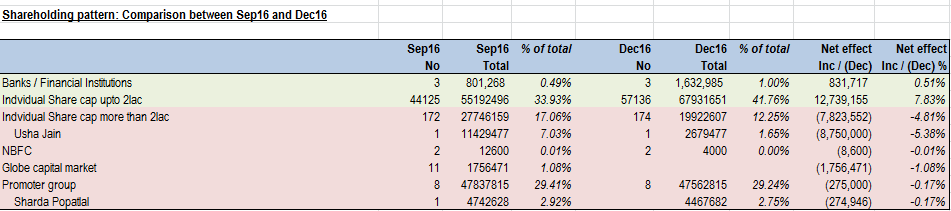

Some possible red flags here with the new shareholding pattern for Dec-16 released

- Usha Jain has decreased her stake which everyone knows

- Sharda Popatlal has decreased her stake (0.2% of total) and no other promoter has purchased it which means that its possibly gone to the public

- Another decrease is in ‘Individual more than 2lac’ bracket which has gone down drastically by 5% of total shareholding ie 7.8m shares

- The increase is only in ‘Individual upto 2lac’ bracket which means retail investors like us

- The only small positive is that Banks / Financial Institutions braccket where the 3 investors have increased their stake by 0.51% of total

However, on a read of this, it doesnt look good. This can signal two things as per me:

-

Much higher chance of this share being operator driven now.

-

Small panic can lead to large downfalls given the shareholding breakup

Here is a snapshot

Disc: Invested

As per the declaration filed by the company, Sharda popatlal sold shares before Q2 results…i dont think its going to have a bearing on the stock price now. …in a way its old news.

Secondly, in the coming quarters the EPS of Aksh is expected to jump quite significantly…once the capacity expansion and upgradation is completed. At that time, the operators may pump up the stock to higher levels. I too have said at the begining of the thread, that its an operator driven stock.

Instead of worrying about it now (when the stock is trading at a low p/e), we should remember about it being operator driven stock, when it is trading at much much higher levels and everything is lioking good and rosy. Thats when the dumping / distribution will start.

Today Sterlite Technologies came out with a very good Q3 result…there was an impressive increase in the topline and the profit before tax almost doubled when compared with Q2 results. In the conference call the following points were noteworthy…

-

Most of the analysts congratulated the management for very good Q3 numbers. That itself can be taken as a good indicator of the quality of the Q3 numbers. It seems there was no adverse affect of demonetisation on the production and sales of Sterlite technologies.(Hence we may expect good numbers from Aksh optifires too)

-

PRICING…it seems the international price of Optical fibres ranges from 7 - 8 USD and is presently at the higher end of this price range. The indian price is directly linked to the international price. (Thus we may expect good price realisation for Aksh too)

-

DEMAND>…The mngt of Sterlite sees very robust demand continuing for 5 years and more. The main drivers of demand in the international market are China and Europe.in India there will be continued demand from the Smart cities and telecom operators - who keep adding layers of Optical fiber cables for providing 2g, then 3G…then 4G…then 5 G…

Also the first phase of linking 1 lakh villages under Bharat NEt is set to be completed. The next phase is even bigger linking about 1.5 lakh villages. And then there is demand from Armed services for a separate network for them.

Thus Aksh too may have a good demand for its products in the next few years. I expect the next phase of expansion in Aksh to begin with capacity expansion of the newly purchased Unitape facility. The mangt of aksh has already expressed its preference for FRP rods because of its high margins. Hence Unitape expansion may be on cards.

In all the fibre optic makers are neither affected by demonetization nor fall in rupee value against USD as exports to China form a big component of turnover.

Yes, nice results from Sterlite. It seems to be a good company to invest as well. Hoping for a rub off effect on Aksh.

disc: invested in Aksh

A push for fibre deployment. The last paragraph shows the tremendous scope and opportunities that are ahead for all optic fibre manufacturing companies

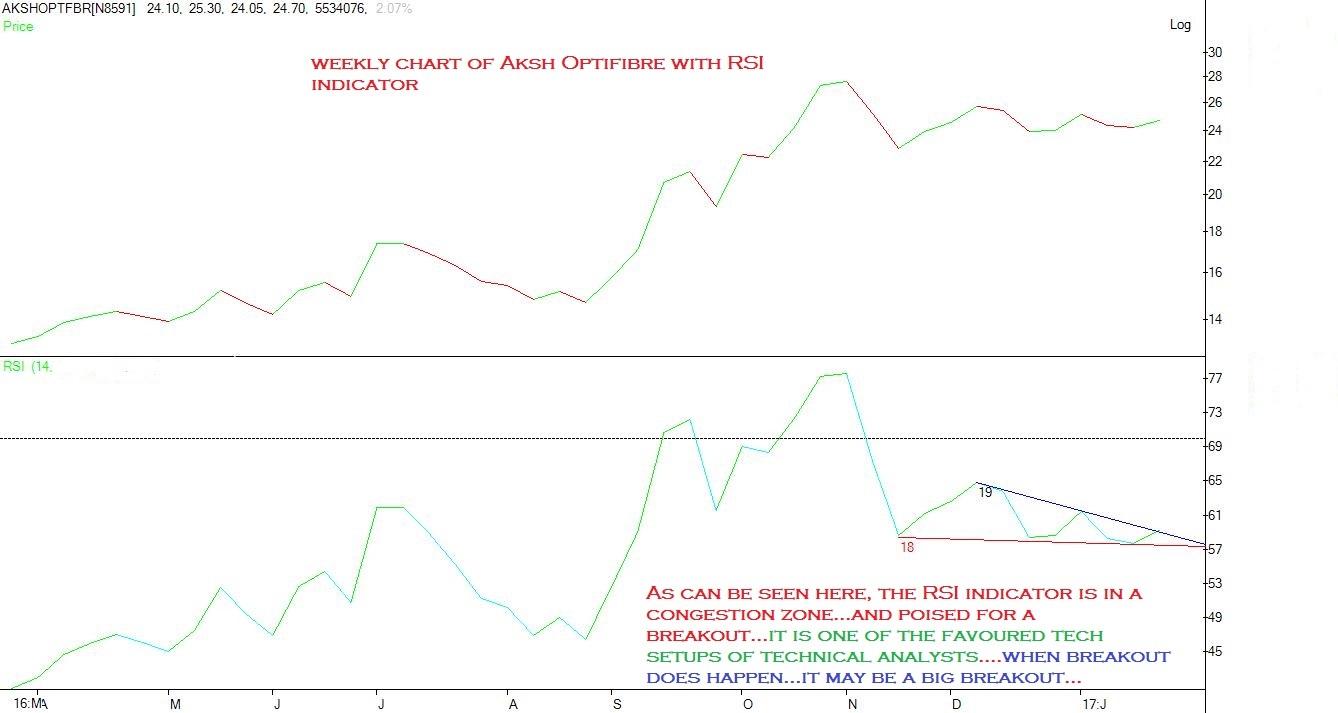

You talking about STERLITE or Aksh or both !

I am now talking sbout Aksh…sterlite alreqdy had a breakout when the stock raced from 95 to 125 in a short period…

Thanks. Q3 will be released on 14th Feb. Let us see signs of inside trading

- if any.

Mehnazji

This is the quote on the Apar Industries thread as per the concall details. What is your take on this?

Another quote on the same thread.

2017 Budget has the BharatNet Project with plan to connect 1.5 lakh villages with optical fibre. Assuming this initiative gets off the ground and is implemented properly, we should see a rise in Optical Fibre demand?

Bad result from Aksh…topline growth is impressive @127 crores…but the profit has fallen…mainly on account of increase in cost of raw materials…eps for this quarter@12paise is really pathetic…its less than even last quarter…For a low debt company which claims to be the most efficient manufacturer…this kind of eps is quite disappointing.

Suggest holding the stock for one more quarter to see if there is any growth in profits…if not then exit…as of now investors may brace for a fall in stock price…with this kind of result, difficult to see the stock going up in the near future.

The only saving grace is higher tax expense. Almost 3 cr, which wasn’t there last year, somewhat soft lands it a bit

The worldwide optical fibre cable deployment reached an all-time high of 420 Million Fibre-Km in the year 2016.The global preform capacities being fully utilized has led to worldwide shortage of optical fibre, creating a demand-supply gap and firming up of the optical fibre prices across the globe. This situation has put an adverse impact on the margins in the OFC business. However, this situation will improve with the proposed global expanded capacities of preform becoming operational in forthcoming quarters

The raw material costs might be high in Q4 also. If they can’t pass it on to their customers, margins will continue to be under pressure.

I agree. We have been discussing about the prospects of the industry- but have never discussed about quality of management- professionalism, integrity and attitude towards shareholders. Sudden high level/fluctuations of tax provision makes me uncomfortable about predictability of bottom line.

Can we trust the management on all counts. They have been around for more than a decade. Can we share our perception of their past performance on all fronts. If they do not inspire confidence- let us move elsewhere- irrespective of the industry prospects.

A very experienced investor has bought some points to my notice…

In microcap stocks the usual mechanism to depress the eps is to book the next quarters raw material costs in the present quarter. Thus the very factor that causes the eps to fall in Q3 will cause the eps to rise hugely in Q4 as in Q 4 the raw material costs will be quite less…

Also the tax shown is unusually high, more so for a company like Aksh where exports form a significant portion of the topline. This too will be used to supress the eps in the present quarter…

The sole purpose of resorting to such tactics is to discourage the retail investors from buying at the present level / lower levels and once the weak hands are shaken off, then the stock price will be pumped up.

Since, I am not a chartered accountant, I cannot comment on the above points. I therefore request, those from accountancy / finance background to examine the above and offer their comments.

In your dilemma lies the answer, higher pe is given to stocks who have stable earnings and investors can calculate or perceive earnings.

What does this perceived accounting manipulation reflect on the quality of management.