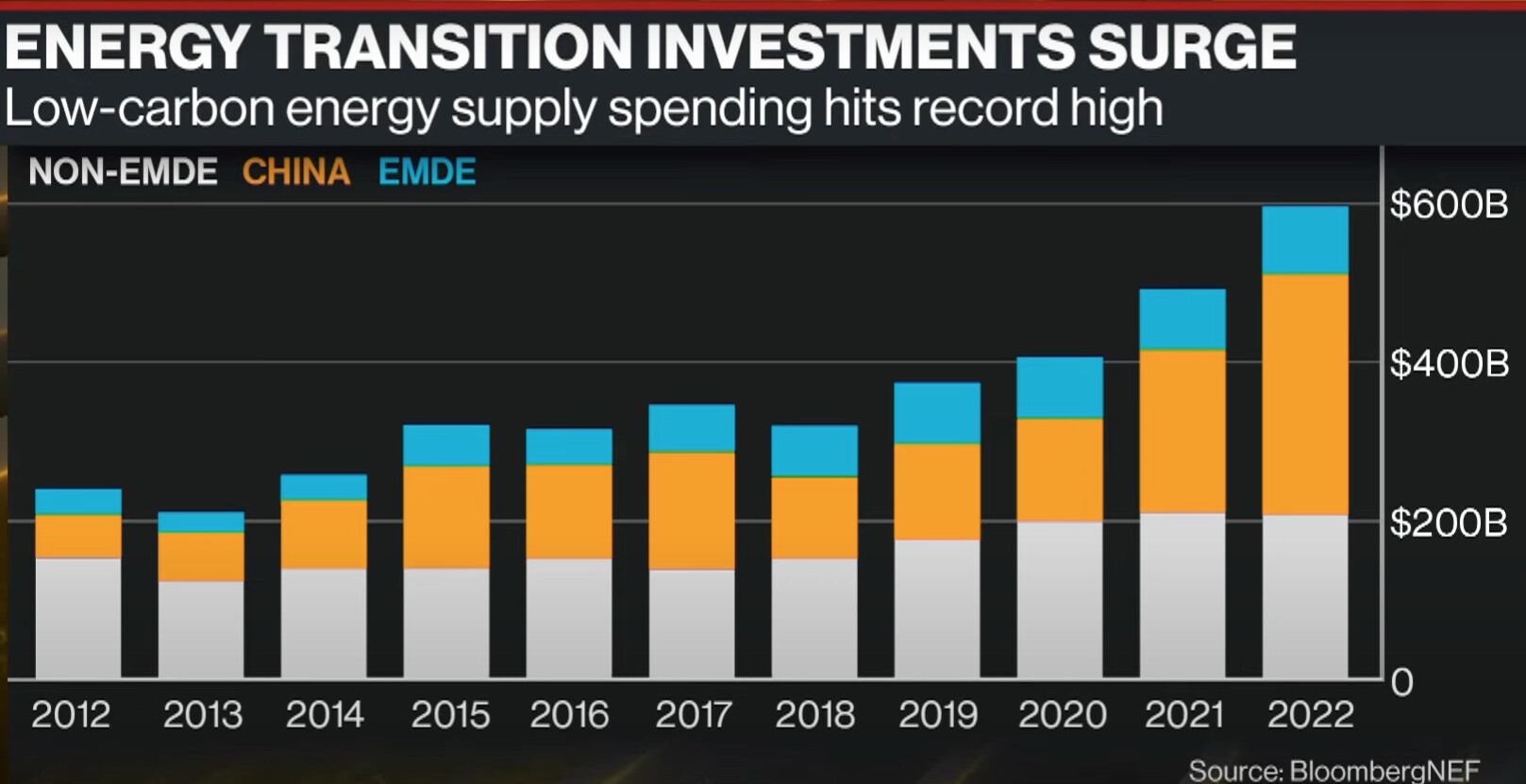

Energy transition direct relation to storage too.

1 Like

VinFast, the Vietnamese electric vehicle manufacturer a key competitor of Tesla and BYD, is preparing to inaugurate its inaugural production site in India, specifically in Tamil Nadu’s southern region. The facility is touted to be primarily dedicated to producing batteries for electric vehicles (EVs). Notably, this venture in the city of Thoothukudi stands distinct from VinFast’s earlier intentions to assemble vehicles using parts imported from Vietnam.

4 Likes

Assuming Only Electric is the future might be ignoring on-ground reality. ICE cars are here to stay.

1 Like

EV adoption won’t take off significantly unless it gets to place where it’s near competitively priced with ICE vehicles.

Even in markets like US and China ICE vehicles are still dominating in sales.

2 Likes

1 Like

Gautam Ji, What conclusion we should draw from this. (Please accept my sincere apology, if my question is too silly)

1 Like

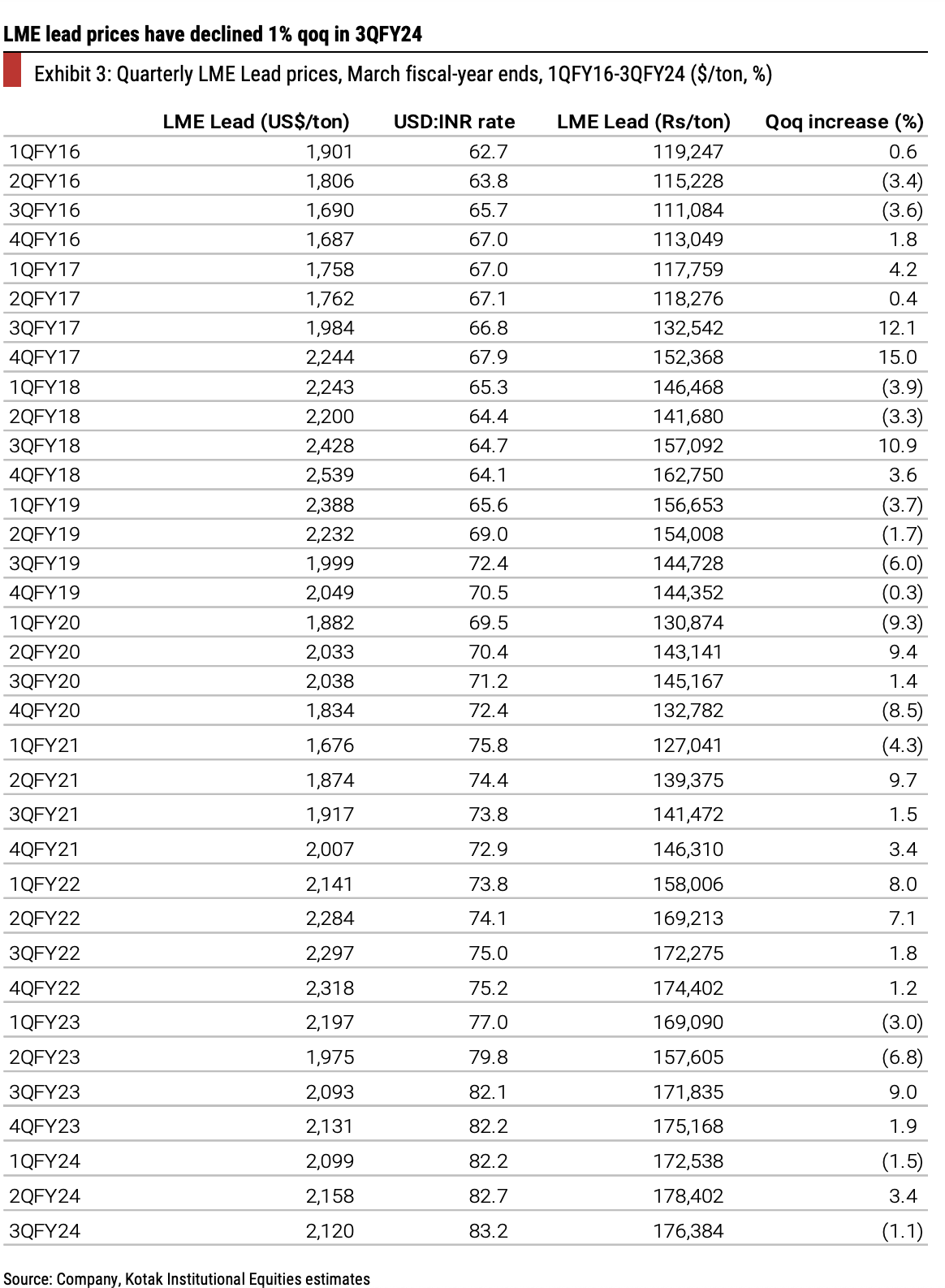

We see a decrease in Lead prices as per LME exchange.

Which does impact battery space businesses. Also, a long historical movement to visualize volatility.

Kind of a overhang apart from the BAU at Amara raja. Might help Mcap for Amara raja

2 Likes

Some discussion around battery companies.

Calls it a day in politics and will start to focus on Amara raja as per news

3 Likes

Galla, 57, is one of the richest MPs in Lok Sabha with a declared asset of around Rs 683 crore. Amara Raja is moving from being a battery manufacturer to a comprehensive provider of energy and mobility solutions. “It is with a heavy heart that I announce my decision to not contest in the upcoming 2024 general elections. I will be taking a break from politics to focus on diversifying the business which is at a crucial stage of leading the world in the transition to a more sustainable future,” said Galla, who represents Guntur in Parliament.

Bold letter represent : positive for business.

6 Likes

PE is low, ROE is better than Exide. Promoter returning back to participate in renewable game.

Looks like low risk bet.

Disc : Not invested, will do soon.

2 Likes

Looks like a breakout in stock on news of Mr Galla exiting politics . Has a potential of giving multibagger returns from here considering the tailwinds in Industry and its financials compared to Exide . Waiting for this quarter results and management commentary to confirm my views

3 Likes

Microsoft Word - Outcome of Board Meeting - January 31. 2024 (bseindia.com)

Result

Microsoft Word - Outcome of Board Meeting - January 31. 2024 (bseindia.com)

Press release.

Concall on 02.02.2024, so get better idea on Mangal Industries Merger and future giga factory.

2 Likes

Amara came out with decent results with sales and EPS growing by 15%. It seems that their new energy business benefitted from lower lithium cell prices. This also brings into question future of lithium battery business, at a scale of 7-9 GWh, they expect to make 10-11% EBITDA margin at current cell prices of $80/GWh. They even went on to say that given the Chinese overcapacity, EV penetration has to reach 50% for the business to be lucrative. And market is most excited about this division! Concall notes below

FY24Q3

-

Lead acid battery : 13% YOY growth

-

4-W volumes : OEM: 2%, after-market: 11%

-

2-W volumes : OEM: 30%, after-market: 15%

-

Industrial volumes : growth of 6-7% (telecom: 8-9%, UPS: __%)

-

Home inverter volumes : no growth (only doing trading currently)

-

Exports : 24% YOY growth (4-W AGM batteries: 25% volume growth). Revenues are recognized after delivery. Catering to large retail chains

-

RM pricing : 200/kg (have not taken any price hike)

-

Trading revenue of 7%

-

50% of volume is from after market

-

-

New energy business :

-

148 cr. (vs 150 cr. in Q2 and 68 cr. in Q3FY23). 80% battery packs of 2-W and 3-W (Mahindra and Piaggio are main customers with 2-W being small)

-

Successfully powered an E-Bike using in-house NMC based 2170 cylindrical cells

-

Have started supplying battery pack for telecom (BSNL) and for industrial applications

-

Small cell towers have seen adoption of lithium packs

-

-

Tubular battery plant will be ready in March 2025

-

Plastic component acquisition from Mangal Industries is now complete, effective date will be 01.02.2024

-

Lithium cell : currently estimate 10-11% EBITDA margin (at current lithium prices) with 10-11% ROE at 7-9 GWh scale (@$80-90/GWh)

-

Given the Chinese overcapacity, EV penetration will have to reach 50% for business to be lucrative

-

FY24 capex: 250 cr. (lead) + 250-300 cr. (lead recycling + new energy). Recycling plant will commence in Q1FY25

-

FY25 capex: 600 cr. (mostly around new energy)

Disclosure: Invested (position size here, no transactions in last-30 days)

15 Likes

Is there a way to know market share of Amaraja for telecom towers ?