did interest reduce by more than 50%? Did they pay back 50% of loan in a quarter?

1 Like

How expenses (COGS +others) came down when raw material prices are going up. Also the growth in difficult monsoon period of first period, how they grew when all other companies have shown de-growth. Something is missing.

2 Likes

@ashishverma @SlownSteady @shyamutty @Kuldeepjadeja @saumya2010 - Before posting or even thinking about investing in a company like Aries Agro - I have one suggestion for all of you. Look at how the PAT for this company has grown in the last 10 years - 5 crores to 8 crores - that is an extremely poor performance. In my opinion, there is no point investing in a company like this or doing all this analysis when there is a long term track record and that is so poor. There are plenty of decent, good and great companies on the stock markets where substansial wealth can be created over the long term. In my opinion, there is no point doing secondary analysis of such poor track record companies. The only way to make money in companies with such poor track record companies (and yes, great money can be made) is when you have done professional, real hard, private equity style, deep primary research and when you know exactly what is changing in the company and what will be the impact of the same. This secondary analysis (like % of expenses and interest cost) will lead you nowhere in my opinion. I hope you don’t mind my candid unsolicited advise.

14 Likes

Is this interesting story still? I am not sure why company paying less Dividend comparatively around 2018. Is anyone still holding this counter?

I see Dolly Khanna recently bought good amount of shares in this counter. Is there any new capex going commission soon?

The following filings came in BSE:

Dear Sir,

Pursuant to Regulation 30 of the Securities and Exchange Board of India (Listing Obligations and Disclosure

Requirements) Regulations, 2015 we wish to inform the Exchange as under:

- that a Manufacturing Unit of Wholly Owned Subsidiary viz M/S Mirabelle Agro Manufacturing Private

Limited at Chattral, Gujarat was inaugurated and started functioning from today i.e. 12th July, 2021 with

Manufacturing Capacity for Micronutrients of 9,000 MT per annum.

This is for the information of the Exchanges and to the public at large.

What’s the implication due to this?