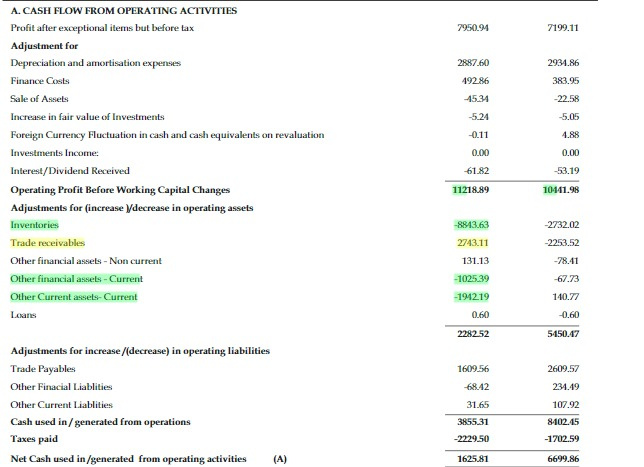

CFO during the financial year deteriorated to 16 Crore(big change in inventories). Generally, ambika’s PAT ~ CFO. This year there is a lot of variance. Any one digged further? Please let me know if I am missing something.

Disclosure: 6% of my PF

CFO during the financial year deteriorated to 16 Crore(big change in inventories). Generally, ambika’s PAT ~ CFO. This year there is a lot of variance. Any one digged further? Please let me know if I am missing something.

Disclosure: 6% of my PF

Snippets from FY18 Annual Report

Cash Flow from operations -

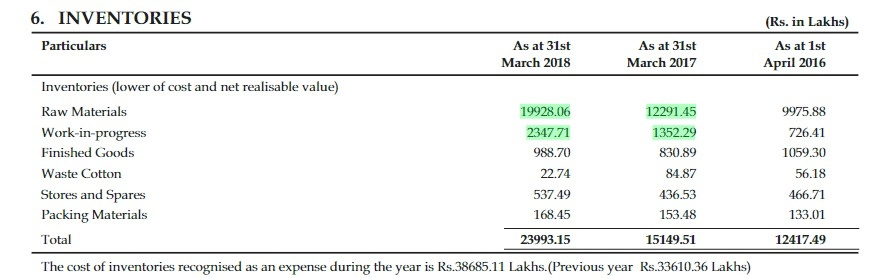

Inventories - Increase in Raw Material and Work in Progress. Companies usually buy cotton in advance in case they have a reason to believe that cotton going forward would be costlier.

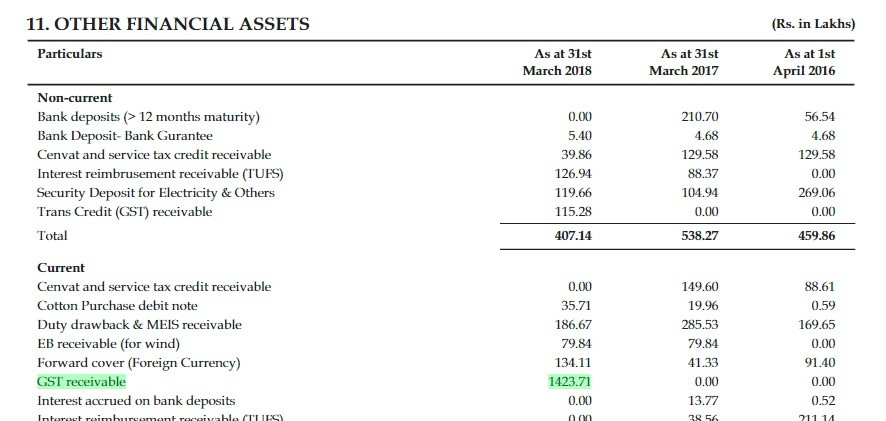

Other Financial Assets - Predominantly due to huge GST receivables. This is a problem with most of the companies due to new GST regime

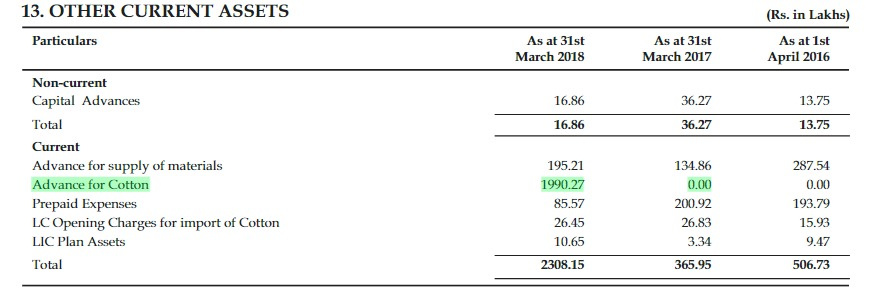

Other Current Assets - Advances paid for cotton are significantly higher.

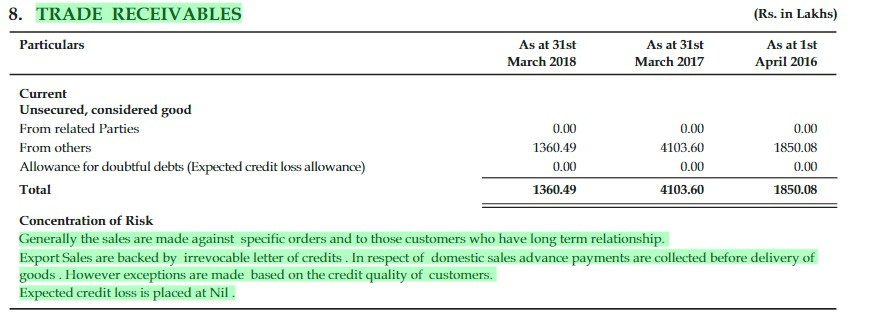

In general, how secure are Ambika’s receivables can be guessed from highlighted note underneath.

@jirohit Thanks buddy for the correction. Appreciate your effort to go through numbers in details. Group effort always helps

Did some more number crunching (again based on lot of assumptions) as I was not sure of spinning vs knitting business with valuable inputs from some of VP colleagues . Putting it below. Let us debate it out and find questions/poinst for AGM which can help us to get deeper insight into business:

As per current estimates, the capex can be done in 2 areas:

spinning

Based on latest capex cost given by management, 30k addition of spindles is projected at Rs 129 cr which means Rs 43k per spindle which historically has led to annual revenue per spindle between Rs 38K - 42K at 10% PAT margins. So, this is is kind of cost and return on investment economics we have based on history.

So, with Rs 100 Cr, we can buy 23256 spindles which can 23256* avg Rs 40000 revenue which is approx 90-100 Cr revenue. So, on a 10% profit margin basis, this comes around Rs 9-10 Cr

Knitting:

In Knitting, as per latest data (7000 kg/day knitting cost Rs 13 Cr) at 100 Cr capex, 55,000 kg/day knitting capacity can be generated which lets say at 70% capacity utilization and Rs 200 per kg price (based on last 2 years range of RS 195 - 202) can generate Rs 281 Cr of revenue which at similar 10% PAT margin looks 28 Cr. This business is a value addition business,so, my guess is it should be better than spinning business

So, on paper, based on these assumptions, knitting capex looks a mjuch better business than spinning but I am not sure if there is something wrong with my assumption.

So, where future capex should go? Is objective of current spinning capex is to support need for knitting or there is enough demand to be sold outside?

Based on 1, knitting seems a better business and knitting contribution in revenue went up but still margins remained same. So, where we are going wrong?

Raw material prices went up from 61% of sales to 64% of sales and employee cost (5% of sales) went up by 32%. So, is it like the benefits of better margins of knitting got supressed.

We say that Ambika can pass raw material prices but 2008-13 avg raw material to sales price was around 53% which now from 2014 to 18 is around 62% and now in current year 64%. Are we really getting biased by by our holding in company? The reason PAT margins were less impacted is more because of expense control in other line items

What is the interdependence between spinning and knitting division from raw material and out flow perspective? What is a better - use captive production for knitting or purchase from outside . why?

@ayushmit @Mridul Thanks for the points. Please add your comments

@vivek_mashrani @jirohit @Nirmal @harshitgoel Any views on above?

I think AGM is scheduled this month. Anyone planning to attend?

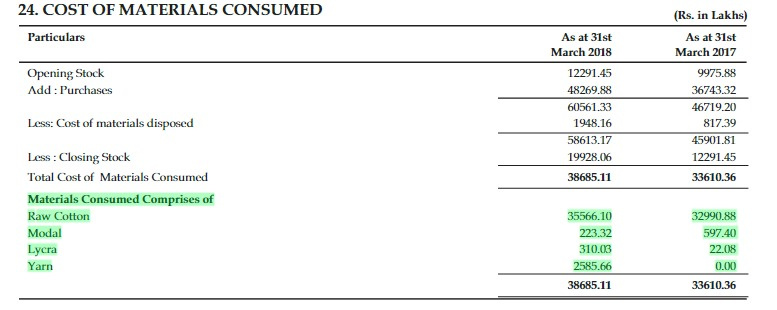

Some additional inputs.

It is evident that they are taking a hit on their margins being unable to pass full RM price escalations to the client. Though, they are managing 19-20% margin profile by cutting down costs (other expenses) and reducing manufacturing expenses. This is clear from the above screenshot.

This huge increase in salaries is probably due to scale up of knitting division.

So they in part are actually purchasing yarn from outside to feed in to knitting division. With fully integrated operations once additional spindles come online, they might become more efficient.

If someone is attending the AGM, what is key to understanding all this is EBITDA per spindle for yarn and EBITDA per spindle for fabric (end to end). And how does this profitability metric change based on in-house yarn vs procured yarn.

Ambika is just doing pure grey knitting and not processing the knitted fabric.So they are selling unprocessed fabric to its customers.Now knitting is also a very competitive/commodotised business with very little margins in grey fabric selling.But as we see what Ambika is able to achieve in terms of their ebitda and pat margins is not seen anywhere in the industry in general.That means they are making special yarn quality with consistent results.Now as you see they are using modal fibre and lycra fibre in their cotton blends which has higher margins as compared to normal cotton yarns.These days there is a good demand in cotton-modal/ cotton-tercel /cotton-lycra value added yarns with superior margins.Going forward if Ambika is able to do more of these blends their margins might increase.We still don’t know about the exact counts they are making in what blends.But looking at their quantity of modal and lycra fiber consumed it looks its a small quantity as on date.I think modal, lycra fibre they might be using for the knitted fabric as well.We could see use of modal ,tencel fibers going ahead for manufacturing of knitted fabrics.Because these fibers are consumed more in knitted fabrics.It would be difficult to judge the margin profile of their knitted fabrics at this juncture,but need to wait for 2 more qtrs to arrive at any numbers.

Similarly if Ambika is able to make some value added knitted fabric then they might command a premium on the same.

if they have good demand for their yarn in the market for the additional capacity they are putting up, it makes sense to sell the yarn and use outsourced yarn for their knitting business.But it needs to be digged further if for the kind of knitted fabric they are making what are the yarn parameters required by them or are they able to source very high quality yarn as required by them at a better price than what they sell. .So if they are able to source, it will alway make sense to sell their in-house yarn and source yarn for their knitting division.

also asset turn for knitting business will be between 5 to 5.5 So for a 37000 kg capacity one would get sales of around 210to 220 crs. on an capex of 1.2 cr per 1000 kgs equals to 45 cr total.This will be a high asset turn business as compared to spinning where it is around 1 for new machinery and 2 on depreciated assets.I have a sense which says this knitted business will have pat margins of 4 to 5% which works out to 10 to 11 crs on a asset of 45 crs(25% on return of invested capital) which is fantastic.I might be wrong in my assumptions here.

in spinning ambika makes roughly 55 tons/day on existing spindles which will increase to around 75 tons/day after addition of 30000 spindles. so if it consumes captive yarn, almost 45 % capacity will be consumed by knitting division and rest 55% for market sales.

so in terms of sales

spinning sales after full capacity utilisation(138000 spindles) will be roughly 400 cr with 10% net 40 cr pat

knitting sales 230 crs with pat of 15%(10% spinning pat and 5% knitting pat) (37000 kgs/day) pat will be 35 crs.

waste cotton -90 cr and other revenue- 19 cr total 109 cr with 10% PAT -11 CRS

so total revenue=400+230+90+19=739 crs

total pat of 40+35+11=86 CRS

above is a rough estimate.(figures can change drastically if margins on knitted business is more than 5% what I have assumed)

will try to check from market sources abt their current yarn products and knitted fabrics ambika is making to arrive at some concrete conclusions.

disc-invested

Thanks guys for detailed discussion. Its definitely good to see that Fabric segment has picked up well for Ambika and there are further expansions lined up.

Fabric is more of a value-addition that they must be doing and consuming the yarn in-house that they were producing. The yarn brought from outside must be the different kinds of yarns needed to be mixed to make fabric. The good thing is that making fabric would bring them closer to the customer and open more growth opportunity.

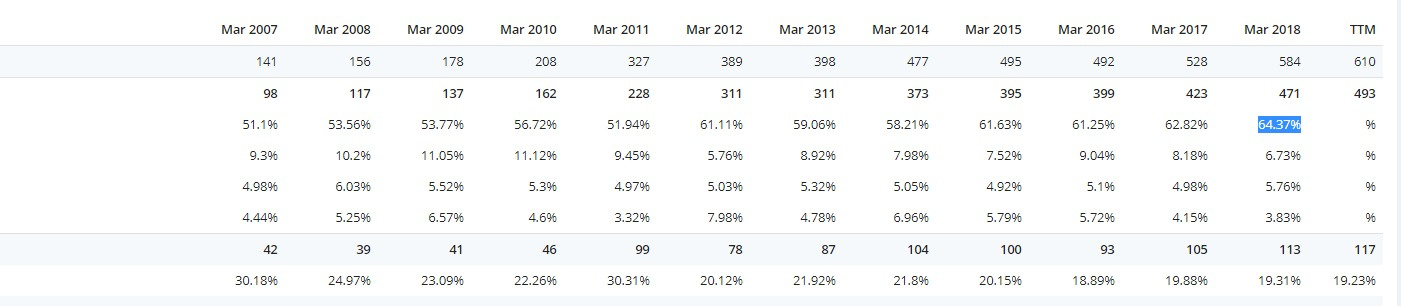

I have been amazed at the quantum of production they are able to do. The company hasn’t expanded capacity for quite sometime yet every year they have been able to deliver on volume growth:

In the below data the sale includes yarn and fabric sale. Sale qty is the total yarn produced (including in-house use for fabric)

On the negative - despite such stellar operational efficiency + fabric, the margins are at same levels or have softened a bit. Though the performance is commendable given the sad state of affairs in the whole textile industry esp yarn.

Other thing to notice is the high dividend payout

Also, the company imports all of the cotton. What will be the impact given the sharp rupee fall? Though they might have a natural hedge as they export also.

Regards,

Ayush

Disc: Invested

Thank you for sharing your working. It was very helpful. I have a few observations.

If we go back to AR 2015-16, the company has mentioned that they are implementing knitting

facility which shall be operational by October 2016. Prior to this, the Company had knitting

facility of ~3,000 kgs per day (10.1 lakhs kg production as mentioned in AR2015 - increased

from 2,000 kgs per day (7.3 lakhs kg installed capacity – as mentioned in AR of 2011). So as of

March 2016, they had capacity of ~3,000 kgs per day.

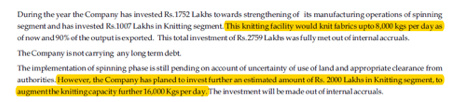

2017 AR – the Company spent Rs. 10.1 crores and knitting fabric capacity was 8,000 kg per day (operational from October 2016 as mentioned in AR 2016)

The Company also mentioned they will be adding additional capacity of 16,000 kgs per day

during the year.

Quarterly results of 1Q18 mention that Company is adding the said capacity which will be ready by November 2017

![]()

Quarterly results of 3Q18 mention that the capacity has been increased to 20,000 kgs per day

and will be increased to total of 30,000 kgs per day (instead of 24,000 per day as mentioned

earlier)

![]()

Quarterly results of 4Q18 mention that the capacity has been increased to 30,000 kgs per day

![]()

Therefore, the weighted average capacity for the Year ended March 2018 was

(8000x6 + 20000x3 + 30000x3)/12 = 16,500 kgs per day. The company produced knitted fabric of 49.1 lakh kg during the year, taking the average capacity utilsation to c. 81% for the year.

If we assume similar capacity utilization numbers (85%) for future, the revenue from knitted

fabric increases from 99 crores in March 2018 to 235 crores in March 2021. The increase in

knitted fabric revenue is offset by reduction in cotton yarn revenue (higher captive utilization of

cotton yarn)

Also, the Company will take at least 2 years to add 30,000 spindles. So the full increase in

production will come in March 2021 and not in March 2020. Conservatively, let’s assume they add 10,000 spindles (weighted average for the year) by March 2020 and total of 30,000 by March 2021.

I have made these changes in your model (highlighted in Red). Please find attached the revised version. saurabh model Amended_Hardik.xlsx (279.5 KB)

Overall numbers don’t change much in March 2021 as the increase in revenue from knitted fabric is offset by decrease in cotton yarn revenue. However, if indeed margins are better for knitted fabric, the overall PAT margins will improve. (I have not changed your assumptions here). After the changes, knitted fabric accounts for 31% of total revenue in March 2021 (27% in your version)

Kindly share your thoughts.

Can you please explain point number 7. What are your underlying assumptions driving knitting revenue from 99 crores to 235 crores by 2021? Thanks.

I have not changed these assumptions from @suru27’s model except that capacity utilisation is assumed at c.85% as they have already achieved c.81% for FY18. Saurabh’s model has assumed 75% utilisation for FY21, may be because in his model the capacity utilisation for FY18 comes to 56%. I beg to differ here and I have shared my thoughts on the same in above post with updated model.

As per my attached model, the knitting capacity is 37000 kgs/day. At 85% capacity utilisation, this translates to c.115 lakhs kgs. Revenue per kg for fabric works out to Rs.202 for FY18. Even at the same rate of Rs.202/kg in FY21, total revenue for FY21 works out to c.232 Cr. infact, as per model this will happen in FY20 itself and is assumed constant for FY21.

As per the sales break up given in the Notes to Accounts (page 57), the company’s sales revenue from cotton yarn was Rs.410.34 crore and that from knitted fabrics Rs.99.37 crore. As per the MDA (page 23), the quantity sold was cotton yarn 154.66 lac kg (excluding captive consumption) and knitted fabric 48.51 lac kg. This gives me a sales realization of Rs.265.32 per kg for yarn and Rs.204.85 per kg for knitted fabric (99.37 * 100 / 48.51 = 204.85). How can realization for fabric be lower than that of yarn? What am I missing here?

As per what I know from industry sources and other analysts, Ambika cotton does not only manufacture premium yarn from their installed spindles. Approx 75% of spindles are used to manufacture speciality ultra premium yarn that is used for exports to branded players like Uniqlo, etc. Rest 25% spindles are used for manufacturing commoditised yarn that is used for supply in local markets, etc.

What I think is, ultra premium yarn is made for exclusive third party sale and not captive usage in making knitted fabric. Now the difference in costing of normal yarn and ultra premium yarn is massive. They use 20-25% spindles for making standard yarn which is now used for captive purpose of knitting fabric. Realisation for this fabric can be far lower than realisation of the premium yarn exported, due to a massive difference in the quality of the premium yarn made from Supima cotton.

An Analogy would be, SAMSUNG selling ULTRA HD DISPLAY ONLY to Apple for let’s say Rs. 15,000.0 vs they sell a mid -range Samsung branded complete MOBILE PHONE for Rs. 12,000.0. Their numbers would say that realisation for entire phone is lower than realisation for only displays sold to third party.

Now that they are finally expanding their spindle capacity, it needs to be clarified by the management as to what yarn will be made from these spindles, premium or standard. And how many of these additional 30,000 spindles are going to be used for making yarn for captive consumption and for exclusive sale.

I am surprised as markets have not discounted the growth due to the much awaited CapEx plan. It will have to be understood from this AGM whether they have signed exclusive contracts with clients for premium yarn, fabric, etc in order to understand better how this additional Capex will be utilized.

The most important part is to understand what is the ROCE on yarn vs ROCE on knitting. Even if realisations in knitting is lower, it can have a much higher ROCE. Now how much would you consider the cost of yarn used in knitting that is coming in from the same premises, where the same yarn could have been sold as well. It is also important to remember that the yarn used for captive consumption is of lower quality that yarn sold / exported.

Discl: Ambika cotton forms 30% of my portfolio and adding at every dip

Having 30% and adding more pose a risk at portfolio allocation side which says need to have 10 to 15 stocks in portfolio…I hope you would have given thought on that…just my cautionary thoughts…I have very bitter experience of portfolio allocation side

Happy investing

I am attending AGM on 27th Sep 2018 at Coimbatore. Anybody else attending? I was planning if we can ask the mgmt for meeting/plant visit post the AGM. Also, pls let me know if you have any questions which you may like to ask the mgmt in the AGM?

few queries for AGM:

Hi Varun…

Mentioned this in my posts above but posting here again for you to add to your Qn list.

A. EBITDA/spindle for just yarn

B. EBITDA/spindle for fabric (end to end) i.e. yarn + fabric

How does this ebitda/spindle metric change based on in-house yarn vs procured yarn?

What was the knitting utilization for fy18? Target for fy19?

Will all fabric be made from in-house yarn i.e. at 100% knitting capacity utilization?

Why did ebitda margin deteriorate despite knitting capacity coming online. Expectation was that there would be an improvement.

Why was cash flow from operations lowly this year? In part we know (cotton advances, gst receivables, and stuff), but would be better if we can get a direct answer.

Thanks.

Hi varun,

Just ask a simple question on my behalf.

How does the company see the knitting and yarn segement contribution going in to future?

Are they focussing on increasing % of the knitting segment substantialy wrt total earnings?

Thanks

Mike

Hi Varun, One question from my end would be - What is their succession plan?

Varun,

just if you can check, if the old issue of court case on nearby land is resolved fully. though it seems so because of expansion plans but never have seen it being mentioned explicitly so far.

I realy wonder if some1 want to exit ambika, how he will. It just doesnt have any liquidity.

Liquidity is also a margin of safety