I was researching on Alkyl amines stock, found that it has decent ROE , ROCE, dividends, debt to equity and profit growth history. However one aspect that was surprising was that i could not find any mutual funds holding on this. In this day of specialty chemicals hype and research on small and midcap research this is surprising. I am hoping that i am not missing out some crucial information about management quality or something. I did search on promoter history a bit, not finding any major issues so far. Another research report by Philip capital also shows alkyl amines in it, but finally not recommended : http://www.phillipcapital.in/Admin/Research/702452410PC_-Specialty_Chemicals_Sector_Initiation-_Mar_2016_20160329212843.pdf . Find it strange to believe that no big fund managers are finding it worth buying. Anybody has more information on this company beyond what numbers show out there?

Alkyl Amines is been tracked by BOB Capital since Dec 2015.

You will find quarterly reports for Alkyl Amines on the BOB Capital Research page.

The firm has capacity expansion planned in Dahej which is underway and should come online FY 17-18.

I have also found the concall transcripts very useful in understanding this firm.

Disc. Invested.

Alkyl Amines Chemicals Ltd Q4FY16 Result Review - https://www.bobcapitalmarkets.com/getreport.asp?id=149

Alkyl Amines Chemicals Ltd Initiating Coverage with BUY - https://www.bobcapitalmarkets.com/getreport.asp?id=102

Thanks @elusionist . Before making this post i somehow could not reach to the BOB recommendation. Now i also see that FirstCall research is tracking this stock as per information in moneycontrol. I had bought small quantity and was ever confused after that about my decision particularly since i could not find opinion from more experienced investors. Another point that scared me was same promoters seem to own another company by name Diamines and chemicals ltd. There was a report about fundamentals and valuation of that company here which was showing it in good light and projected bright future in 2011(that was not buy recommendation though) : http://www.dacl.co.in/investors/Crisil%20Report.pdf . It said crisil report. But ever since then stock seems to have declined, sales and profit numbers of that company were scary.

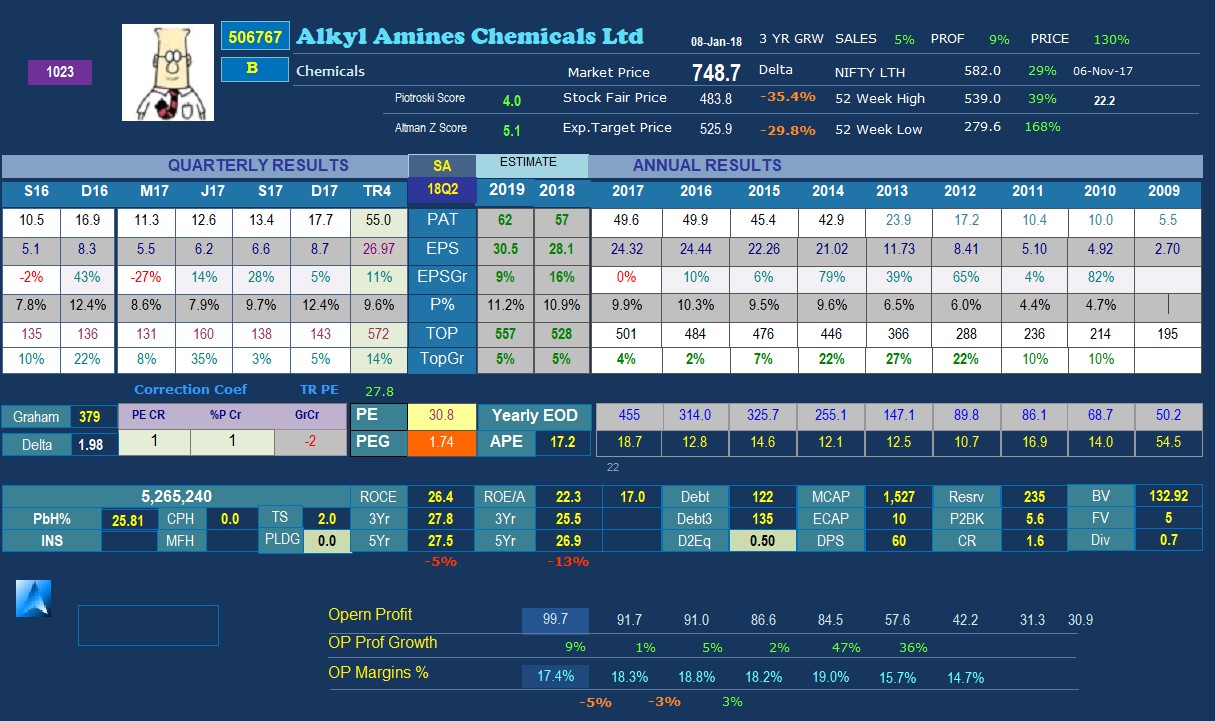

Good to see BOB research data. It seems to have projected FY16 EPS of 26.82 and EPS growth of 16% yoy. This appears to be a miss (actual as per money control and screener.in are less. Subsequent to this June quarter result seems to be bad, but no update from BOB capital on that result yet and my feeling is it has not progresses as good as their projection, but i may be wrong in jumping to conclusion too early. One or two quarters may not necessarily decide fate of company. BOB capital seems to have review after March quarter results and they have still kept FY17 EPS growth to be 16%. It would be interesting to watch how it progresses in next couple of quarters. Keeping fingers crossed since i have already invested some bit though not large quantity.

@valuehunt - I am personally not thinking too much about the hits and misses Q on Q.

My thesis is - the capex is via internal accrual, may add 250 cr to peak sales ( which is at 450 cr now), and the de-bottling of current capacities will add 50 cr more. I have faith in the management execution from what I have researched. I plan to hold and see how things pan out and exit only when any one of the above assumptions is proved incorrect. I expect gains via EPS expansion and not via PE expansion as at the end of the day its a commodity like business.

do anyone has idea for negative growth in Topline and bottomline in Q1Fy17?

Prashant

Negative growth in Topline and bottom line is due to less demand for some of its Product. Having read the Annual report, I believe Management is trustworthy but company doesnt have a moat due to which they had to lower the sale prices of the products and highly depend on pharmaceutical industry which is in sluggish mode due to USFDA import alerts.

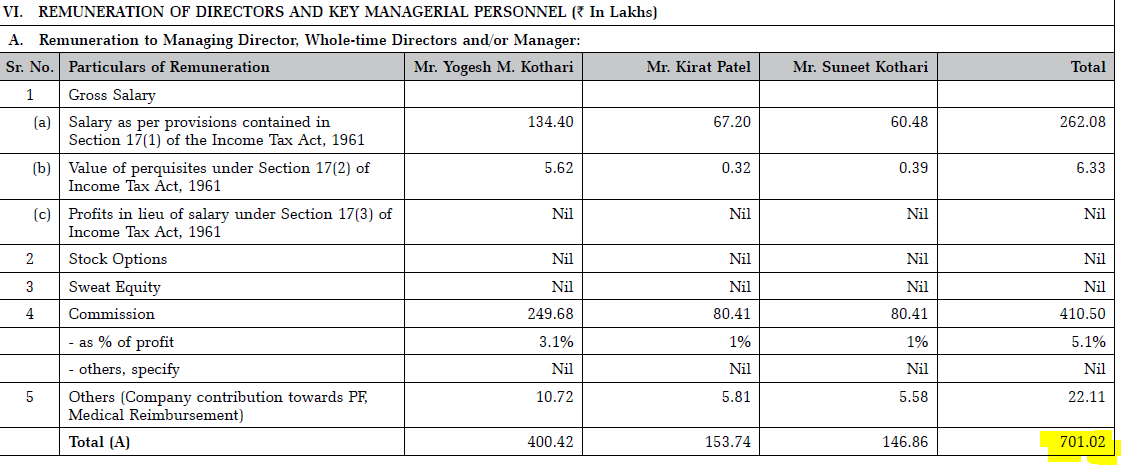

as per AR 2016 the whole time directors are getting a salary of about 14% of PAT. I think the ceiling is 10%. Is this ok?

As per the companies act, is the ceiling 10% of PAT or 10% of profit before tax?

I think the recent price hike due to ban of exports from China has just given all similar companies like this one a free run. I think this is more structural, so untill competition comes up, it’s a complete pricing power in the hand of the company.

Its not a stock reco. Views expressed are personal

Has anyone done a comparison between Indo Amines and Alkyl Amines? I’ve recently been studying Indo Amines and it looks good fundamentally, promoters have also increased stake and it now stands at 74.26%. It seems to be among the few players in India that are into Fatty Amines too. I’m finding it hard to figure out whether they have any market edge in this category or any other category as there is no coverage of this stock or even any concall transcripts.

From a price perspective, the stock has been on a uptrend since '16. It’s currently available at 88 after a recent drop and has a EV/EBIT of 12.

My notes from Q4FY18 concall -

Manufactures methylamines, etylamines, propylamines, and other mixed amines and derivatives.

Total capacity (fungible with minimum investments) - 100000 - 120000 pa.

Whether EBITDA% is sustainable?

Due to Industry tailwinds (China) they had better realizations (customers’ business improved due to china factor). Customers want to buy locally as much as possible. At least half of it is volume growth (10-12%). Improved performance is due to VAP and derivatives such as esters where realizations have been much higher.

RM (Methanol) has been on an uptrend. Buying all on spot basis. Ammonia is important but doesn’t impact much despite fluctuations in overall scheme of things.

Mathanol Q4FY18 33500 Q4FY17 29000

Ammonia Q4FY18 29000 Q4FY17 34000

Acetic Acid Q4FY18 54000 Q4FY17 48000

Isopropanol Q4FY18 78000 Q4FY17 70000

Ethyl Alcohol is steady. Large consumption.

Dahej facility (Methylamine) commenced from Q1FY19.

Cost - 165 cr.

Added Capacity - 30 ktpa.

Expecting 70% utilization by FY19E.

Asset turns - 1.5

Also building downstream product capacities here.

Acetonitrile (Mulling where to put and how much). Got clearance (70-80 cr capex planned for FY20 for this product. Doing cost benefit analysis). FY18 was tough for Acetonitrile, margins were much lower.

Utilization - 90%.

FY18 Price 150±. Fy17 Price 130±.

Volume growth guidance - 15/20% for next 2 years

Rate of Interest - 8.1%

Existing capacity for Methylamine at Patalganga - 15 kpta (will be used for some other amine forms now). Methyalamine domestic market size - 70 kpta.

Realization - 70-80 per kg

Min margin - 20 Rs/kg

Good margins here as imports for this product is not possible due to mixing with water while transporting

Though Methyalamine margins are lesser than overall company margins.

Isopropylamine capacity at patalganga - 10kpta

Top few derivatives they are present in -

Methyalamine -> DMAH -> used in metformin (inreasing capacity at Dahej)

Methyalamine -> DMAPA -> used in betains

Also looking to expand VAP pf.

Current DMAH capacity 100% utilized

Pataganga 15 kpta methyalmine capacity is fully fungible. They can go for ethylamines, morpholine, isopropylamines. Mulling many other products as well.

20% of total sales is exports.

Next 2-3 years capex - 50-100 cr pa

Overall, the company over last 5 years has managed to maintain/improve ebitda margins by focussing on good product mix, integrated business model, investments in r&d, efficient manufacturing processes, high utilization, focus on import substitutes, and all this helped by limited competition domestically. China tailwinds is resulting in improved demand and realizations of course.

The products they manufacture are raw material for API in pharma and agrochem and few other industries.

Disclaimer: tracking position.

Does somebody know a place to track methyamine and ethylamine prices? i Couldn’t find it googlinig it.

I had attended the concall of Alkyl Amines. Some of the points I noted in the concall:

• Volumes growth for FY19 – split between volume and value growth – Volume has been larger portion and price has been smaller portion. Volume growth is 2/3rd and 1/3rd is price.

• Decline in gross margins during Q4 – Large extent is due to raw material price increase in previous quarter impacted. Change in mix of the products has also led to decline in gross margins.

• Tax included deferred taxes and tax on esops also. Q3 deferred tax was understated. Overall tax rate for the year is 35% of the PBT.

• Competition set up acetonitrile plant which is expected to ramp, impact of same? Definitely it will have an impact.

• Capex – every year 150 – 200 crore capex. Capex 70 crore. Next year will be 100 crore and FY21 will be 150 crore.

• Capacity utilisation of 80% for the year.

• Gross margins guidance for next year or so? Gross margins has two impacts – selling prices and RM prices both have an impact. Going forward finished goods prices will catch up although RM prices will remain high. Hopefully, we will be back to gross margins of old days. RM – acetic acide, ammonia and ethyl alchol – prices increased.

• Methyl amine Dahej plant – capacity utilisation this year? We have managed 70% utilisation during the year – couple of % more. Expansion in Dahej? We are going to debottleneck by end of the year in two stages to bring out 45,000 MT. First phase will get completed by year end – take capacity to 37,500 MT by year end.

• Acetonitrile capex – done part of debottelenecking – some portion remaining

• Next year capex is for derivatives and other infrastructure investments. Year after ie FY21 will be for amines.

• Imported large consignment of RM for which payment fell in April first week. Happens on and off. Other current liabilities going up? Normal course of business.

• Trend with methanol prices going ahead? Trying to derisk it? We have been buying methanol from shippers. Prices currently are stable. Things are going on regarding Iran. In next one month or so we will get better idea.

• Bulk of growth has come from volume, not able to pass on the prices? We cannot sell prices higher than what existing prices are in market and imports. We do not want to loose the market share. We will have to reduce the market share if we increase prices higher than market.

• Amine derivatives – haven’t come across any of these pressure from China imports.

• Demand outlook to remain stable – local producers also produce derivatives. Demand of end user hasn’t gone up the way we thought during the quarter. It all settles down at some stage.

• Capex plan – this year we will be de-bottlenecking – one or two specialty products which we has been produced by others we will now will be producing it – asset turns – 100 crore capex to be planned across three plants including infrastructure – derivatives plant turnover ratio is 1.5 times to 2 times. It will take 2 to 3 years for full capacity utilisation.

• 220 crore increase in revenue – some part is derivatives of methyl amines, other is natural growth for other products also. Some of the other products have done well that has also helped.

• Gross margin reduction – high cost inventory of ethyl alcohol, product mix impact shifted towards methyl amine which are lower margin product than ethyl amine.

• Yet not reached 30,000 MT capacity touched 21,000 – 22,000 MT. Towards end of this year we will have de bottlenecking completed. Have capabilities in place.

• Volume from methyl amine will be 20% CAGR for two years. How it will be absorbed? 3 players in the market. Even if the market grows by 8 – 10%, other 2 players are not expanding capacities. In fact, RCF has reduced capacity last year.

• Pharma doing well and agrochemicals doing well. Would you say industry as a whole can grow volumes by historic growth rates of 8 – 10%? Quite confident about pharma side, agrochemicals will still depend on monsoon. Its possible that growth rates will be much higher than historical growth rates.

• This year we have strong volume growth on back of Dahej expansion. Volume growth going forward in next 2 years? We are hoping that volume growth will be 12 – 15%. We have incremental capacities for that.

• Patalganga – methyl amines capacity switched to other amines. Already done that. Kept methyl amines option open. Producing other amines currently.

• Acetonitrile prices – gross margins scenarios? So far the scenario looks encouraging as acetic acid prices are better than what they were earlier. Also, lets see what happens between China and USA. So far its ok.

• Capex – 70 crore this year slower than 100 crore earlier. Budgeted about 80 - 85 crore. Mainly on account of slippage in one plant due to delay in delivery of equipment. Nothing to do with demand.

• Dahej plant – except for first month, rest of the months have been reasonably steady.

• With current capacity, we can touch 1050 – 1100 crore? If prices remain same, yes we can touch that. But we are doing capex. Hoping to push that topline even further.

• Inflection side – we are still in the same frame of mind. We have lot of projects in our drawing board. One by one we are clearing them. Once the approvals are done, we will set them up. Direction remains the same.

• Q4 growth compared to Q4 growth last year? Volume growth has been the major component of that. Price has been second thing. Product mix change also happens.

• Dahej plant commenced in March, 2018. We might see few quarters where we might not see volume growth? Our 15% growth is something like 7 – 8% market growth. Other competitors are reaching full capacity. We have multi purpose plants with total capacity is 80,000 tonne plus. No major expansion coming in near future, how revenue growth will look like? We have significant room for volume growth this year also. For older plants we keep on doing de-bottlenecking and increase capacity.

• Gross margins trend? Pressure has been eased out? Difficult to predict what is going to happen in the future. EBITDA margins of 19 – 21% have been consistent.

• Capex – demand really coming from – same kind of sector, clients etc? they are aiming towards pharma and agrochemicals. We are hopeful that the pharma market will remain aggressive and overcome its problems which were there 2 years back and agrochemicals also doing well. What is really driving the growth – end product by clients doing well? This is our clients growth which will drive our growth. Pharma is our major sector. Volume growth has been good. This year they seem to be catching up and trend will continue going ahead.

• Revenue mix to change towards exports growing forward? Changing a little more in favour of exports from 20% earlier to 22 – 25%.

• 100 – 150 crore annual capex. From demand side, do we get contract from customer side? No one gives guarantee. But pretty good risk to take.

• Broadly, four year hence how much times the capacity will we have? I think if you look forward we will add 30 – 40% capacity through de-bottlenecking and new capacity over the next 3 years. Also product mix will change.

• Pharma – metmorfin product goes into it. Almost 60% sales is to pharmaceutical industry. It goes into 20 different APIs. Statins, blood pressure etc are key segments. Working on new products for new APIs. Amines is a versatile molecules. Used in large number of medicines. We are among the first one to supply and get our names registered.

• Share of derivatives this year? Will it go up as we add capacity? Don’t have exact nos. This year has been little bit more amines. 30% derivatives sales.

• Most of the capex will be at Kurkumbh and Dahej for expansion.

• Agrochemical and chemical capex announcement? China is not an issue. Sometimes China becomes a problem when our customers don’t have product from China. Question how are customers are making use of intermediate from other countries. Hopefully, all this comes in line in next one to two years.

• Pharma perspective – new capex not happening? Don’t think there is an issue as per our products are concerned. Products themselves are increased both on domestic and export side. Our products are used in many usage like shampoos, water chemicals. This will continue to grow.

• Capex – 100 crore break up – wouldn’t like to disclose that.

• Margins – bulk of the capacity addition will be for methyl amines derivatives. Do you see a structural change in margins to lower levels? There is a mix of product mix and some RM and finished good prices moving in other direction. One is hopeful that margins will restore to its normal state. It overshoots on the other side also.

• Price of acetonitrile current and past? Our price is we enter into agreement with customers. Revision of contracts happen every 2 – 3 months. Hopeful of getting some benefit.

• Capacities going to move? 30,000 methyl and rest is ethyl amines and derivatives. 3 years targeting 30 – 40% capacity addition. Normally 3 year cycle for us 2012 – 2014 bumper growth, 14 – 15 lower growth and then pick up. Difficult to predict volume growth? Volatility in volume growth beyond our control. Longer term will settle at 8 – 12%. Higher capacity addition phase and lower capacity addition phase. When we put a new aliphatic amine plant, it is once in decade opportunity. Similar kind of volume growth is not possible in FY20? Its not just capacity but market. Still at 80% capacity utilisation. Difficult to repeat 40% growth this year. Growth of 20% possible given demand and other things – volume growth. Value is difficult to predict.

• Both amines segment and derivatives segment grew well this year.

• The capex in derivatives segment is mainly for increasing capacity of existing derivatives and introducing two new products in speciality segment. These new products will largely cater to pharma and agrochemical industry.

• The prices of acetonitrile has increased quite a bit over the past few months due to some shutdown of large plant globally. We have two months contract with our customers for it. Post the contract gets over, lets see how pricing moves.

(Disclosure: Invested)

Q1FY20 results

Very Good results.Revenue increase…50% Y-O-Y & 16% Q-O-Q.

Profit bef exc items & Tax…13% Y-O-Y & 11% Q-O-Q

Net Profit…10% Y-O-Y & Q-O-Q

Discl: Invested

I had attended the AGM of Alkyl Amines held in Mumbai on August 6, 2019. Some of the key points I noted during the AGM:

• Planning to increase capacity at Dahej and Kurkumbh both. In Dahej – Methyl Amine capacity expansion (30,000 MT to 45,000 MT), derivative plant as well as acetonitrile expansion will come up.

• We will spend Rs.200 – 300 crore on capex during FY20 and FY21 depending on EC approvals. Most of the capex will be funded through our internal accruals. We already have EC approvals in place for few products while have applied for EC approvals for others.

• The return rations and asset turns for derivatives and speciality chemicals is much better than aliphatic amines (2 times asset turnover vs 1.5 times for aliphatic amines) but one cant do away with aliphatic amines as they supply the RM to derivatives plant. Mother (aliphatic amines) plants is usually set up once in a decade.

• Apart from capacity expansion plans, we keep on working on plans to improve efficiencies in processes and plant. In terms of following pollution norms, we are way ahead of market.

• Dimethyl Amine HCL (amine hydrochloride) is almost like commodity products. Dimethylaminoproply amine (DMAPA) is used in surfactants but it’s a smaller opportunity size in India given its small market size compared to world markets.

• We are working on new products which are import substitutes (for domestic market) and also looking at export opportunities.

• Debottlenecking capex is most return accretive as for a limited capex one gets big upside.

• The payback period for new green field plants is 3 to 5 years while its lower for brown field capex. Green field capex takes at least 2 years to come up.

• Criteria for selecting new products:

o Technology and our chemistry skills to manufacture it – Why are we better in it?

o Competitive landscape for the product

o Opportunity size

• Pipeline of products is developed by us developing the new products through R&D as well as customer approaching us to manufacture a product for them

• Ideally, it takes 3 to 4 years to develop a new product. Our R&D team has been working on for 3 – 4 years on the products that we plan to launch in near term.

• Q1FY20 results – the impact is not just because of acetonitrile but we have seen healthy volume growth in aliphatic amines as well as derivatives. The acetonitrile prices went up due to shutdown of plant of a global competitor. The supply is expected to come back soon in the market.

• We have some exposure in autos where we supply our products (primarily rubber chemicals) but its not substantial (less than 5%).

• We continue to see good demand in export market as well as domestic markets from our key customers across pharmaceuticals and agrochemical markets.

• We do phase out some products which don’t scale up but its proportion is low in our overall sales.

• We have a large basket of products – decline in sales of one products gets compensated by other product.

• China issue is a structural issue in the overall chemical and API industry. Chinese Government has taken long term view on environment and has become stricter. Even if the Chinese supply comes back, the prices of products will not go back to earlier levels. Although, our products don’t have much direct impact because of China issue but our customers do which in turn impacts our demand. Lot of API companies in India are expanding capacities and product basket. Lot of these products were earlier imported from China.

• While looking for any products we focus on IRR. Not looking at any opportunities where margins are low. We are not chasing top line but focused on bottom line.

• Gross margins in our business will vary depending on product mix. Last 2 quarter numbers, were impacted due to product mix change.

• The supply of ethanol to refineries (as mentioned in AR) has some chemical processes and that opportunity comes once in every year. We might bid for such contracts this year as well. This is not significantly contributing to revenues.

• Impact of raw material availability due to Iran ban? Iran is not the only supplier for ethanol and methanol. Already, supplies are coming for other countries.

• Product price revision happens on monthly and quarterly basis depending on products and client relationship.

• Its not necessary that multistep products are more complex. Even for a single or two step process the chemical process can be complex.

• In R&D we have 25 people and plant to increase it. We also want to increase their efficiency.

• Acquired a piece of land adjacent to our Dahej plant for future expansions during FY19.

• Most of the capex for next 2 years will focus on amine derivatives and speciality chemicals. In speciality chemicals also, we will launch new products. In FY20, we plant to start 3 new plants (one already started in Q1FY20) while in FY21 also we plant to start 2 – 3 new plants (at existing locations).

• Europe and US are our major export destination. We continue to focus on exports and launch new products for it.

• We continue to focus on amines chemistry for the next 3 – 4 years as our hands are full with these chemistry only.

• We continue to maintain our guidance for reaching Rs.2000 crore revenue in next 3 – 5 years.

(Disclosure: Invested)

Rating Update dt Aug 23, 2019

https://www.investing-notes.com/alkyl-amines-bse-506767-nse-alkylamine/

Post on Alkyl Amines.

Diamines & Chemicals: Promoter Alkyl Amines Chemicals sold 29.8 lakh shares (30.44%) at Rs 115.12 each