Somany to expand in Tier II cities in AP

CONFERENCE CALL

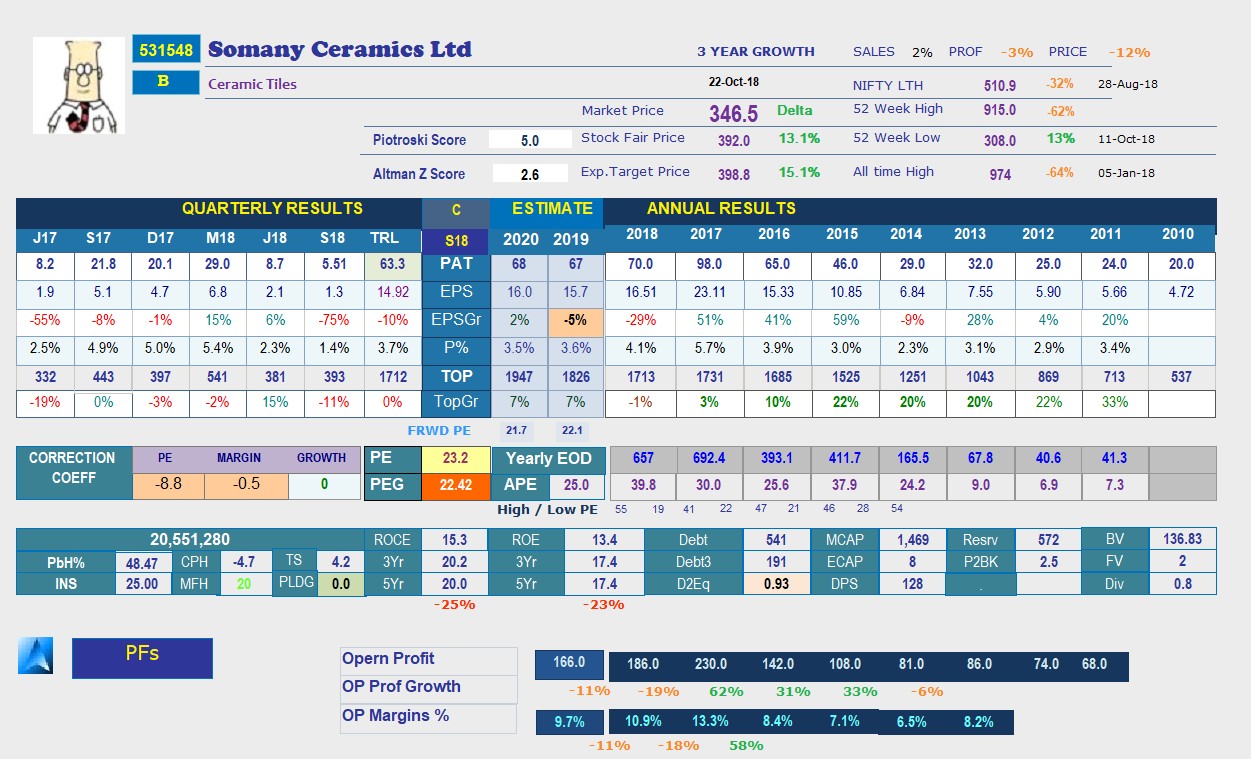

Somany Ceramics

Target revenue growth of 12% for FY16 and 15% for FY17

The company has conducted a conference call on 4 February 2016 to discuss the financial performance for the third quarter December 2015 and nine month of FY 2016 and way forward. Mr. Abhishek Somany, Joint Managing Director of the Company, addressed the conference call.

Key highlights

Net sales of the Company grew 10.7% YoY to Rs 413.08 crore in Q3FY 2016 and rose 12.3% to Rs 1207.87 crore in M9FY 2016. Q3FY 2016 PBT grew by 25.3% to Rs. 21.32 crore with margin of 5.2% M9FY16 PBT before exceptional item grew by 26.6% to Rs 57.68 crore with a margin of 4.8%. Q3FY16 PAT grew by 25.8% to Rs 13.86 crore and 18.3% to Rs 35.00 crore for M9FY16.

The Company gross revenue grew 10.7% YoY to Rs 429.86 crore in Q3FY16. The revenue mix was Rs 152.57 crore from own manufacturing, Rs 195.23 crore from JVs, and Rs 82.06 crore from outsourcings. For M9FY 2016, gross revenue grew 12% YoY to Rs 1257.34 crore, with revenue mix was Rs 447.38 crore from own manufacturing, Rs 532.89 crore from JVs, and Rs 277.07 crore from outsourcings.

Sales mix in Q3FY16 - Own manufacturing (35%), JV (45%) and Others (20%) while for M9FY16 sales mix - Own manufacturing (36%), JV (42%) and Others (22%).

The Company tiles business sales volume grew 8.4% YoY to 11.04 million square meters (msm) in Q3FY 2016, while it rose 9.3% to 32.53 msm in M9FY 2016. For Q3FY 2016, sales volume mix was 4.77 msm from own manufacturing, 4.61 msm from JVs and 1.66 msm from others. For M9FY 2016, sales volume mix was 13.90 msm from own manufacturing, 12.43 msm from JVs and 6.20 msm from others.

The Company plans to increase capacity to ~60 msm p.a. by end of Q1FY 2017 from current capacity of ~56 msm p.a. Capacity Expansion for 4.0 msm p.a. of Glazed Vitrified Tiles at Kassar Plant at Haryana is on course for completion by Q1FY17.

The Company remains optimistic about its future growth prospects in general and building and construction material industry in particular especially in the background of various initiatives being taken by the incumbent government which would fructify in near future. Implementation of Government Policies remains the single largest catalyst to Boost Sentiment and Demand across categories of buyers. Investing in branding activities to create a stronger brand recall amongst buyers.

The Company guides tiles industry would benefit in coming quarter after invitation for anti-dumping duty on vitrified tiles on China commenced. Also, expects recent revision in long term gas prices is positive for the company.

The Company has raised Rs. 120 crores via QIP to strengthen Balance Sheet; Interest of Marquee Investors in QIP reinforces confidence.

The Company guides topline growth of around 12% for FY 2016 with 9% volume growth and 15% growth for FY17 with volume growth of around 12%.

Disc: Invested.

2 Likes

CONFERENCE CALL - from Capital Markets

Expects growth in range of 10-12% in FY17

The company has conducted a conference call on 6 June 2016 to discuss the financial performance for the fourth quarter March 2016 and FY16 and way forward. Mr. Abhishek Somany, Joint Managing Director of the Company, addressed the conference call.

Key highlights

- Net sales of the Company grew 12.7% to Rs. 514 crore in Q4FY16 and rose 12.4% to Rs. 1721 crore in FY16. Q4FY16 PBT grew by 85.7% YoYto Rs. 37 crore and 38.7% to Rs. 91 crore in FY16. PBTmarginsbeforeexceptionalitemat7.3%forQ4FY16and5.5%forFY16.

- The Company gross revenue grew 12% YoY to Rs 533 crore in Q4FY16. The revenue mix was Rs 91 crore from own manufacturing, Rs 265 crore from JVs, and Rs 177 crore from outsourcings. For FY16, gross revenue grew 12% YoY to Rs 1790 crore, with revenue mix was Rs 368 crore from own manufacturing, Rs 798 crore from JVs, and Rs 624 crore from outsourcings.

- Sales mix in Q4FY16 - Own manufacturing (35%), JV (50%) and Others (17%) while for FY16 sales mix - Own manufacturing (35%), JV (45%) and Others (20%).

- The Company tiles business sales volume grew 9.9% YoY to 13.82 million square meters (msm) in Q4FY16, while it rose 9.4% to 46.35 msm in FY16. For Q4FY 2016, sales volume mix was 1.63 msm from own manufacturing, 6.35 msm from JVs and 5.84 msm from others. For FY16, sales volume mix was 7.83 msm from own manufacturing, 18.78 msm from JVs and 19.74 msm from others.

- The correction in gas prices and Anti-Dumping duty on Chinese vitrified tiles has increased competitive edge for tiles manufacturers especially the branded tiles players.

- The Company expansion of Kassar plant(Haryana) for 4 MSM of Glazed Vitrified Tiles(GVT) was successfully completed and commercial production was commenced from March 28, 2016. With this total access to tiles manufacturing capacity increases to ~60 MSM.

- Low gas prices, energy conservation practices as well as a value-added mix aided margin expansion in the Q4FY16.

- The Company expects maintaining 0.5-1% increase on PBT margins in FY17 and to maintain PBT growth between 10-12%. A healthy value-added mix will continue to aid margins this year.

- The Company guides 10-12% revenue growth in FY17. The manufacturing unit at Kassar will help topline and bottomlines both this year. Growth in FY17 will also be aided by strengthening demand, especially post monsoon. The focus will also be on expanding sanitaryware manufacturing, which has already begun.

- The Company guides total capex of 40-45 crore for FY17.

Disc: Not invested any more.

Sold off during Feb correction to cash in on the LTCG and reallocate to higher conviction picks.

2 Likes

It posted back to back disappointing results and now keeps on falling. Any idea of the management future plans ?

I have one question on above , it looks little confusing. Whenever we apply for any debt issue, we apply by giving cheque on direct company’s name. we never give cheque on brokers name and transfer to his account …

Does anyone know about the below loans extended this year?

PS - Mentor (the broker which defaulted with INR 26Cr) has also been extended a loan.

This looks like a fallen angel. Although the company is not as good as Kajaria in terms of capital management and brand recognition, I think it is well positioned to grow once the cycle reverses.

However, we need to make sure that it is indeed an “angel” and not a company looking to cheat minority shareholders. Is it a coincidence that the company lent out to these unrelated parties (in terms of business) and classified it as “loan & advances” which is generally meant for business relationships?

Somany loans.xlsx (10.2 KB)

1 Like

Disc: Not invested

Tiles industry update

Industry volume growth under pressure; GVT pricing pressure intensifies:

-

The Indian tile industry was valued at an estimated INR 285bn as of end-FY19 and has

posted a CAGR of 10% over FY10-19, reaching 750msm at end-FY19 (+5% CAGR in

volume terms). Kajaria/Somany reported tile revenue growth of 14%/10% (volume

CAGR of 13%/8%) over FY11-19. Kajaria management has highlighted that the tile

industry growth was in low-single digits in FY19 and this is expected to continue in

FY20 and FY21 as there are no visible signs of demand greens hoots. -

In 3QFY20, Kajaria/Somany delivered a tile volume growth of 1%/4% YoY. Both

company managements are optimistic about volume growth on the back of a market

share gains from Morbi players following the NGT order, increased spends on

branding and impending improvement in real estate; however, at the same time, they

highlighted that on-ground demand would be tepid over the medium term. Cera’s tile

revenue growth improved to 22% in 3QFY20 (5% in 1HFY20; FY15-19 CAGR: 29%). -

In 3QFY20, Kajaria/Somany tile realisations declined 3%/2%. Both managements

highlighted that pricing pressure in GVT tiles has intensified and is expected to

continue over the next 2-3 quarters, which will keep blended realisations under stress. -

Kajaria’s EBITDA margins contracted 90bps YoY to 15.0% (+30bps QoQ) in 3QFY20

as savings in power and fuel costs (-8% YoY on per sqm basis; -2% YoY) were offset

by an increase in employee costs (+8%YoY; +120bps YoY). Somany’s EBITDA margins

expanded 100bps to 9.2% in 3QFY20 as a drop in gross margins (-460bps YoY) was

offset by lower power and fuel costs (-16% YoY on per sqm basis; -420bps YoY) and

other expenses (-8% YoY; -150bps YoY). -

Kajaria management has scrapped the 5.6msm PVT expansion plan at its Malutana

plant in Rajasthan, and will be catering to future growth through outsourcing.

Somany’s management has highlighted that builder segment sales continue to be in a

bad shape and that it plans to keep a cautious eye on that segment, while the retail

business is in a positive zone. Somany will focus on improving the value-added mix and new product/size launches to sail through tough times.

TODAY @5 pm

Nepean Capital Leadership Series presents

Abhishek Somany, Managing Director

SOMANY CERAMICS LTD.*

(India’s leading Tiles & Bathware company)

will discuss

The Resurgence of Demand in the Tiles & Bathware industry

*Abhishek is a third generation entrepreneur under who’s leadership, Somany Ceramics (SOMC IN) has swiftly grown to become an industry leader in Ceramics, bagging many prestigious awards and global recognition. He has also been recognized in the Power Brand Hall of Fame as a Corporate Leader of the Ceramics Industry.

Date: Mon, Feb 22, 2021

Time: 5 pm IST

Zoom Meeting Details:

Meeting ID: 646 386 9154

From Reliance sec report

What We Heard – Conference Call - Key Takeaways:

-

Demand Scenario: Volume was impacted in Apr-May’21 due to second COVID-19 wave, as SOMC could sell only 85% and 32% of its targeted volume in Apr’21 and May’21, respectively.

It expects >70% of targeted volume in Jun’21, with which it may end 1QFY22 with 65-70% of targeted sales volume. However, it expects sharp recovery in volume during the rest three quarters of the current fiscal. -

Guidance: Despite two months of disruptions due to second COVID-19 wave, it expects volume to grow in high teens in FY22E and sees EBITDA margin in the rage of 12-13%.

Notably, it stated that due to change in accounting standard, margin appears to be higher in 4QFY21, which is not sustainable. Further, it made Rs185mn provisioning in 4QFY21 towards its investment exposure to SREI bonds. -

Capacity Expansion: Expansion programme (10MSM) was impacted led by labour availability issues due to second COVID-19 wave. Expansion plans include Southern region (brownf i eld expansion under 60% JV with total cost Rs750mn), Western region (greenf i eld expansion with total capex of Rs900mn) and Northern region (brownf i eld expansion with Rs400mn capex). Total capex for these expansions – which are expected to be commissioned in 4QFY22E and take SOMC’s total capacity to 72MSM is pegged at Rs1.6-1.7bn. Currently, the company’s owned and outsourced capacity stands at 52MSM and 10MSM, respectively.

-

Volume & Segment Exposure: Retail accounted for a large pie (80%) of volume in FY21, while the government, export and builders’ segments accounted for 12%, 4% and 4%, respectively. Further, Tier-II/III/IV geographies jointly accounted for 75% of total volume.

Segmental Volume in FY21 vs. FY20: GVT: 26% vs. 23%; Ceramics: 39% vs. 40%; and PVT:

35% vs. 37%. -

Dealers Addition: Despite cash and carry business format adopted in FY21, SOMC did not lose any distributor during the year and added 400 net distributors. SOMC attributed reduction in price differential between organized and unorganized segments to government’s vigil against GST evasion and stoppage of coal gasif i ers supplies to Morbi players, which aided the organized players to garner market share.

-

Gas Prices: As per the management, tailwind of lower gas price seen in FY21 is unlikely to persist in FY22E. Currently, the average gas price hovers at ~Rs30-31/SM. (a) North Plant at Kasar: as the gas price in this plant is linked to 3-month average crude price, it increased signif i cantly; (b) Kadi & Morbi Plants: Sabarmati Gas and GSPL increased the prices for these plants; and © Southern Plant: depends upon the spot gas price, which witnessed signif i cant rise. Whilst SOMC anticipates this will weigh on its margin in the coming quarters, it expects the gas prices to decline in the medium-term

-

Export Markets: While SOMC’s exposure to the export market stands at just 4-5% of revenue, it expects exports to account for 50% total revenue for Morbi players in FY22E vs.

40% in FY21. According to the management, anti-China sentiment and China+1 strategy have been helping the domestic tiles manufacturers. -

Morbi Expansion: About 50 upcoming plants (with aggregate capacity of 170MSM) are delayed due to the pandemic. However, it is unlikely to hurt domestic markets, as these plants are mostly coming up for export markets. Commissioning of these plants capacity will take the industry’s capacity to 1,250MSM (>90% from Morbi only).

-

Focus Area: Given its past experiences, the management stated that it will never opt for pledging, overleveraging, running treasury book and loose receivable cycle. Rather, it will remain committed to maintain prudent working capital cycle, cost-rationalization measures and strong balance sheet, which is encouraging in our view.

2 Likes

From ICICI securities report

Capex plans in place to meet anticipated demand

Somany’s entire product portfolio is spread across a) tiles: capacity of 63 MSM/annum (including dedicated outsourced tie ups), b) sanitaryware: 1.15mn pieces/annum (excluding outsource tie ups) and c) bath fitting: 0.65 mn pieces/annum (excluding outsource tie ups). Additionally, the company has announced capacity expansion plans worth ~| 160-170 crore to be spread across a) southern India plant: joint venture with total estimated capex of ~| 75 crore (60% to be spent by Somany), b) western region plant: estimated capex of ~| 90 crore and c) northern region plant: | 40 crore. The proposed capex is likely to increase Somany’s capacity to 70-71 MSM. The management expects commissioning of all plants by FY22-end. We expect overall revenues to grow at ~15% CAGR in FY21-23 to | 2168 crore.

Somany Ceramics Q1 concall summary -

Q1 volume growth at 8 pc. Capacity utilisation- lowest (except COVID days) due lower demand, higher inventory and maint shutdowns

Capacity utilisation now increasing. This plus cost controls,lower gas prices should lead to margin expansion

Current capacities -

Tiles-75 million sq mtrs ( including JVs and outsourcing tie ups )

Sanitaryware-7.8 lakh pcs

Bath fittings-13 lakh pcs

Capacity utilisation in Q1 -

Tiles-70 pc

Sanitaryware-58 pc

Faucets-70 pc

Tiles sales mix-

Own Mfg- 37pc

JVs-35pc

Outsourcing-29pc

Financial outcomes( consolidated ) -

Sales- 584 vs 555 cr

EBITDA- 51 vs 45 cr ( margin at 8.7 vs 8.1 pc )

PAT- 15 vs 21 cr ( due exceptional item of 7 cr )

Total Tiles sold- 15.41 vs 14.25 msm

Bathware sale contribution - 58 vs 54 cr

Net debt down from 308 to 190 cr, qoq !!!

Capacity utilisation now at 100 pc. Things r looking much much better now

Gas prices have come off wef Q1. Now with increased capacity utilisation, EBITDA margins should improve signifigantly

Sanitaryware has also picked up momentum in Q2

Added 50 dealers, 25 showrooms in Q1

Demand in Q2 has been much better. Should pick up further in Q3

Gas prices have further corrected from Q1 levels, down another 7-8 pc

Large format tiles to start production in Q3. No major fresh capex planned in next 2 yrs

Company’s new capacity will come up in Nepal next yr

Share of GVT (value added) tiles now at 35 pc vs 32 pc in Q4

North India is Somany’s biggest mkt. Have seen better sales in July despite heavy rains

Q1 is generally weak as labour goes back home in June due heat

75 pc of company’s sales come from retail segment

Rest is a combination of - Govt business, Private builders and corporates buying directly

Aim to end the FY with 10-10.5 pc EBITDA margins (in Q1, margins were 8.7 pc)

Looking to clock > 300 cr revenues from bath ware business this yr and > 500 cr in next 3 yrs

It has 3-4 pc higher margins than tiles business

Disc: hold a tracking position, looking to add more as the future looks bright

3 Likes

What’s Buyback acceptance ratio for retail share holder? Anyone tendered in BB? Thanks.

Somany Ceramics Q3 FY 24 highlights -

Sales - 612 vs 622 cr

EBITDA - 59 vs 41 cr ( Margins @ 10 vs 7 pc - sharp margin recovery despite sub-optimal capacity utilisation - down from 91 to 82 pc )

PAT - 23 vs 11 cr ( jump in PAT is due to due margin recovery )

Company successfully commissioned a large format tiles / slab plant in Q3

Looking ahead - company is confident of demand recovery as Tiles are consumed towards the end of any project’s construction cycle. A lot of projects went live wef 2022, 23 - should now be nearing completion

Sanitary and Bathware sales @ 65 vs 60 cr. Adhesives sales @ 15 vs 9 cr

For 9M ending Dec 23, Sanitary and Bathware sales @ 187 vs 170 cr. Adhesives sales @ 41 vs 22 cr

Invested aprox 4 cr to set up a solar power plant at the Haryana facility to bring down the power costs in the long run

Spending 70-80 cr/ yr on advertising. Added 300 new dealers this yr

Aim to grow at rates 5-6 pc higher than Industry levels in FY 25

Capex for next yr only at 15-20 cr for Nepal plant

Company’s exports are aprox 3 pc of sales

Company has expanded its total capacity by aprox 25 pc in last 24 odd months vs under 20 pc capacity expansion for the Industry leader ( Kajaria ). Somany shall announce further capex only after 12-18 months from now

In Jan, the company has grown in mid single digits (unlike Q3). Same or better trend should continue in Q4. Margins are likely to be at or above 10 pc at EBITDA levels in Q4 as well

Disc: holding, inclined to add more at CMP, biased, not SEBI registered

3 Likes

Hi Ranvir, I’ve started looking Somany only a couple of hours back and I find it promising. I heard the concall as well, and have a couple of questions which I am hoping you can asnwer.

-

Does the capacity increase by about 25% include the Nepal capex thhat will come live later in the year, or is that separate? They were at 82% tile capacity in Q3, and so if the total capacity increase is just 25-30%, the peak quarterly sales can go up by about 50% at best, unless prices of the tiles rise meaningfully. And if they announce the next capex say this time next year, it will take them probably another year or so to get it on stream. And so they’re not expecting peak sales of higher than 800cr from the times business over the next two years. Is this too conservative, given the uptick in real estate cycle and many projects getting to completion this year onwards?

-

In the Q2 call it was mentioned that 75% of their sales are retail sales. Does this mean individuals who are getting their homes constructed / renovated? Or does this include sales to say a DLF or a Lodha for their projects? The uptick that we’re seeing at the moment seems to be in apartment sales through branded developers. Is the same happening in standalone buildings as well in your opinion? How does the cycle typically flow? And shouldn’t the 75% retail number change going forward?

-

While they haven’t shared the details, my sense is that there can be a decent margin uptick once the new capacities are on stream. But what proportion of the const structure is natural gas? That’s a variable that could impact margins in either direction, irrespective of demand of products

Thanks!

Not invested yet, but interested

1 Like

Hi … @Vineetjain111 …

Some quick thoughts -

The capacity increment includes Nepal - Yes. Even if the peak sales ( volumes ) go up by 20-30 pc for next 2 yrs, I think it would be a descent outcome as the company is sitting on a lot of operating leverage. The margins may end up expanding by 200-300 bps. The bottom-line should get a good boost

If they r capacity constrained / demand outpaces supply before fresh capex comes online ( say 30 months from now ), they can go in for 3rd party manufacturing

Wrt retail vs developer sales - Ur observation is correct. The sales that we r witnessing right now is the base business - IMO ( primarily / mostly the standalone houses being constructed as the construction cycle in case of standalone houses is much smaller + the usual project work ). The kicker should come in once the Tiling work starts wrt the new project work where the construction cycles are longer (2-3 yrs)

Disc: invested, biased

2 Likes

Thanks for your response @ranvir

Also, do you know why margins of Somany Ceramics have consistently been 4-5% lower than those of Kajaria Ceramics? Both have 90% revenues from tiles and 10% from bathware, both have similar product quality, distribution network etc

Kajaria makes higher gross margins which should mean they would be selling at a price premium to Somany. That premium may not go away in a hurry

Wrt Gas prices - I don’t think anyone can predict anything beyond a point when it comes to commodities. However, a slowing Chinese economy gives me reasonable confidence that commodity prices should be well behaved for some time to come unless there r big supply shocks

On Morbi players - Their dumping in the local mkt does have an impact but not a huge one as they lack distribution strength in the Domestic Mkts. Beyond a point, the effect fizzles out - generally

Disc: biased, holding

2 Likes