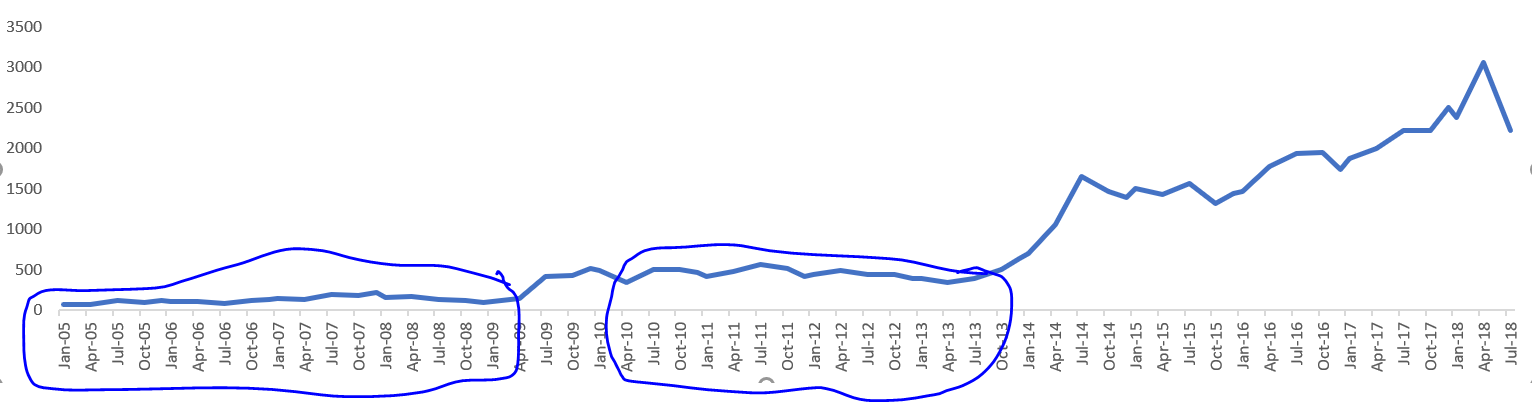

A chart to chew…

Top-line and gross margin improvement is not reflected in the stock price yet. A decent compounding machine is available at more than reasonable valuation currently.

Disc: Invested (post Q1Fy19 results)

A chart to chew…

Top-line and gross margin improvement is not reflected in the stock price yet. A decent compounding machine is available at more than reasonable valuation currently.

Disc: Invested (post Q1Fy19 results)

What has been driving topline growth of late (particularly when the spindle capacity has remain unchanged since last 4-5 years)? Forward integration i.e. Knitting.

Snippet from Fy17 AR -

“During the year the Company has invested Rs 10 cr in Knitting segment. This knitting facility would knit fabrics upto 8,000 kgs per day as of now and 90% of the output is exported.”

“… the Company has planed to invest further an estimated amount of Rs. 20cr in Knitting segment, to augment the knitting capacity further 16,000 Kgs per day.”

Snippet from Q3Fy18 -

“The Knitting facility is operational as on date to an extent of converting 20,000 kgs of yarn per day against the proposed capacity of 30,000 Kgs per day and in respect of the balance capacity installation of machinery is in progress. The products are 90% exported.”

Snippet from Q4Fy18 -

“The Company during the year has further spent an amount of Rs.32.04 Crores In Knitting Facility which was fully met out of Internal accruals and the completed facility would convert 30,000 Kgs of yarn per day Into Knitted Fabrics.”

Snippet from Crisil Jul 19, 2018 credit rating report -

“Revenue grew by 9.4% to Rs 584.4 crore for fiscal 2018, due to setting up of fabric capacity of about 40 metric tonne per day (MTPD) during the same fiscal. Fabric revenue increased to Rs 99.37 crore in fiscal 2018, from about Rs 18.1 crore in the previous fiscal. This growth in fabric revenues is likely to continue over the medium term, supported by steady addition in new clients and growth in orders from existing customers.”

What does this QoQ increase in knitting capacity indicate? Strong traction in fabric/knitting segment in all likelihood.

If i see the figures below…last 3 years they have not managed to increase sales or profits meaningfully…

After reading through this thread i found they have now recently added 30000 spindles which will give them an opportunity to grow revenues/profit by 30% in next 2-3 years.

So given the last 3 years of low growth and future as well looking like low growth numbers… need some help here to understand how others are projecting growth here… would be helpful to understand how those following this company see the future numbers…

| Growth Trends | ||||

|---|---|---|---|---|

| 10yr | 7yr | 5yr | 3yr | |

| Sales | 15% | 14% | 6% | 3% |

| Operating Profit | 12% | 12% | 6% | 0% |

| PAT | 17% | 17% | 18% | 5% |

Almost similar thoughts hit me too that “not easy to fill his shoes”. Tremendous respect for the man. Hopefully, H1FY19 balance sheet should throw some light on progress on discussed expansion.

On succession, as anyone attended AGM and interacted wit daughters and 2nd line of management to get a feel/opinion on capability and ambition ?

Would be good to get a feel of same. thanks for the help

Latest Credit Rating Report of the company. https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Ambika_Cotton_Mills_Limited_August_24_2018_RR.html

Key Points.

Regards

Harshit

Disclosure: Not Invested

Have been watching Ambika cotton for some time now, any reason why there isnt any appreciation in the price.

Had thought that the increase in cotton price is the reason but looks like that is not the case as this would be factored in the yarn that they sell, can someone share their opinion on this plz and correct if my understanding is incorrect, many thanks.

Disclaimer : Not invested but interested

I think rather then price appreciation we should assess whether business quality and business performance in terms of earnings power has increased or not? If the answer is yes then time correction or price correction is good for someone who has longer horizon. This kind of market behavior is very common in dull and boring businesses with boring name (Peter Lynch  )

)

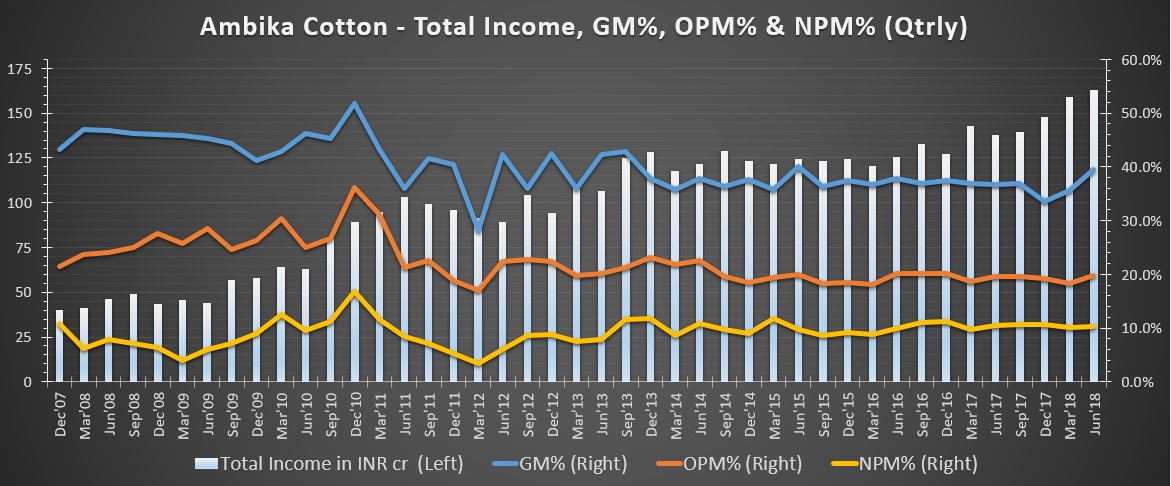

Important point to note is that company is scaling up knitting business very fast. In the above post I had shown calculation giving ~126 cr revenue from decent capacity utilization. The company has already achieved ~100 cr revenue vs. ~18 cr last year as per credit rating report. This is despite very high volatility in cotton prices.

Anytime when I get fed up with a company price stagnation or see someone doing same where company seem to be doing relatively well, I go back and remember TED discussion (does not exist now) that there have been companies which have given 30%+ CAGR over 12-13 years but 8-9 years they did not move at all. Below is a chart of one such company. If you see, in 9 year period from 2005-2014 when it became a 24 bagger, all the gains came in just 2 years and for remaining 7 years, it did NOTHING. Almost NOTHING. Despite of the fact that PAT went from Rs 5.86 Cr in 2005 to Rs 29 Cr in 2009 to 49 Cr in 2013. So, we should better focus on earning and be happy that Mr. Market is giving enough opportunity to accumulate IF we believe in story else pass on ![]()

Leave it to guess the above stock for some fun element in boring price movement of Ambika ![]()

Thanks @vivek_mashrani for the response, appreciate it, one more question in the context of the price rise in cotton, I believe this doesnt have a big impact on the margins of Ambika, is that right understanding?

Thanks @suru27 makes sense, sorry couldnt figure the stock though

This was VST tillers. Used to trade at 5-6 PE despite good earning growth, low debt, decent return on capital, dividend n fair promoters. With stagnant price for years, so much was negativity that people started justifying why it does not deserve more than 5-6 PE until it did a big PE rerating in few months after few years going no where. We often see ourself justifying a high PE if it stays there for few months n justifying a low PE similarly more based on recency biases than structural strengths n risks of business. I keep this as reminder n learning from history.

hi guys

I come from textile industry background with interest in fabric manufacturing and garmenting.It really amazes me to wonder this small company having absolute focus on operational efficiency and product quality while commanding premium for there products and sustaining it through these years.Textile is a very cyclical and commotodised business where sustainability is a issue.I see most of the yarn spinning companies going the the rough patch taking volatility in the cotton prices and degradation of the products as the cotton prices increase.Also there is a structural shift towards more knitted products globally for various applications in mens, womens wear and kids wear.This will one of the other drivers for Ambika.

But here a shining star in the same business but with niche focus, fantastic management,minority shareholder friendly, amazing return ratios, very conservative in thought process.Its very difficult to find a company like Ambika in this sector.I am waiting to add up as and when Mr. market gives the opportunity to load up this stock.Hope this remains underrated for long period of time so that we have long span to add as and when we have surplus money to invest.

dic: invested 5% of my portfolio

AR FY18 notes:

total capacity of 37,000 kg per day could result in 111 lac kg p.a. at 100% utilisation and current rates give around 222 cr topline. but this topline and bottomline also negates revenue and profit from cotton yarn which will be used for captive use for additional knitting capacity. so, not sure of net impact to PAT in next 2-3 years by when 100% knitting capacity gets used

for FY19 assuming 30k capacity usage going higher from 54% to 75% could result in knitting topline increasing from 100 cr to 138 cr and overall net topline increasing by 22 cr and around 2.3 cr PAT

assuming 17 cr PAT from new capacity addition as well as additional PAT from knitting, one gets around 12% CAGR in PAT for 2019-2021. so, agree with ayush thoughts, market may want to see higher longer term growth rates for a sustained higher valuation

2018 2019 2020 2021

PAT 63 69.3 80.3 88.8

growth 10% 16% 11%

@jirohit Please find my estimates attached. My numbers are bit different from your estimate of 12% CAGR. Have given rationale in attached excel. Please note that this is a rough estimate exercise and there could be errors with approach and may not be totally accurate as I have not done a complete BS,P&L,CF tally.

Key Assumptions:

Additional 30000 spindle capacity would be ready by Mar’2020 mostly through internal accrual

Additional 13000 kg/day knitting capacity would be ready by Mar’19

1% of additional margin improvement taken based on :

a. Lower employee salary growth than revenue growth as current year salary growth was 32%

b. Raw material prices will cool off

c. Better margins on higher economies of scale and

d. Higher contribution from high margin value added products

The rates per Kg for spinning, knitting and waste cotton would remain same as Mar’2018

Wherever needed, extrapolation based on last 2 years of numbers has been done (Historical numbers are also more or less consistently uniform)

Knitting capacity utilization assumptions are rough estimates

However, Please note the following:

If we consider as is margins, then, our numbers will more or less tally on CAGR though may differ on year to year basis

Sharing of spinning production for knitting needs with a constraint on capacity is one of major drivers for profitability. In case there is enough demand and new capacity comes up, this could lead to better valuations.

AMBIKA.xlsx (276.1 KB)

Well a good amount of detailed discussion has been done in this thread.

Well I will keep things simple.

At the CMP 1200+, ambika is not undervalued in my opinion.

Even if one look at average historical p/e trend.

Ambika has been running at neck utilisation for few years now. The capex in the main segement(30k spindles) was in talk since 2015 and for various reasons it didnot fruictify. The reasons has been discussed so let me not go there.( Land, approval delays and also unwillingness of managemnt part).

Hence the growth in topline was majorily driven by forward integration( knitting capacity) and improvement in its efficiency.

Now both has its own limitations and kinitting contributes a small part of net earnings( though it has grown in last 2 years considerably with regular capex in the segment).

However the company now seems to suggest that all is clear for their 30k spindle capex which will be done in phased manner by 2020.

But we don’t know how will be demand for those added capacity or how the market is, as there is no immediate past record to suggest the demand in yarn segment is lucrative for ambika to grab.

One would say they have kept their margins and ran on full utilisation for few years now and hence new added capacity will be commercialised as it gets on board.

But I feel thats a question mark?

Knitting capacity is growing and company has every intentiion to grow it further.

Are they looking to make the fabric and yarn contribution more evenly?

Time will tell.

Mr. Chandran has been a great man at helm. Future holds little uncertainity. So lets see how things goes.

I have not added numbers as it has been extensively discussed by others.

I may be wrong in my views as i try to look at simpler and bigger picture.

I feel from these levels( it is not undervalued so not a low risk bet) but fairly decent one. Future is little unrcertain in terms of higher growth numbers if ambika can achieve , the very nature of their business model/ industry has its own inherent risks.

It is a fantastic business and on my watchlist.

M not invested.

Regards,

Mike

hi Saurabh,

2 suggestion in the model:

as per AR FY18, extra knitting proposed capacity is 7,000 kg per day and not 13,000 kg. though it doesnt materially changes the nos.

for the price Gain CAGR, think you have taken time period as 1.5 years, but for sep18- march 21 shall be 2.5 years.

Pls find attached amended model with above changes. saurabh model Amended.xlsx (279.3 KB)

Cotton commodity price is upward trend and lower production forecast in India and world, will be tough to maintain margins