Hi,

What do you think about the current valuation of this company?

At this CMP is it a value buy?

Ev/EBITDA greater than historical median

PE is also greater than historical median

However compared to peer it looks value

Thanks

Hi,

What do you think about the current valuation of this company?

At this CMP is it a value buy?

Ev/EBITDA greater than historical median

PE is also greater than historical median

However compared to peer it looks value

Thanks

I am inclined to buy at CMP

Its a personal view, not a recommendation

The corporate structure has become more and more complicated over the years. In 2012, there were only 2 subsidiaries - SR Continental and Somany Global both of which were 100 % WOS. But in FY23, there are 11 subsidiaries and 3 associates / JVs. And many of these subsidiaries are NOT 100 % WOS.

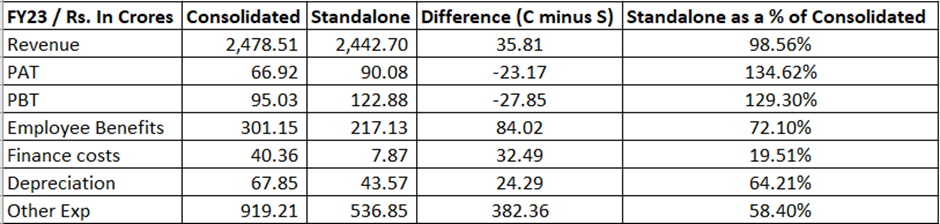

Almost Rs.131 crore have been invested in these Subsidiaries / JVs so far, but the returns from them are nil. While Standalone revenues are almost same as Consolidated, Standalone profits are significantly higher. Look at the table given below:

While almost entire revenues are coming from Standalone, a large part of the costs (Rs.382 crore of Other Expenses!) are stuffed away in subsidiaries. What is happening here? This pattern would have been okay if these were 100 % WOS, but now I think someone is saving on taxes at the cost of listed company’s shareholders.

Another issue is every year there are exceptional items, that too for reasons as bizarre as losing money in employee fraud or broker defaults and so on:

If you have an exception every year, it is no longer an exception, it is a rule.

Does anyone know about the high other financial liabilities ( dues other than micro enterprises) on somanys balance sheet? Is it possible shift of expenses to the balance sheet?