Ajanta Pharma’s AR is out.Key takeaways:

-> Company registered a growth of 16% in the domestic market as against 11% for the industry.This was led by 28 launches in the branded generics segment.9 of these were “first to market”.

-> The anti-malaria business in Africa was the worst hit.Company says it has always been forthcoming about the unpredictability of this business.The immediate future remains uncertain.

-> US business grew 46% on the back of 8 new launches.This takes the total number of “on the shelf” products to 25.Company expects to make 10-12 filings every year(13 ANDA filings in FY19) However,the cost of servicing the US market has risen and thus,Ajanta expects this market will be challenging.

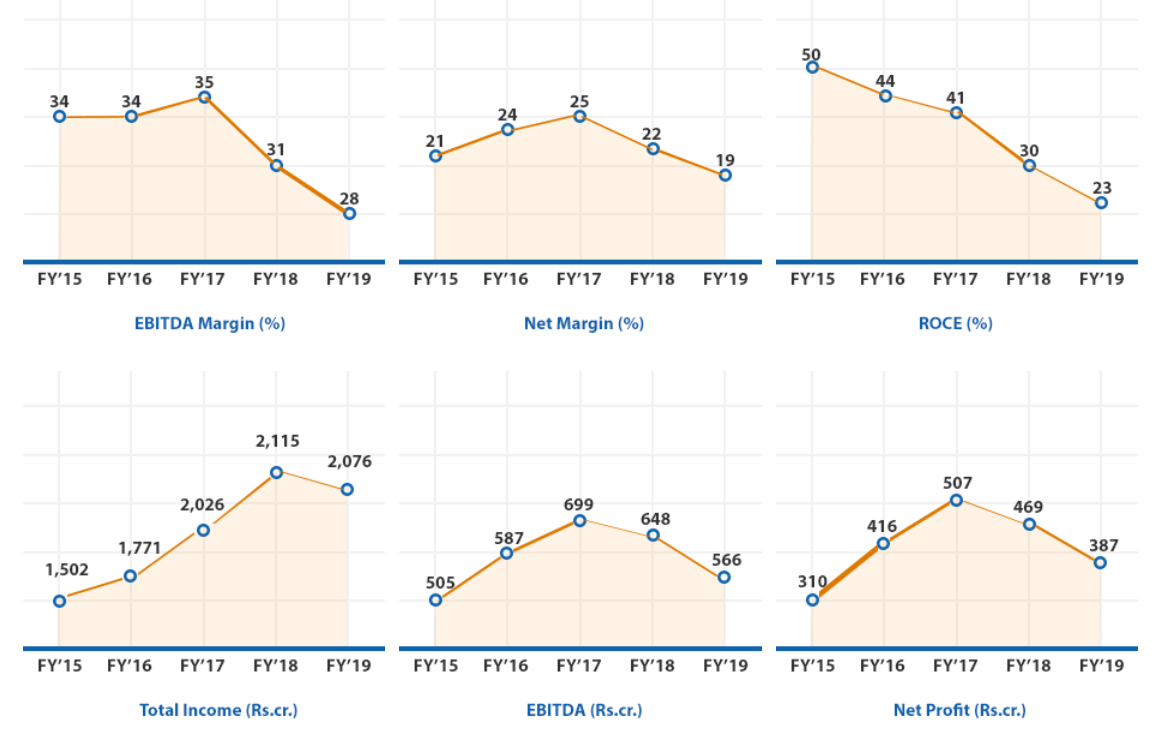

-> Due to a 49% decline in revenues from the Insttl. business,the company registered a de-growth in revenues.This is the first time in 15 years that Ajanta has reported a YoY decline in revenues.

-> Company generated OCF of 375cr. which helped fund capex(361cr.) entirely from internal accruals.In Fy20,construction work on Ophthal section at Guwahati and greenfield manufacturing facility for oral solid at Pithampur in Madhya Pradesh will continue to put some pressure on margins.The total capex for FY20 is expected to be 350cr.

-> EBITDA Margins contracted by 250 bps.This was on the back of higher costs from capex at Dahej & Guwahati.The utilisation at both these facilities is still quiet low and thus Ajanta couldn’t offset the hit on margins.

-> The African markets started facing major issues two years back post Crude price decline.Thus,the company decided to fix any inventory issues they had in those geographies.Moreover,the management took a conscious decision to go slow in that market.The decline in FY19 was on “expected lines”.The US market has helped the company neutralise the adverse impact from Africa to some extent.

-> The company operationalised it’s expanded R&D wing in Mumbai.Total spend ~100cr. over last 2 years.

-> Inventory has risen due to growing US ops.The US market has a longer WC cycle.

All in all,I found the AR to be quiet subdued and “cautiously optimistic” at best.The company is preparing itself for better days(whenever they come back) …getting the new facilities stabilised and having an improved R&D centre.I got the sense that the management expects the issues in the Insttl. business to persist and thus the revenue growth may be muted in FY20 as well.On the other hand,the US market is looking good.However,higher cost of servicing and a stretching WC cycle are key things to watch out for.

The stock has done very little in an overall weak market over the last 1 year.RoE,RoCE and margins are at multi-year lows.Imho the time to buy is still a bit away.

Disc.: Not invested.Views are biased.